Quarter Ends Painfully. What Are We Watching Now?

In this 07-02-22 issue of “Quarter Ends Painfully”

- Quarter Ends…Finally. What Next?

- What Are We Watching Now?

- Portfolio Positioning

- Sector & Market Analysis

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Need Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

Schedule your “FREE” portfolio review today.

Weekly Market Recap With Adam Taggart

Quarter Ends…Finally. What Next?

With relief, the quarter-end came after a dismal performance for markets over the last 3-months. The message has been consistent for the quarter to “sell rallies” and “raise cash,” but even with markets deeply oversold, bounces remain short-lived.

For the month, stocks ended lower, adding to the losses already incurred for the year. Last week’s 6.2% surge in the S&P 500 failed at resistance, making that level critical for any serious advance in July.

However, the market did rally on Friday, holding that minor support built over the last three trading days at 3800. While the bounce was certainly welcome, as noted, rallies are quickly met by “trapped longs” looking for an exit.

While July tends to be more bullishly biased, and given the extremely negative sentiment, a “reflexive rally” is undoubtedly due. However, such rallies remain elusive.

From a contrarian view, a bullish rally is needed to lure the “bears” off-sides. There is TOO much bearishness in the market for a bear market to continue. As Bob Farrell once quipped, “when all experts agree, something else tends to happen.”

What is needed is enough of a rally to get Jim Cramer proclaiming a “bear market bottom” is in. A rally strong enough to force “shorts” to cover their index positions will likely provide a more opportune level to reduce equity allocations, raise cash and rebalance risk.

As we discuss below, if a recession is coming, earnings have yet to be revised to compensate for weaker economic growth. If that is the case, then most likely, the market will have to reprice assets lower to adjust valuations for those reduced earnings.

The big question is, what happens after such a dismal quarter-end and one of the worst starts for markets historically speaking?

Worst Start For Markets.

The quarter-end marked one of the worst starts in history for U.S. stocks. Notably, the Nasdaq had the worst start ever to a new year. However, as Chartr noted on Friday:

“The flagship S&P 500 Index declined 20.6% in value, putting 2022 off to the worst start for 52 years, when the index fell 21% in 1970. Before that you have to go back to 1962 when stocks fell 23.5% in the first half of the year — a crash which became known as the Kennedy Slide.

The stock market is not the economy, but investors do try to anticipate what’s coming down the road — and JPMorgan analysts suggested a few weeks ago that the movement in stocks implies an 85% chance that the US economy does go into recession. Some high-profile investors already think we’re in one.

Trying to predict what stock markets do next is a notoriously humbling endeavour, but the historical data is reasonably optimistic. Of the 23 times that stocks have fallen in the first half of the year they’ve gone on to rise in the second half of the year on 12 occasions.” – Chartr

There are a couple of crucial points to note concerning the first-half returns.

The first is while the stock market may NOT be the economy, the economy directly impacts it. Such is because economic activity is where revenue and earnings come from. If a recession comes, stocks will likely be materially lower as stocks have not fully accounted for the coincident reversion in earnings.

If a recession is averted, then markets are likely closer to being fairly valued.

Secondly, the 2002 and 2008 bear markets didn’t end until the Fed cut rates. With the Fed hiking rates, likely exacerbating a recession’s onset, we will err on the side of caution.

The Risk To Investors

Experience is an important teacher. Currently, 31% of investment professionals have never seen a “bear market.”

Due to more than a decade of monetary interventions by the Fed, there has been an extensive adoption of “buy and hold” and “Buy The F***ing Dip” strategies pushed onto retail investors.

Many investors are likely unprepared for the extended period required to recoup previous losses. Following the Dot.com crash, investors did not recoup their lost capital until 2015. As Yahoo Finance concludes:

“Exactly how long it takes stocks to recover bear market losses tends to depend on where we are within a secular, or decades-long, timeframe. After prolonged secular bull markets, such as the two-decade bull of the 1980s and 1990s, a secular bear market tends to follow. These are periods where old market paradigms give way to new ones amid violent portfolio adjustment.”

How long it takes for stocks to recover will ultimately depend on two things:

- A reversal of Federal Reserve monetary policy to zero-interest and monetary accommodation, and

- A reversion of valuations to support lower earnings.

Considering the Fed is likely to commit a policy error, we likely have more work to do as valuations tend to revert below the exponential growth trend line before a bear market is complete.

Powell Admits He Doesn’t Understand Inflation.

This past week, Federal Reserve Chairman Jerome Powell made a startling admission:

“I think we now understand better how little we understand about inflation. This was unpredicted.”

Powell said there is “no guarantee” they can tame runaway inflation without hurting the job market. However, that is their goal.

“That is our aim. We are committed to and will succeed in getting inflation down to 2%. The process is highly likely to involve some pain, but the worst pain is failing to address this high inflation and allowing it to become persistent.”

Considering that the Fed entirely missed the mark on understanding what caused inflation in the first place, it is hard to believe they can contain it without making a policy error. Again.

As we stated previously, the “cause” of inflation was apparent even to non-trained economists. A flood of economic stimulus on a scale not seen since World War II created demand in a shuttered economy unable to provide supply. Such led to an inflationary impulse not seen in a generation.

It requires about 9-months for liquidity to work its way through the economy. Therefore, the reversal of that liquidity will also impact inflation. As we noted in our Daily Commentary (Subscribe for free daily email) this week:

“The Cure for High Inflation is High Inflation. The graph below shows that since 1950, the U.S. has experienced four bouts of significant inflationary periods, as highlighted in red. The prior three periods lasted between 22 and 28 months. The current episode is 25 months old.”

As high prices crush consumer sentiment and force people to reduce spending, weakened demand brings prices down. If history is a guide, we should expect a recession, deflation, and the Fed reversing monetary policy to correct another mistake.

This Week’s MacroView

Earnings Are The Most Wrong During Recessions

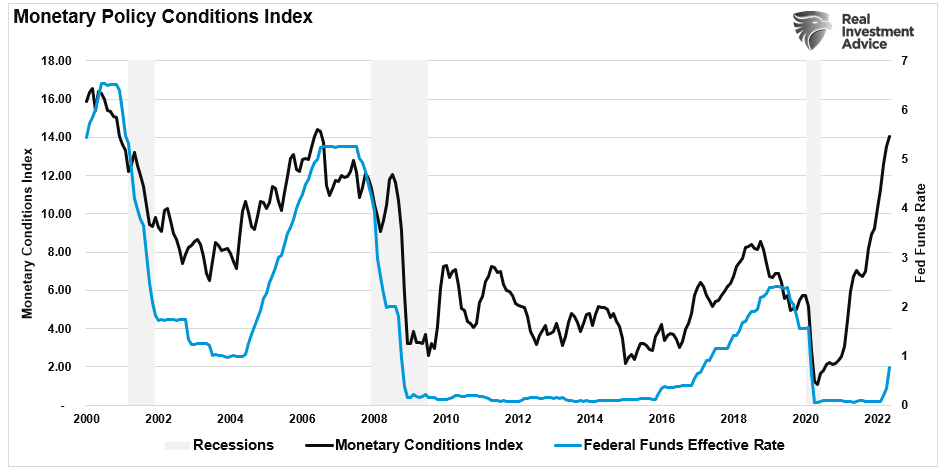

Of course, as the Fed aggressively tightens monetary policy, the drag on consumption from the tighter monetary policy will continue. As we showed last week, the economy’s monetary conditions are already substantially tighter due to higher rates and inflation.

(The index is comprised of short-term rates which impact consumption. Long-term rates which affect capital expenditures and mortgages, and inflation.)

With the Fed hiking rates, such will further drag on economic growth. Of course, since earnings are highly correlated to economic growth, earnings don’t survive rate hikes. As the arrows show, Fed rate increases consistently lead to an earnings recession.

Currently, earnings estimates for stocks are not accounting for much slower economic activity. While the “P” in the valuations (P/E) calculation has declined, the “E” has not. During a recession, earnings tend to fall quite significantly, as noted by Bloomberg:

“Outside of recessions, the black line in the chart doesn’t stray too far from zero. But during recessions, we see that actual earnings are considerably worse than expected ones.“

Such is a problem not only confined to equities. Economic data is typically wrong at major turning points such as recessions. Ironically, though, this is when you need the most clarity. As shown, forward earnings estimates have fallen this year, but if the past is a guide, they are still likely too optimistic.

That also suggests prices have more room to fall to account for a recession if it comes.

Speaking Of Recession

As the quarter ends, we also face quarter-end economic data that will set the tone for the second-quarter GDP report. Unfortunately, the final revision to first-quarter GDP was down, and much of the real-time data has become negative. Such has all fed into economic tracking indicators, suggesting recessionary risks are rising.

With the latest readings from the Chicago PMI, our economic data composite, which precedes economic slowdowns and recessions, turned negative.

Consequently, as a confirming indicator, the Atlanta Fed’s GDPNow tracker also fell into recessionary territory on Thursday.

“The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2022 is -2.1 percent on July 1st, down from -1.0 percent on June 30th.”

For investors, the risk of a recessionary event increases the probability the Fed will pivot from tighter to more accommodative monetary policy as financial instability increases. Such was a point made by Michael Lebowitz this past week:

“The current equity trend is sloping steeply downward. It will likely stay that way until the market thinks the Fed is letting up. At times prices will deviate toward the bottom of the channel and other times towards the top. Trading within the channel can be a valuable bear market trading tool.”

“The Fed is unlikely to become more hawkish than it is today. The question is, when do they start to pivot to a less hawkish policy. At that time, the slope of the red channel is likely to flatten, and a bottoming process can begin.”

We aren’t there yet.

Portfolio Update

With the quarter-end behind us, we can now focus on what the last half of the year may bring. As noted above, market outcomes highly depend on whether we face a recession.

If there is no recession, we are likely closer to a bottom than not. However, a recessionary outcome could push stocks another 20% lower.

As noted last week, bear markets test investors on the way up and down. When the news cycle seems like it can’t get any more horrifying, stocks tend to seize an olive branch. Perhaps it is a reprieve from a hawkish central banker or a drop in sky-high oil prices.

With investor sentiment very negative, maybe that is just the catalyst we need for a reflexive rally that brings the bulls back into the market? As Jim Colquitt at Armor ETFs noted this week:

“It is interesting the degree to which the S&P 500 and VIX are following the 2007 – 2009 narrative. With that said, if the analog continues, we could be in for a fairly decent summer rally.”

While we are hoping for a summer reprieve, this bear market is likely not over yet. As such, we continue to suggest using any rallies to reduce risk and rebalance allocations accordingly. As noted last week, we continue carrying higher cash levels and focusing on risk management for now. There is no easy measure to navigate markets at the moment, but for those who have never been through a bear market, this is just part of the process.

Remain cautious for now. There is no rush to jump into markets trying to speculate a bottom is in. It likely isn’t.

Have a great week.

Market & Sector Analysis

S&P 500 Tear Sheet

Relative Performance Analysis

Technical Composite

The technical overbought/sold gauge comprises several price indicators (RSI, Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. The current reading is 10.86 out of a possible 100.

Portfolio Positioning “Fear / Greed” Gauge

The “Fear/Greed” gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, to more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0 to 100. It is a rarity that it reaches levels above 90. The current reading is 26.75 out of a possible 100.

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares the relative performance of each sector and market to the S&P 500 index.

- “M/A XVER” is determined by whether the short-term weekly moving average crosses positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- The table shows the price deviation above and below the weekly moving averages.

- The complete history of all sentiment indicators is under the Dashboard/Sentiment tab at SimpleVisor.

Weekly Stock Screens

Each week we will provide three different stock screens generated from SimpleVisor: (RIAPro.net subscribers use your current credentials to log in.)

This week we are scanning for the Top 20:

- Relative Strength Stocks

- Momentum Stocks

- Technically Strong With Strong Fundamentals

These screens generate portfolio ideas and serve as the starting point for further research.

(Click Images To Enlarge)

RSI Screen

Momentum Screen

Technical & Fundamental Strength Screen

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

June 27th

“As we enter into the last week of the quarter, we are adding a smidge of trading exposure to portfolios ahead of the $30 billion portfolio rebalancing required by month-end. With many mutual fund managers underexposed equities, and the markets triggering a short-term MACD buy signal, there is some upside to 3900-4000 on the S&P 500 index.

As such, we are adding 5% equity in two trading index positions and increasing exposure to energy by 1% following the rather brutal sell-off recently. These are opportunistic trades that we will sell on a rally, or as needed to reduce equity exposure later on.”

Equity Model

- Buy 2.5% of the portfolio in the Nasdaq 100 Index ETF (QQQ)

- Buy 2.5% of the portfolio into the S&P 500 Equal Weighted Index ETF (RSP)

- Add 1% of the portfolio to build a starter position in Devon Energy (DVN)

ETF Model

- Buy 2.5% of the portfolio in the Nasdaq 100 Index ETF (QQQ)

- Buy 2.5% of the portfolio into the S&P 500 Equal Weighted Index ETF (RSP)

- Add 1% of the portfolio to the SPDR Oil & Gas Exploration ETF (XOP)

Lance Roberts, CIO

Have a great week!