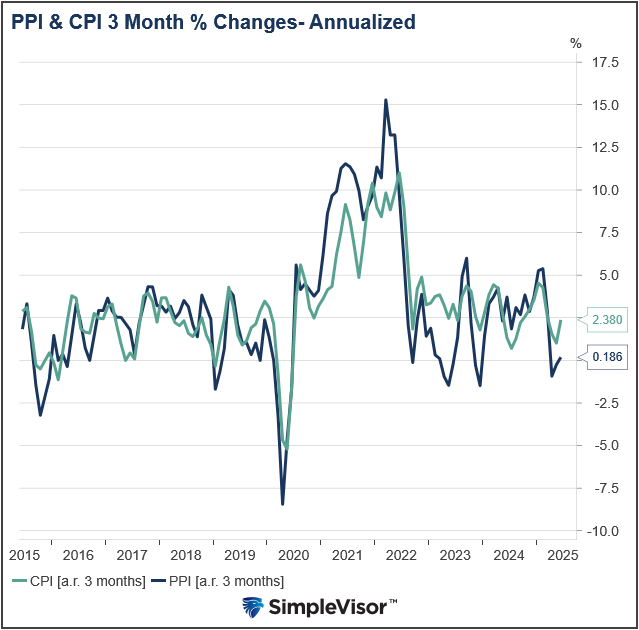

The BLS Producer Price Index (PPI), measuring wholesale prices, surprised to the downside, showing a zero percent increase in prices for June. PPI came in lower than what all 50 forecasters in Bloomberg’s survey predicted. To wit, both the core and headline figures were 0.20% below estimates. Notably, the headline PPI for the last three months has averaged near 0%, while the core PPI is less than 0.1%. Year over year, PPI is down to 2.3%.

This data challenges the idea that tariffs are an inflationary force, as producer prices are a key indicator of cost pressures that manufacturers could pass through to consumers. Instead, the weak PPI data suggests that supply chains and production costs are absorbing tariff impacts without triggering widespread price hikes. While tariffs will affect specific sectors, the broader inflation narrative appears overstated thus far. PPI and CPI should give the Fed a little more confidence that any tariff impact may be less than they initially feared.

The graph below shows that the PPI is now at the lower end of the range that prevailed before the pandemic. Moreover, CPI is closer to the average of its pre-pandemic range.

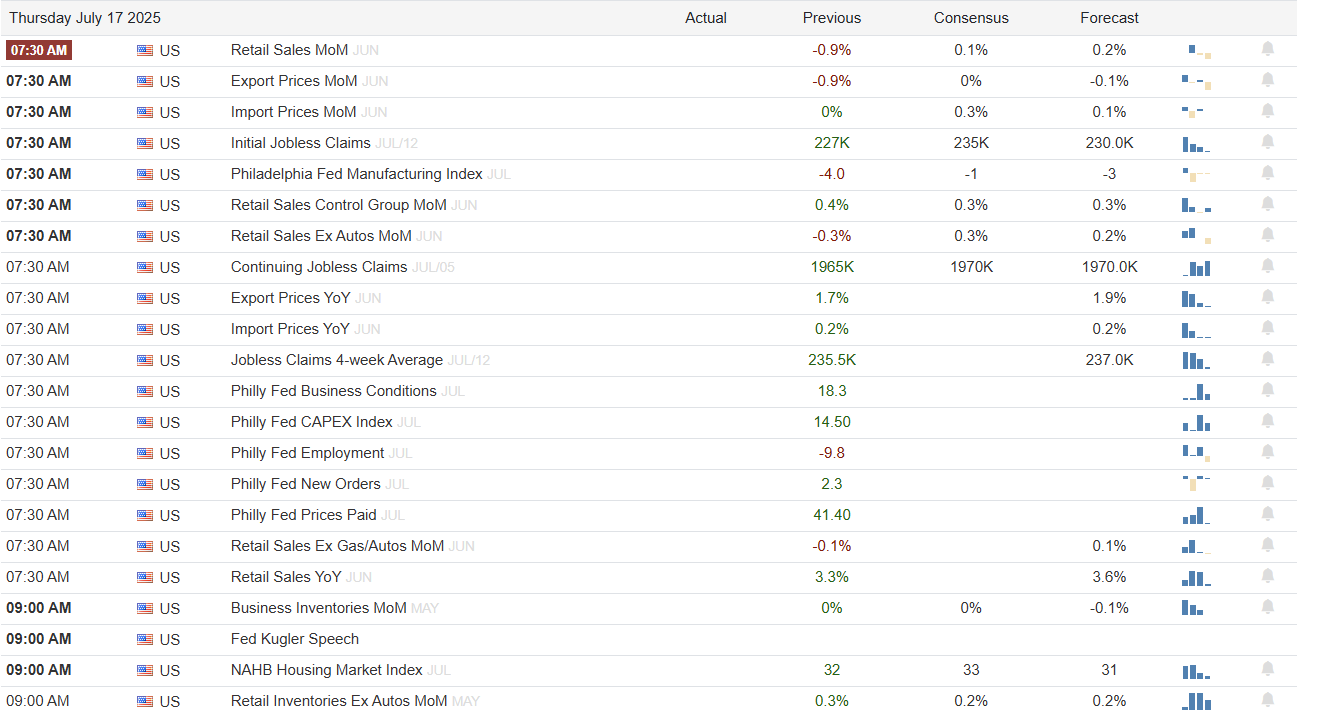

What To Watch Today

Earnings

Economy

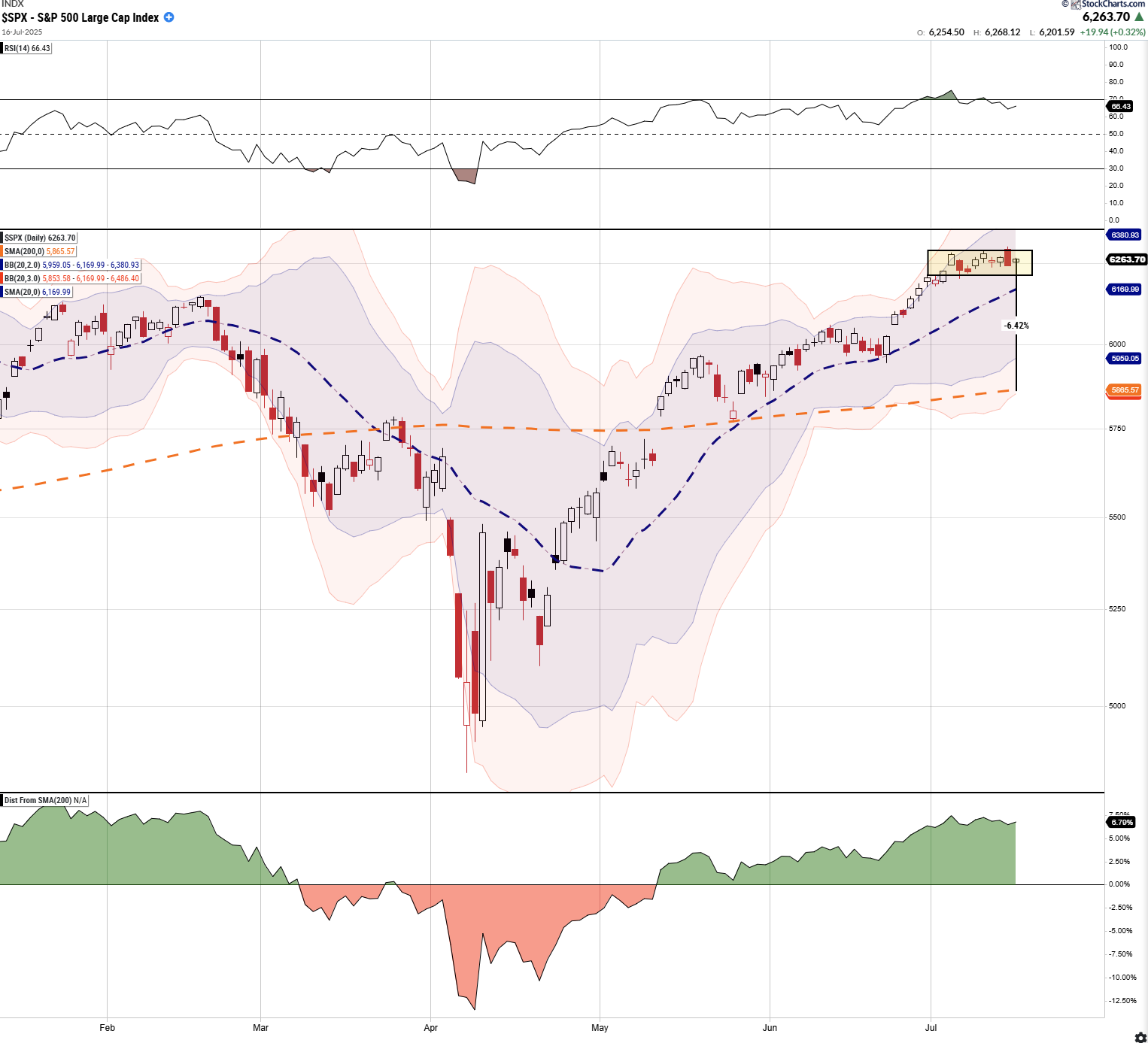

Market Trading Update

Yesterday, we discussed share buybacks and the return of professional investor exuberance to the market. Notably, positioning became elevated, and cash fell to very low levels. While this does not mean a “crash” is imminent, it does suggest that “everyone is in the pool,” to steal a Wall Street colloquialism.

Technically, the market is beginning to work off its more overbought condition and has remained confined in a consolidation range over the last two weeks. At this juncture, a correction to the 200-DMA should be considered more possible, which would entail a roughly 6% decline.

The building of exuberance in the market is part of the “bull market” process. However, when that enthusiasm reaches more extreme levels, it is also a contrarian signal often ignored by investors. The consequences of such are typically not conducive to wealth-building practices. The problem with the above analysis is that the “timing” of such a “mean-reverting” event is always tricky. Momentum in the market is difficult to stop, but it tends to do so quickly when it reverses.

Core Positioning:

- Maintain core equity allocations but trim exposure in extended sectors such as large-cap tech.

- Focus on high-quality, fundamentally sound companies showing strong earnings momentum.

Tactical Adjustments:

- Raise cash levels slightly

- Rebalance positions back to target weightings.

- Sell laggards that failed to perform during the rally from the April lows.

- Add hedges to portfolios as needed to reduce overall portfolio volatility.

- Add volatility protection through short-term Treasury bonds.

- Remain selectively long AI and tech leadership, but hedge tail risks as breadth weakens.

- Add selective hedges using short-term puts on the S&P 500 (SPY) to protect against near-term pullbacks.

Allocation Mix Suggestion:

- 60% Core Equity (tilted towards momentum names showing earnings beats)

- 20-25% Tactical (short-duration bonds, defensive positioning (value stocks), or hedges)

- 10-15% Defensive Assets (cash or cash equivalents)

Investors should stay flexible with equities sitting near record highs, stretched technicals, and rising rates. This is an environment to remain opportunistic but disciplined, buying pullbacks in key areas of strength while using hedges to mitigate downside risk. Capital preservation should be at the front of mind alongside tactical positioning as the market navigates earnings and shifting macro narratives.

Trade accordingly.

Bank and Broker Earnings Beat, But Shareholders Want More

Bank and broker earnings generally beat expectations; however, their share prices retreated. Below is a summary of the major bank and broker earnings:

- JP Morgan: EPS of $4.96, beating estimates of $4.48, with revenue of $44.91 billion against $43.8 billion expected. JPM shares fell due to a weak Net Interest Income (NII) outlook and increasing expenses.

- Citigroup outperformed, reporting an EPS of $1.96 versus the expected $1.60 and revenue of $21.67 billion, compared to the expected $21.0 billion. Furthermore, they boosted their outlook for full-year revenue and NII.

- Wells Fargo posted an EPS of $1.60, topping the $1.41 estimate, and revenue of $20.82 billion, slightly above forecasts. However, its stock fell 5.48% because it trimmed its full-year NII outlook.

- Goldman Sachs reported net revenue of $14.58 billion versus expectations of $13.51 billion. Similarly, its EPS of $10.91 surpassed expectations of $9.59. Equity trading revenues rose 36% to $4.3 billion, and investment banking fees were up 26% to $2.19 billion.

- BlackRock reported a solid Q2, with EPS of $12.05, exceeding the $10.79 estimate, and assets under management (AUM) reaching a record $12.53 trillion. However, it missed slightly on revenue and inflows. The stock fell by 6%

Overall, the biggest players in the financial sector posted good results despite stubbornly high rates. Most benefited from increased trading volumes and IPO activity. However, headwinds from tariff-related concerns, slowing economic activity, and generally cautious forward guidance tempered shareholder optimism. The financial sector, led by the stocks listed above, fell 1.7% yesterday but remains perched near record highs.

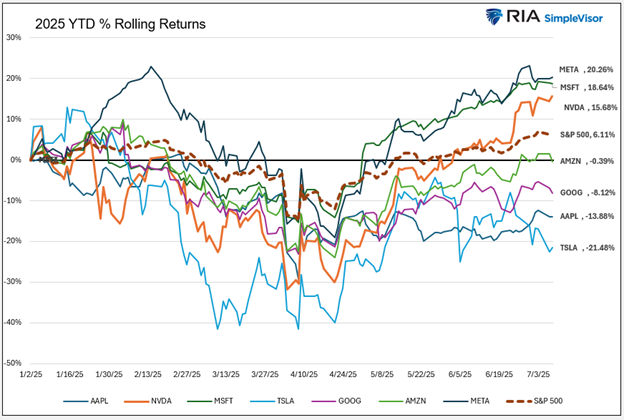

The Magnificent Seven Are Mediocre

Thus far in 2025, the value of the Magnificent Seven strategy is fading. Only three of the Magnificent Seven stocks are among the top ten contributors to the S&P 500. That compares to all seven in 2023 and 2024.

Perhaps the fad is taking a brief hiatus, and the seven stocks will soon regain their lead. Or maybe the trend is shifting.

Given the importance of the seven stocks to the broader market, it’s worth examining them.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.