Former U.S. Treasury Secretary Larry Summers spoke strongly to CNBC about the necessity for the Fed to continue its fight against inflation despite recent inflation data. Specifically, Summers is concerned that if the Fed and other central bankers do not stay aggressive, the potential for a second round of high inflation is possible. Per Summers:

The greatest tragedy in this moment would be if central banks were to lurch away from a focus on assuring price stability prematurely and we were to have to fight this battle twice

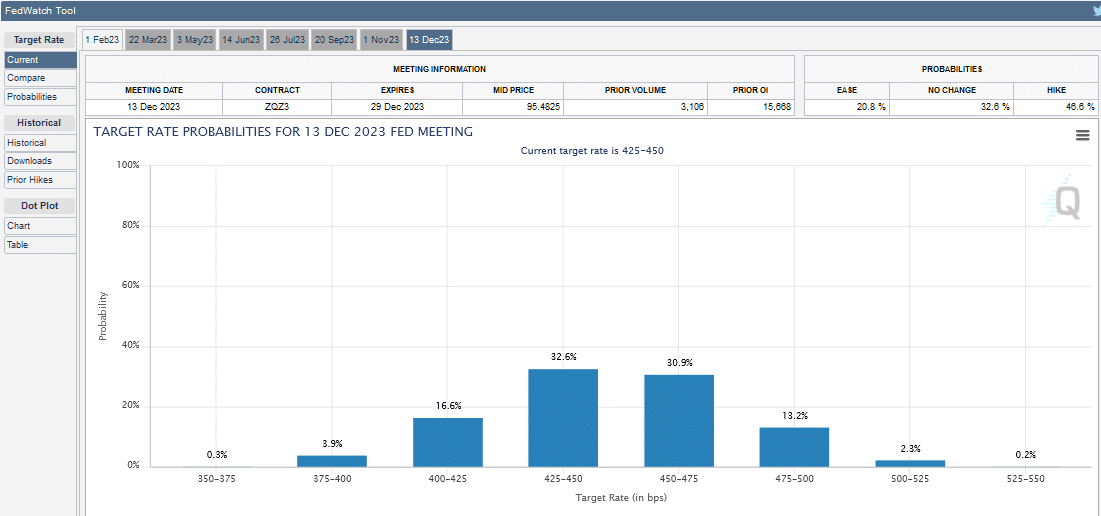

The Fed appears to harbor similar concerns as Summers. Despite inflation peaking and starting to fall rapidly, most Fed members remain very steadfast in their call for higher rates for longer. Fed members are in a media blackout leading to next week’s FOMC meeting. In advance of the blackout this past week, almost all Fed members stressed the need to get Fed Funds to 5% and keep them there for a long time. If the Fed heeds Summers advice, the market is offside. As we share below, the CME FedWatch tool shows Fed Fund futures imply one to two rate cuts by December.

What To Watch Today

Economy

- 10:00 a.m. ET: Leading Index, December (-0.7% expected, -1.0% prior)

Earnings

Market Trading Update

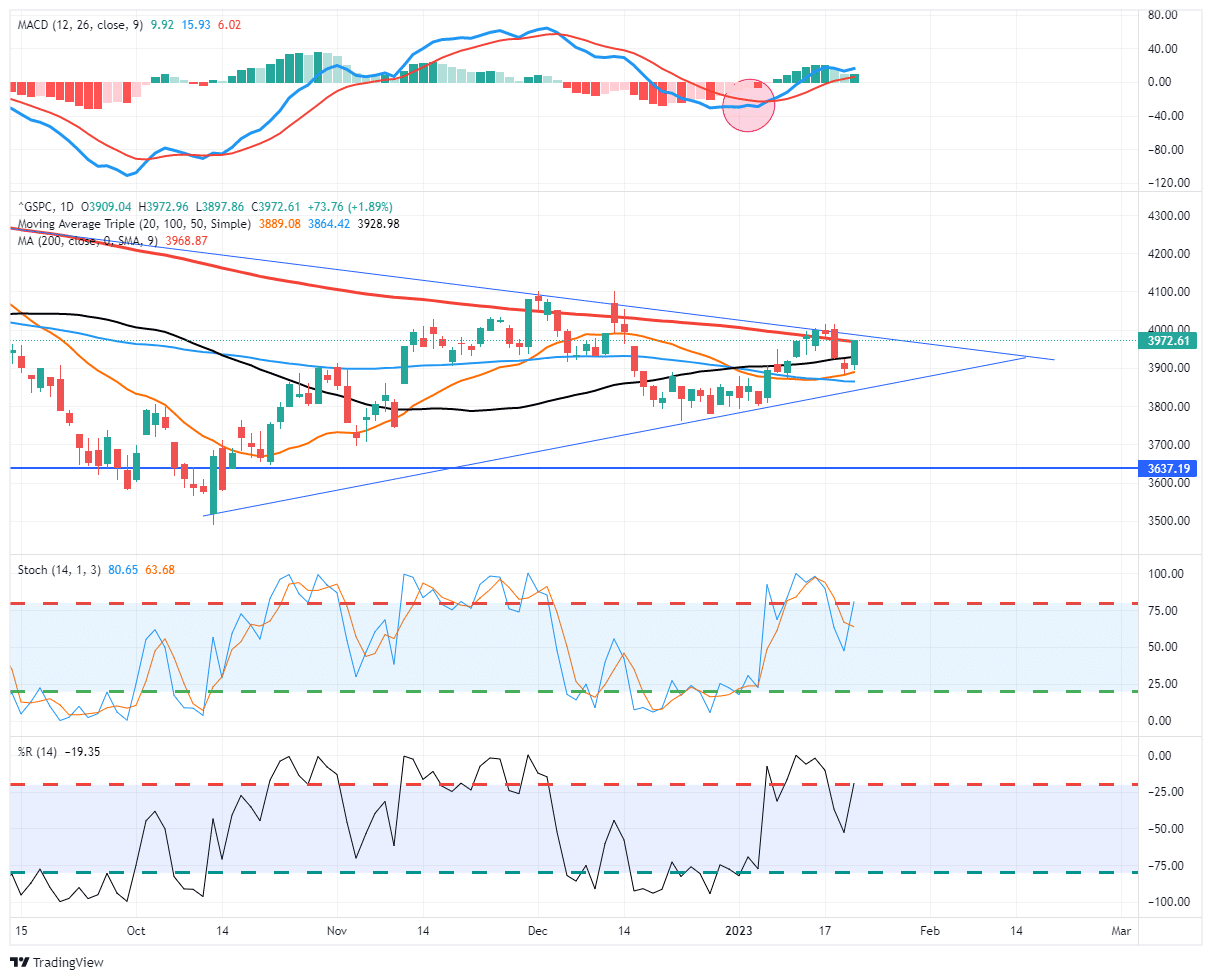

After a brief spat of “Fed” rate hike panic on Wednesday and Thursday, the market surged on Friday to retest the 200-DMA once again. With the correction last week, the market continues to trade within an ever-tighter compression between rising lows and a declining trend line. This pattern will end sooner than later, and, as stated previously, when the market breaks, it will likely be a substantial move.

My best guess is that this market breaks to the upside. However, there is much risk to that call as we head into the FOMC meeting. However, earnings have been decent so far, and outlooks are not as dire as expected (although still pretty bleak), which is giving the markets support. Trade cautiously for now and hold cash. Yes, we will underperform short-term, but once the market breaks out, we will have plenty of time to add exposure and play catch up.

The Week Ahead

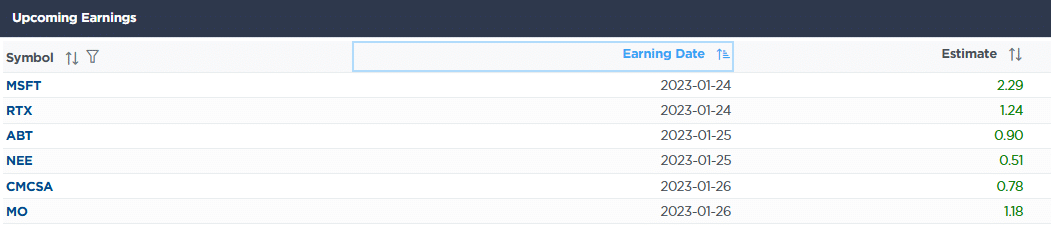

We get a little reprieve from economic data until Thursday and Friday. On Thursday, the BEA will release the Q4 GDP. The current Wall Street expectation is +2.7% annualized growth in the fourth quarter. The Atlanta Fed GDPNow is forecasting 3.5%. Either way, growth was strong last quarter, likely keeping the Fed anxious inflation will be tougher to combat. PCE inflation data will be released on Friday. The price index is expected to increase by 0.1% monthly and 4.6% annually.

The FOMC meets the following Tuesday and Wednesday. Therefore Fed members will be in a media blackout this week.

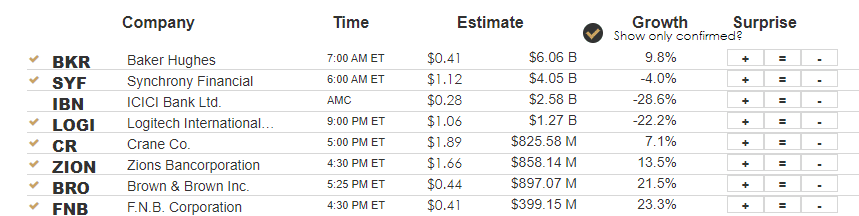

Earnings reports will likely drive the markets. The following table from SimpleVisor shows the earnings expected next week for the holdings of the SimpleVisor Equity Portfolio.

Rent Relief Coming Soon?

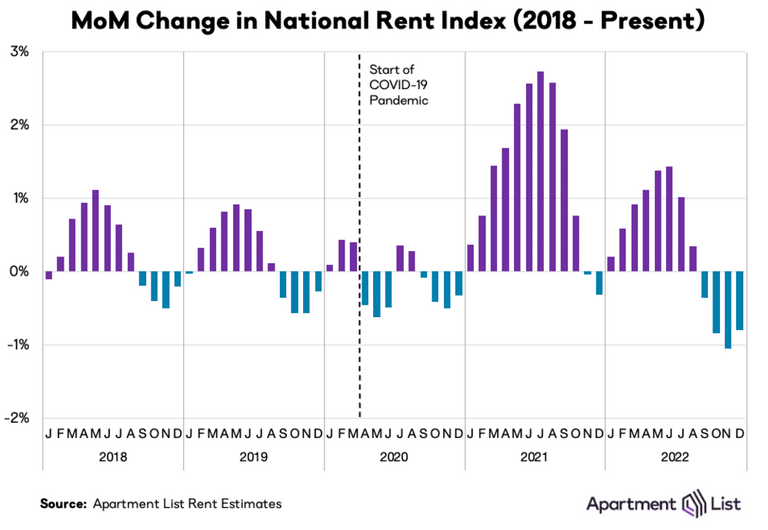

Shelter CPI, predominately rent and implied rent, accounts for about a third of CPI. The recent CPI data point to cooling prices in many sectors except rents. Rental data tends to lag by three to six months, so this CPI input is expected to cool in the coming months, commensurate with real-time rental data. For example, the first graph below, from Apartment List, shows rents have declined in the last four consecutive months. CPI-Shelter has risen between 0.6% and 0.8% monthly in the previous four months.

Looking longer term, there is another reason to suspect rental income may come under pressure. The second graph shows that the number of multifamily units under construction is at a 50-year high. This new supply of apartments will help keep a lid on rents in the coming year or two.

Gold and the Fed

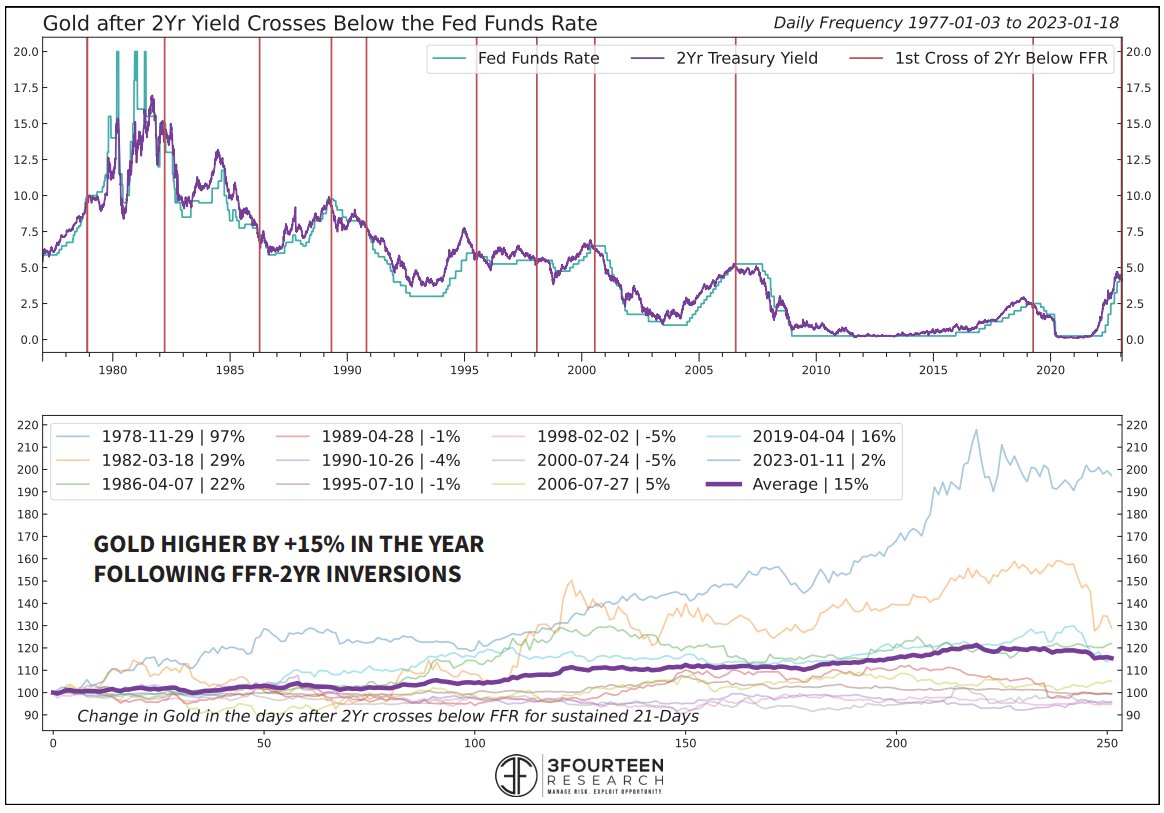

Gold often negatively correlates with real yields. When real yields fall, gold tends to rise and vice versa. Real yields, the difference between bond yields and the expected inflation rate, tend to decline when the Fed moves toward an easier monetary policy. Often the first sign of a Fed pivot from a hawkish policy is when the yield on the 2-year T-bill declines below Fed Funds. That just happened. In the ten times since 1977 that occurred, gold averaged a 15.4% return over the following year. In no case was it down more than 5.3%. Keep in mind the average is skewed higher by the 97% return in 1978. We will release an article on Real Investment Advice in the coming week or two elaborating on the relationship between gold and real yields.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.