We lead with an appropriate cartoon from HedgeEye. In the current environment, investors appear singularly focused on whether or not the Fed will pivot. In layman’s terms, will the Fed reverse its incredibly hawkish monetary stance, or will it stay the course? Each bit of inflation and labor market data seems to increase or decrease the market odds the Fed pivots. The truth of the matter is that the Fed’s worst nightmare, stubbornly high inflation, is a reality. To fight inflation, they are raising rates at a clip last seen over 40 years ago and doing $95 billion of QT a month. Equally important, the Fed’s rhetoric is determined to stay the course and not pivot.

Most likely, they will not pivot until inflation is tamed, the economy is a train wreck, no pun intended, or a financial crisis. We think it’s likely that financial instability, which may coincide with the market train falling off the cliff, is the event that gets them to pivot.

What To Watch Today

Economy

- 08:30 AM Empire State manufacturing survey, October (consensus -4.0, last -1.5)

Earnings

Market Trading Update

Another volatile market week continues to weigh on investor psychology. Such remains the most dangerous part of a bearish market, as emotions begin to take over logical investment processes. The market traded quietly early in the week in anticipation of the September inflation report, which was much hotter than expected. On that news, the market initially broke down but mustered a strong rally of 5.5% from the lows.

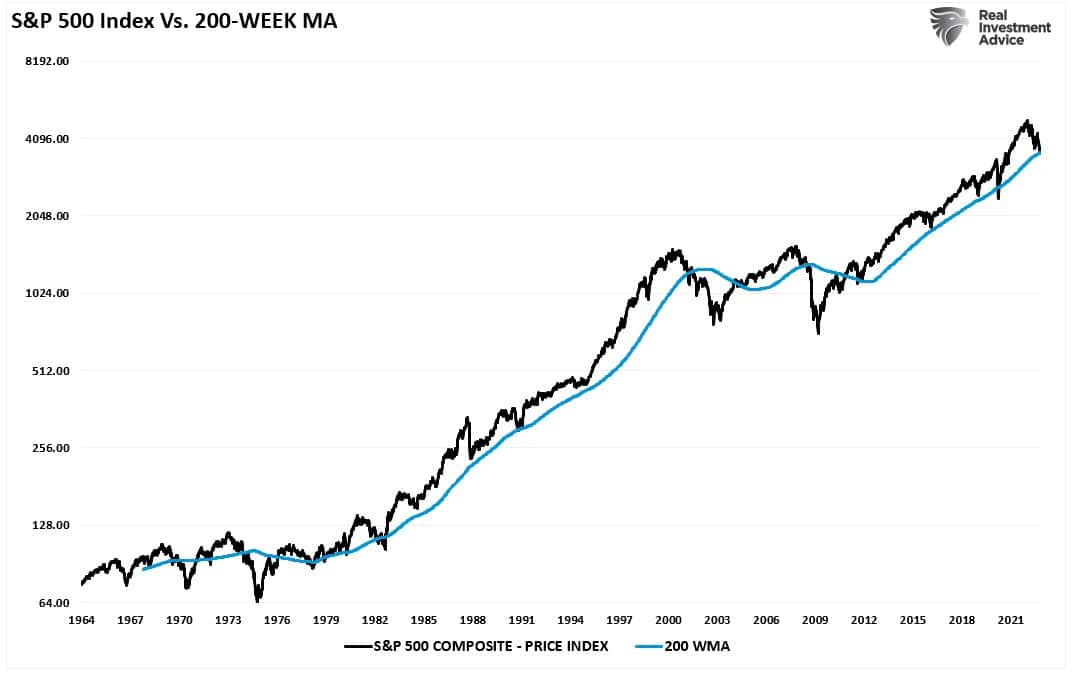

Notably, the market is sitting right at support at the 200-week moving average, which has defined the “bullish trend” since the financial crisis lows. In other words, despite the “correction” from this year’s highs, the ongoing bull market remains intact. However, a break below that bullish trend will constitute a confirmed bear market.

This is an important point.

While the mainstream media continues to define the current decline as a “bear market,” it remains a “correction” within the bullish trend. Many factors don’t currently exist that coincide with previous bear market cycles.

- Surging unemployment

- Recession

- Bankruptcies

- Defaults

- Fed cutting rates

- Falling 2-year and 10-year Treasury yields

- Un-inversion of the yield curve.

- Spiking credit spreads

- Surge in volatility

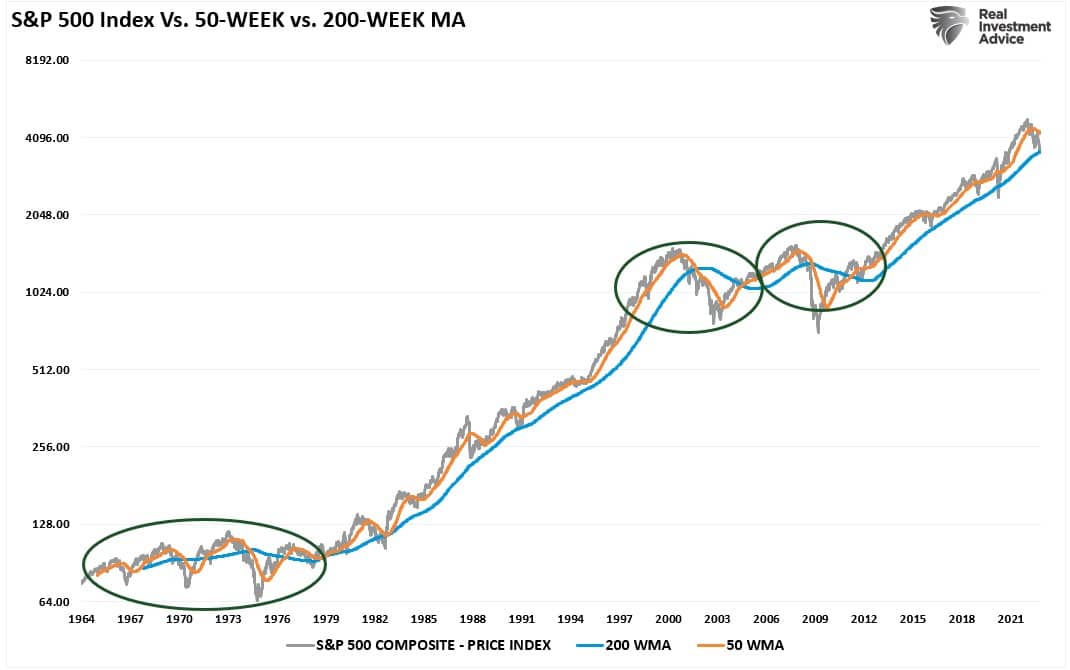

Most importantly, in all previous REAL “bear markets,” the market broke the bullish trend. Furthermore, the 50-week moving average crossed below the 200-week. Such confirmed the reversion.

Yes, those things may come, and if they do, we will see the bullish trend broken. However, for now, that is not the case.

With the market oversold on a short-term basis, and longer-term deviations more extreme, we continue to look for a reflexive rally to sell into to raise cash levels and reduce equity risk accordingly. While the defense of the bullish trend, as represented by the 200-week moving average, is encouraging, there is still a considerable risk of further downside as we move into 2023.

The Week Ahead

After two weeks of crucial labor and inflation data, the market’s attention will shift to corporate earnings. Over 500 companies report earnings this week, including Tesla, Bank of America, Netflix, Goldman Sachs, and J&J. Large tech companies such as Apple, Microsoft, and Google will report next week. As we have seen, we expect to see a fair number of earnings surprises, both good and bad. Further, executive commentary on how inflation affects margins and future outlooks will garner the market’s attention. As we have seen recently 10%+ stock moves on earnings should not be unexpected in some cases.

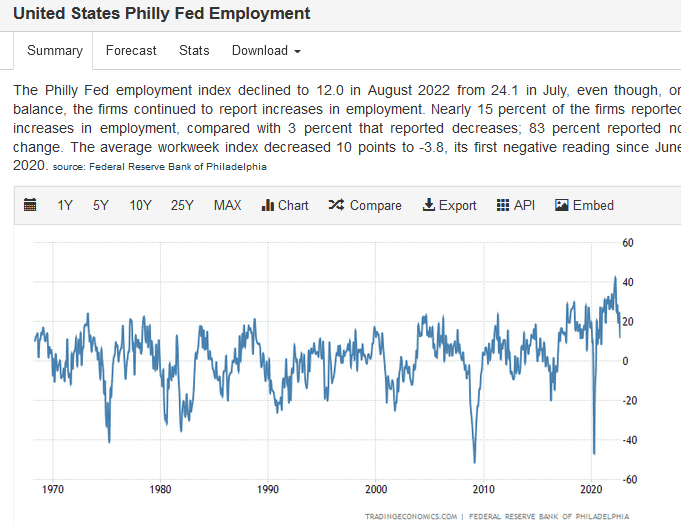

On the economic front, the Philadelphia Fed Manufacturing Survey will be closely followed. Economists are keenly looking for data to better gauge inflation and the jobs market. The data in the regional surveys tend to be much nearer to real-time than most official government data. Economists expect Prices paid to decline to 28. The first graph below shows the Philadelphia Fed price gauge has fallen back into the pre-pandemic range. After peaking earlier this year at a 50-year+ high, the employment index is also declining back toward more normal readings, as shown in the second graph.

Election polls will also factor into market direction over the coming weeks. Investors will want to know if the Republicans can take the House or the Senate. The odds of sizeable fiscal stimulus bills are lessened if such were to occur. While that result might be bond friendly, as it portends less debt issuance, it may weigh on stocks as reduced fiscal spending will crimp economic activity.

At 4%, Cash is no Longer Trash

Every Friday, SimpleVisor subscribers receive our Five for Friday blog post. The article shares an investment theme, such as high dividend value stocks or beaten-down tech companies, and runs stock scans based on numerous factors that define the theme. The result is five stocks that best contain those traits.

Last week’s Five for Friday took a different approach. With money market yields near 4% and larger cash allocations due to market volatility, there is significant interest in cash-like investments. Further stoking the interest, cash sitting at many brokerages earns well below market rates.

This week’s blog post, Five for Friday: Cash Surrogates, discusses the pros and cons of sweepable and non-sweepable money market funds, Treasury Bills, corporate notes, CDs, and fixed-income ETFs. We share the link with you to help address the growing desire to earn additional yield while taking little to no risk. SimpleVisor is a DIY financial website offering fundamental and technical research and tracking tools designed to help our subscribers get the most out of their wealth. Give SimpleVisor a try with a free 30-day trial. Better yet, use the coupon code – 25% Off 2022 – and get a 25% discount for the first three months. Cancel anytime within 30 days, and we will not charge you.

Deflation Will Become the Problem

Lance Roberts just published a piece arguing that, inevitably, the surge in interest rates will cause something to break. With that, our inflation problem may quickly become a deflation problem. Might the U.K. Pension problem be the tip of the problem? Per Lance:

As the Fed continues to hike rates to fight an inflationary “boogeyman,” the more considerable threat remains deflation from an economic or credit crisis caused by overtightening monetary policy.

History is clear that the Fed’s current actions are once again behind the curve. While the Fed wants to slow the economy, not have it come crashing down, the real risk is “something breaks.”

Each rate hike puts the Fed closer to the unwanted “event horizon.” When the lag effect of monetary policy collides with accelerating economic weakness, the Fed’s inflationary problem will transform into a destructive deflationary recession.

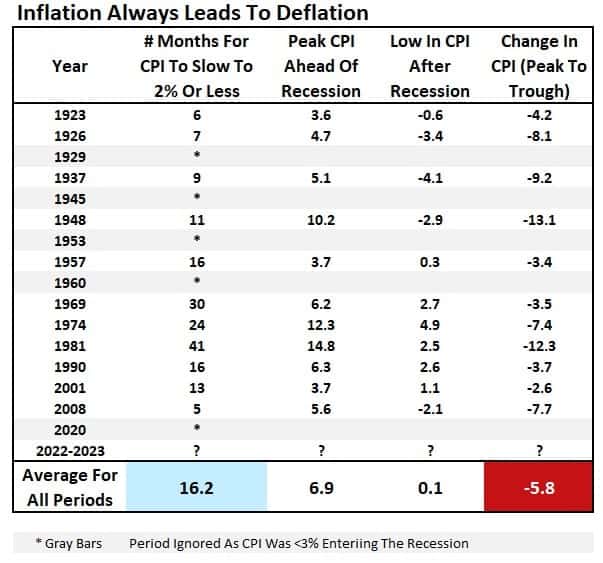

The table below from the article shows that every time the U.S. economy entered a recession with inflation running above 2%, it took about 16 months on average to fall to 0.1% on average. In 2008, the “breaking of something” led to a trough inflation rate of -2.1%.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.