Trade Alert For Equity and Sector Model

A Strong Case for the Euro and Yen

The euro has lost 12% to the U.S. dollar this year, while the Japanese yen has ceded nearly 20%. Those losses may not seem out of the ordinary compared to stocks or bonds, but they are. Foreign exchange markets tend to be much less volatile.

A weak currency versus the dollar is often good for a country as it makes its exports more price competitive. However, a weaker currency makes imports more expensive. Given the soaring rate of inflation, especially energy prices, this instance of a stronger dollar is wreaking havoc on Europe and Japan.

Making matters worse, many foreign borrowers borrow in dollars. If they do not hedge the currency risk, as many do not, a strong dollar results in higher interest and principal payments. Simply they must acquire more expensive dollars to pay interest and principal. As such, a strong dollar is a de facto tightening of global monetary policy.

Europe is doing everything possible to solve its energy crisis, but its options are limited as it is primarily a supply problem. While alleviating supply challenges is difficult, they can reduce costs with a stronger currency.

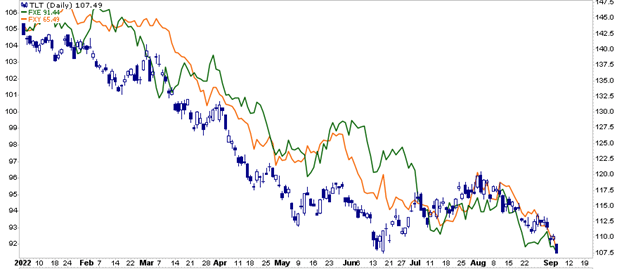

We suspect that the ECB and BOJ have been selling dollar assets, predominately Treasury bonds, to prop up their currencies. To support this theory, the graph below shows the strong correlation between 20-year UST bonds (TLT) and the Euro (FXE) and Yen (FXY).

If we are correct, such actions have been ineffective. In the past, the U.S. Treasury helped foreign countries manage their currencies via currency swap lines. Swap lines are off-market currency trades that allow countries to better manage their currency without selling U.S. assets or printing their own currency.

Given the sharp dollar appreciation and acute energy and inflation problems, we think the Treasury will reopen the lines. Once open, the nations will not need to sell Treasury bonds. Further persuading the Treasury, they have significant funding needs, and the Fed is reducing its holdings of Treasury debt. The growing supply of bonds from the Fed and the Treasury creates a powerful desire to cap yields.

Essentially swap lines kill two birds with one stone.

Such action should cap U.S. yields and help limit inflationary pressures in Europe and Japan. Equally important, it helps defuse what is slowly becoming a financial crisis in those countries.

We realize buying euros or yen versus the dollar is like catching a falling knife. Doing so is not comfortable, but we think the situation is becoming dire enough to warrant global coordination to stem dollar strength and rising yields.

We are adding 2.5% of FXE and buying TLT to return it to model weight. We may add to FXE, TLT, and or start a position in FXY in the coming future.

Equity & ETF Models

- Adding 2.5% of FXE (Euro Currency Trust)

- Increase TLT to Model Weight of 10% of the Portfolio.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)