Super Micro Computer Inc. (SMCI) was the market’s darling only six months ago. Amazingly, Its stock, had risen 3x in just the first three months of 2024. Consequently, S&P Global announced its addition to the S&P 500 Index. The announcement is annotated below with a box in early March. Furthermore, the circle, which coincides with the peak in Super Micro shares, was the date it started trading in the index. From the day it joined the index to today, it has been a one-way downhill ride for shareholders.

The bad news continued last Friday, with shares already down about 80% from the March peak. Super Micro’s stockholders learned the company could face a liquidity problem. If the company does get delisted from the Nasdaq stock exchange, it could be forced to make holders of its $1.725 billion 2029 convertible bonds whole. Currently, the bonds trade at around 80 cents on the dollar.

Per Yahoo Finance:

A delisting — seen as a real possibility after Super Micro missed an August deadline to file its annual financial report and its auditor resigned — would constitute a spectacular fall from grace for a company which is a major beneficiary of demand for high-powered servers and other hardware to power artificial intelligence.

What To Watch Today

Earnings

- No notable earnings releases

Economy

Market Trading Update

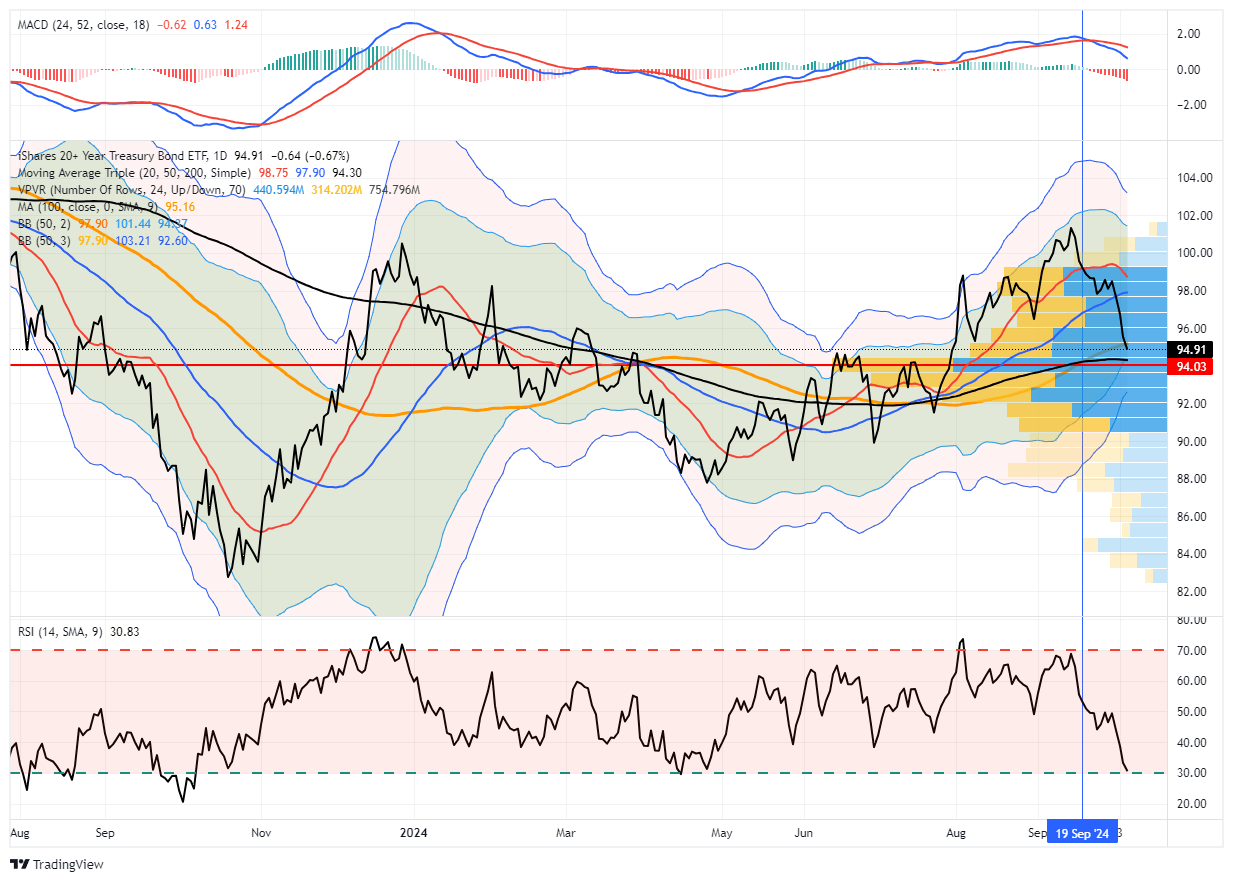

Last week, we discussed the expected derisking heading into an uncertain election.

“There is an important lesson in this week’s action. Over the last several weeks, we have warned about the weakening of momentum and relative strength and the triggering of the MACD ‘sell signal.’ However, many followers commented that the market kept rising despite my warnings and “this time was different.” The lesson is that while technical analysis is NOT perfect, the signals derived from the analysis are often a good process to follow. As always, “timing” is the most difficult challenge. The indicators told us that the market would likely “derisk” before the election, which is now evident.“

With the election over and the Federal Reserve cutting the overnight lending rate by another 25bps, many of the headwinds the market was hedging for are now behind us. As a result, the market surged higher, hitting our year-end target of 6000 on Friday. Furthermore, since election day, the “RE-risking” rally reversed the short-term sell signal, supporting higher prices. As we stated over the last few weeks, despite the many media-driven narratives, the underpinnings of the market remained bullish, suggesting the recent pullback to the 50-DMA was a buying opportunity.

Of course, much speculation exists about what will occur under a Trump presidency. Here is our short take.

The potential economic and market impacts are based on continuing pro-business policies and tax reform, likely involving further corporate tax cuts to boost growth and incentivize domestic investment. The regulatory environment would remain business-friendly, with potential rollbacks in areas like environmental restrictions and financial oversight to foster economic expansion.

Trump would likely maintain an aggressive stance on trade, particularly toward China. This could mean higher or expanded tariffs, which may negatively impact global trade flows and supply chains but benefit select U.S. industries like steel and manufacturing. Those tariffs could lead to heightened market volatility, at least initially. The resulting trade tensions and a “tit-for-tat” policy response could pose problems. However, certain sectors, such as energy, defense, and traditional manufacturing, could benefit from Trump’s policies, while technology and companies heavily reliant on international markets might face challenges.

Immigration policies would likely tighten further under Trump, potentially affecting labor markets and sectors dependent on foreign workers, such as agriculture and technology. The risks of restricting the labor pool are unknown. Still, they could have mixed economic effects, potentially raising wages for some domestic workers but increasing costs for industries reliant on lower-wage labor.

Given those concerns, it is undoubtedly worthwhile continuing to manage risk. While the backdrop is near-term bullish for stocks, it doesn’t mean there will not be corrections along the way.

The Week Ahead

Inflation data will headline economics this week, with CPI on Wednesday and PPI on Thursday. Accordingly, the current consensus is for CPI to increase by 0.2%, bringing the year-over-year rate to 2.6% from 2.4%. Thus, the expected shift higher in the yearly rate is a function of a low CPI rolling out of the 12 month calculation.

Import and export prices on Friday will further inform us of recent inflation trends. Retail Sales on Friday will provide some insight into personal consumption habits heading into the holiday season. However, bear in mind the two hurricanes likely affected the data.

We are looking forward to hearing from Fed members this week. Accordingly, we would like to hear about their views on the recent increase in interest rates, the Trump presidency, and their outlook for Fed policy in 2025. Hints that QT could be near an end would not be surprising.

Quick Thoughts On The Trump Presidency

The prospect of a Trump presidency has led to much debate and speculation about how markets might react. Depending on what policies he can pass, there are potential risks and opportunities in both the stock and bond markets. While the market surged immediately following the election, many potential future headwinds may impact returns from economic growth, monetary and fiscal policy, and geopolitical events.

Therefore, here are some quick thoughts about what we at RIA Advisors think about the stock and bond markets in 2025.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Post Views: 0

2024/11/11