As was widely expected, the Fed left interest rates unchanged. Jerome Powell alluded that it’s much more likely the next Fed move will be rate cuts, not an increase in interest rates. Given the November elections and the internal pressure on the Fed to remain independent, it now seems likely that barring a sharp upturn in unemployment or a renewed decline in prices, rate cuts are not likely this year. The FOMC statement was largely unchanged, but there are two important changes from the prior meeting. First, as highlighted in the first paragraph below, the Fed acknowledges that inflation has become sticky. However, in the second paragraph, they note that supply and demand are in better balance, which should allow for more disinflation.

Second, and more importantly, for the markets, the Fed will start reducing the amount of QT in June. While this was expected based on their FOMC minutes released three weeks ago, the reduction was larger than expected. Further, the entire reduction will be in U.S. Treasury securities, not mortgage-backed securities. This action will help ease market concerns of heavy Treasury debt issuance. During the press conference, Jerome Powell sent mixed messages. While he firmly believes the Fed will meet its 2% inflation goal, they do not want to cut rates too soon. He doesn’t expect to, but they would raise rates if needed. The highlight of the press conference occurred when Powell was asked about stagflation. His reply: “I don’t see the stag or the ‘flation.”

What To Watch Today

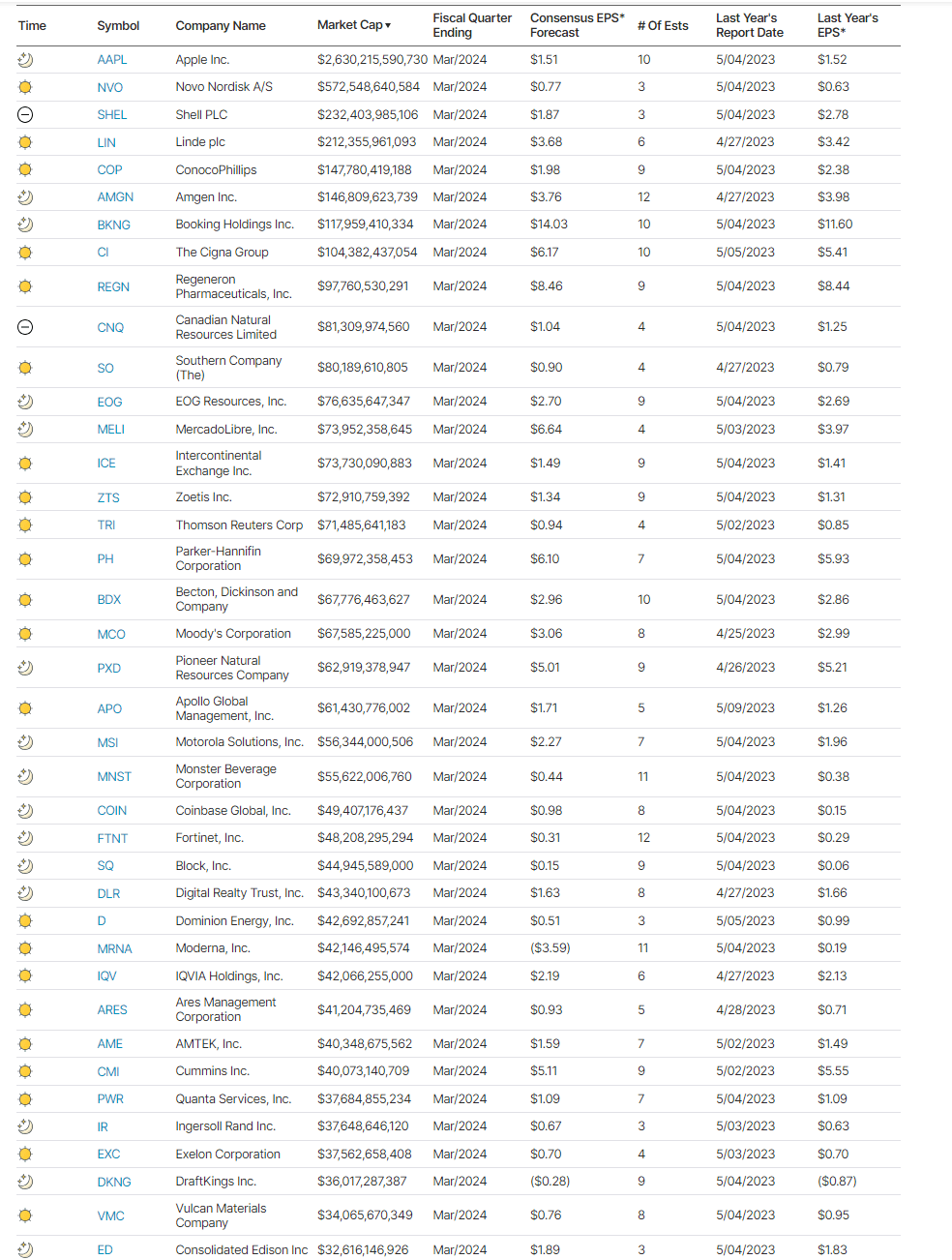

Earnings

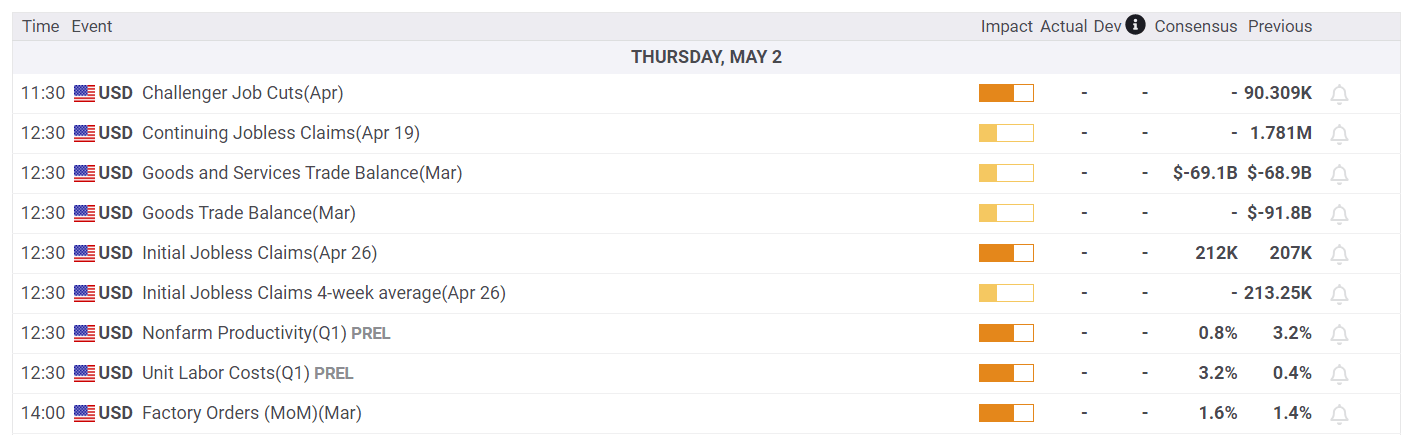

Economy

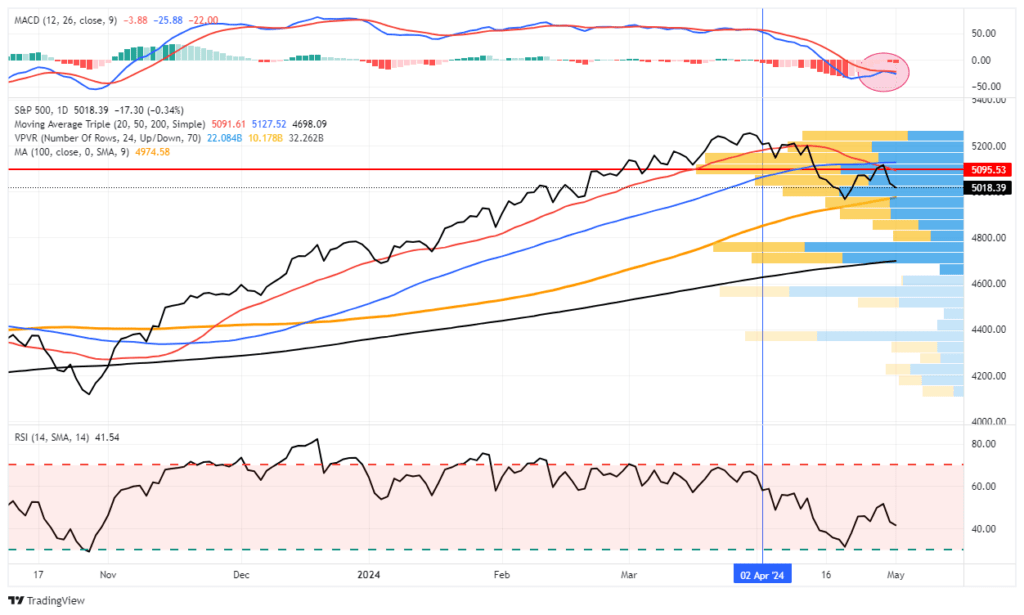

Market Trading Update

Following yesterday’s discussion, the market failed at the 50-DMA and is continuing its correction to retest the 100-DMA. The FOMC meeting concluded its 2-day meeting, and even though rate cuts may not occur this year, the larger-than-expected reversal of Quantitative Tightening (QT) surprised the market. Given that the Federal Reserve is now positioned to start monetizing more debt from the Treasury, it suggests more liquidity for the financial markets and lower yields. As such, stocks and bonds rallied sharply yesterday following the announcement, but day-end sellers emerged, taking away the gain.

There is still likely some near-term downward pressure on stocks, and Apple reports after the bell today, wrapping up the bulk of the earnings season for the S&P 500. Continue to monitor risk accordingly, but with the Fed on hold, stocks will likely find a bottom soon.

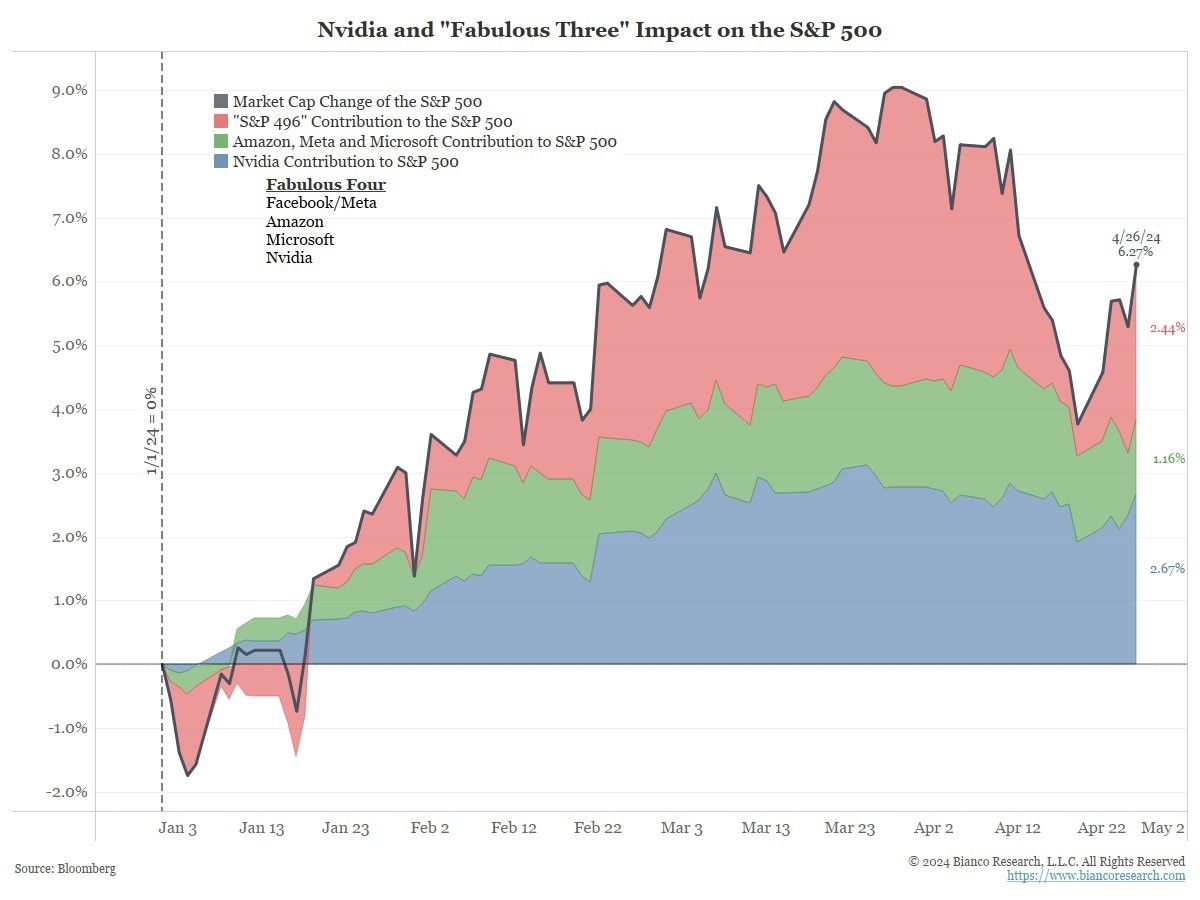

Nvidia And The Fabulous Three

The S&P 500’s market cap was up 6.27% through April 26, as shown by the black line in the graph below, courtesy of Bianco Research. Last year, the Magnificent Seven accounted for almost all of the market gains. This year, the Magnificent Seven is being widdled down to the Fabulous Three and Nvidia. Four stocks account for 62% of the year’s gains. AMZN, MSFT, and META contributed about 19% of the increase in market cap. Nvidia doubles the Fabulous Three, accounting for 38% of the increase. In fact, as shown below, Nvidia single-handedly contributed more to the S&P 500 than the remaining 496 stocks. Nvidia reports its earnings on May 22, a month after most other companies. Accordingly, it has avoided the volatility that has impacted many of the Magnificent Seven stocks this earnings season.

The Dallas Fed Services Sector Bemoans Higher Rates

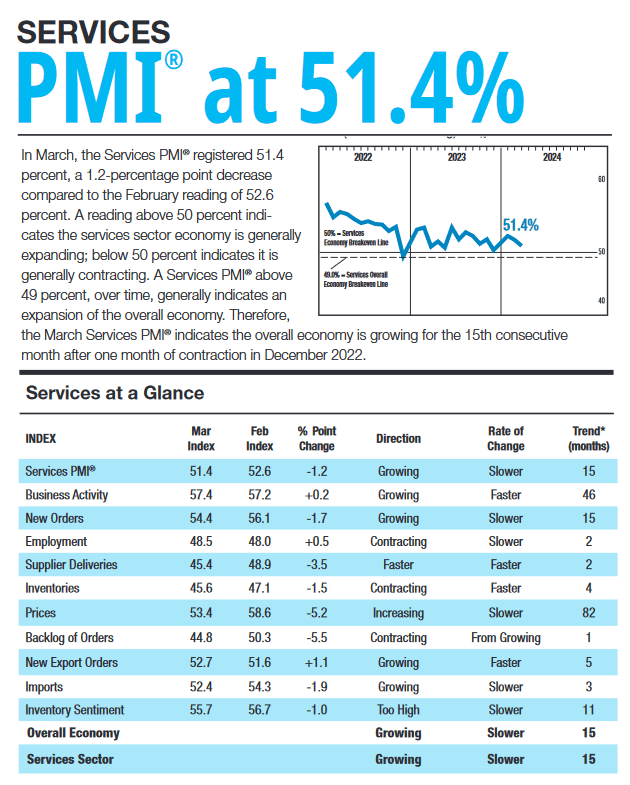

Over the past two years, the service sectors have generally prospered while manufacturing has been in a recession. Recently, manufacturing has shown signs of life, but the service sector is starting to exhibit problems. The service sectors represent almost 90% of the economy. Consequently, the recession in manufacturing did not put the economy into a recession. However, avoiding a recession would be difficult if the service sector struggles. The graphic below shows the March ISM Services survey is still above 50%, an indication of economic expansion. However, the trend is heading toward 50, and a few of its components are below 50.

The most recent Dallas Fed services survey for April indicates that Friday’s ISM services could be weaker than expected. More importantly, it appears that high interest rates are starting to impact the economy negatively. The quotes below, with the respondent’s industry, are from the survey.

Publishing– The impact of the higher rate environment seems to be catching up, with general purchase intent among customers flattening out.

Credit Intermediation– We recently renegotiated our $600 million debt facility. Our cost of funds went from 9 percent to 14 percent—that’s a pretty big hit to our bottom line and resulted in us increasing prices to our customers. Our business focus has been on forecasted easing; however, the reality of rates staying higher longer is creating uncertainty. The Federal Reserve signaling it will hold the rate at the current level for longer has affected our outlook negatively.

Securities– Recent movement in long-term rates, combined with the Fed holding rates longer, have delayed the expected value of investment recovery until 2025 or later.

Real Estate– Cost of capital is weighing on our customers and decreasing volume. The increase in treasury yields since last fall has negatively impacted deal-making activity in the income property industry.

Professional, Scientific and Technical– Persistent inflation and the Fed potentially delaying rate cuts are causing uncertainty for the second half of 2024. This real estate market is hard to figure out. With the 10-year rate still moving in the wrong direction, and the likelihood of a rate cut not coming this year due to inflation and the strength of the economy, we just can’t see the market improving until next year.

Administrative and Support– Continued high interest rates, inflation and general economic malaise has caused employers to be very reluctant to hire professional level talent. High interest rates have drastically hindered our ability to grow our business, and it looks like a rate cut is not likely happening in 2024.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Post Views: 1

2024/05/02