Inside This Week’s Bull Bear Report

- Technical Bounce On Inflation Data

- How We Are Trading It

- Research Report – Investor New Year’s Resolutions

- Youtube – Before The Bell

- Market Statistics

- Stock Screens

- Portfolio Trades This Week

Administrative Note

I am publishing the report a day early as we are holding our Economic and Investment Summit tomorrow morning. As such, all the data in this report is either as of Thursday’s close or early Friday morning. Therefore, any erroneous conclusions will be corrected in Monday’s Daily Market Commentary.

The newsletter will return to its normal schedule next week.

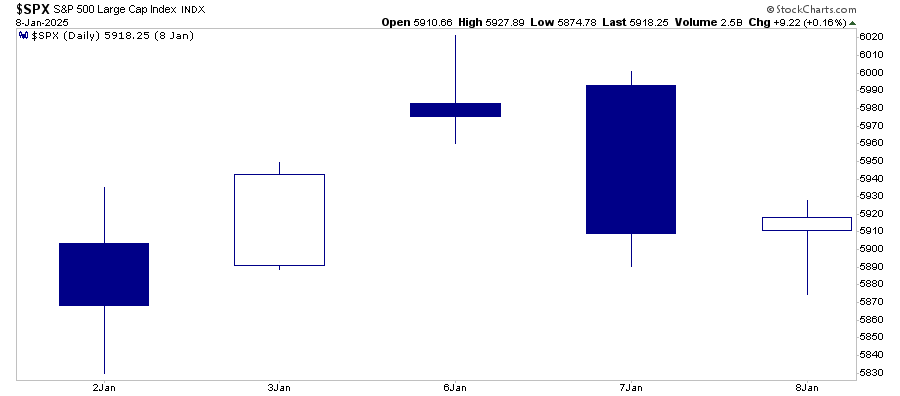

January Back To Positive

Last week, we noted that while closely watching how the full month of January will turn out, we did generate a positive return during the first five trading days.

“As of Wednesday, which concluded the first five trading days of January, that market did generate a positive return, rising about 0.62%”

As discussed, that was the first of two “January Indicators” that have historically, on average, set the tone for the year.

“Since 1950, the S&P 500 has logged net gains during the first five days of the year 47 times. Of those 47 instances, the index ended the year up in 39 of them. That’s an 83% success rate for the first five-day theory. However, don’t get too excited. Of the 74 completed years since 1950, the S&P 500 has logged a full-year gain 73% of the time. That is likely because stocks are rising as the growth of the global economy continues despite the occasional stumble.”

However, following the first five days, the market stumbled to test support at the 100-DMA. As we noted in last week’s newsletter:

“Amost every sector and market, except for Healthcare and Energy, are deeply oversold. This suggests that we will likely see a decent market rally over the next week to rebalance portfolio risks. A weaker-than-expected inflation print or other soft economic data will likely provide the catalysts for the rally.”

Such is precisely what happened with the technical bounce in the market following Wednesday’s inflation report. As of 11 a.m. CST Friday, the market broke above several resistance levels, including the 20 and 50-DMA and the downtrend resistance from the December highs. That technical bounce and break of the downtrend clears the way for a potential retest of those market highs. Furthermore, on the bullish side of the ledger, that technical bounce has reversed the MACD “sell signal” and improved overall relative strength, which should support a rally into next week.

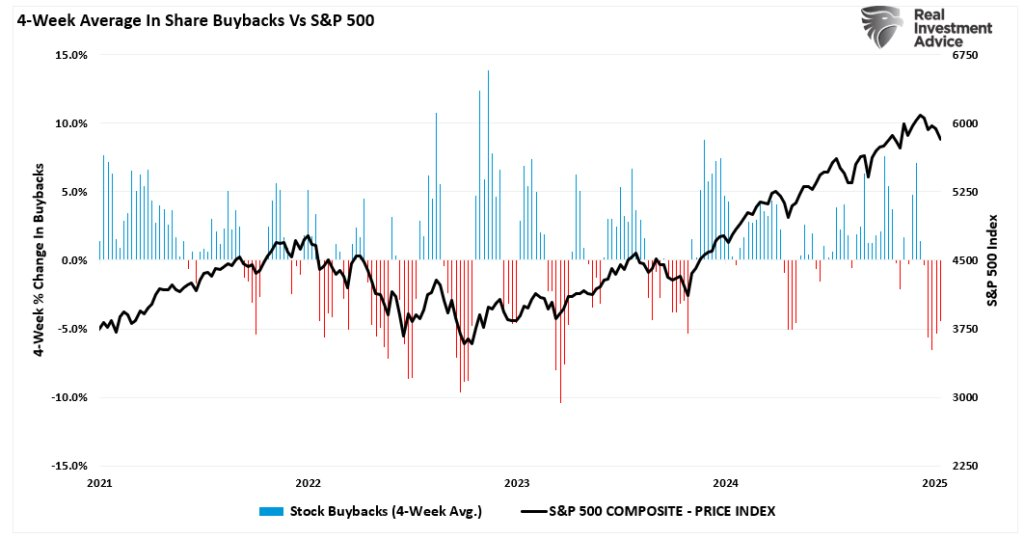

While the recent rally is a positive, we are not likely past the recent increase in volatility. There remain numerous concerns ahead for the market, but in the near term, markets will be supported by the return of share buybacks as we progress further into the Q4 earnings season. Such was a point I made Friday morning on “X.”

“Speaking of share buybacks, in today’s trading update I published the following two charts showing the correlation between the ebbs and flows of buybacks vs the market. Given we have been in a blackout period over the last few weeks, the market weakness was unsurprising. In 2025, the market is expected to set a record of $1 Trillion in repurchases.”

We should continue to manage risk accordingly, but the near-term correction since the beginning of the year is likely over for now.

This week, we will discuss the latest inflation report that supported the technical bounce in the market.

Need Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

Inflation Concerns Remain Unfounded

The market has struggled over the last two weeks as bond yields have surged sharply over fears of a resurgence of inflation and tariffs under the Trump Administration. First, as a reminder, the fears of “Trumpflation” are likely well overstated.

“Many mainstream economists and analysts believe President Trump’s economic policies could trigger “Trumpflation.” The term refers to potential inflation driven by his administration’s fiscal and trade policies. Analysts suggest that extending the TCJA tax cuts, further tax cuts, infrastructure spending, or increased military budgets will boost economic growth and lift inflation. The belief is that this fiscal stimulus, especially during an already low unemployment environment, would increase demand, leading to price increases.

Furthermore, “Trumpflation” could be triggered by introducing trade protectionism and tariffs. Economists argue that restricting imports and raising tariffs on foreign goods will lead to higher domestic prices, as the costs of imported goods would rise. Combined, these policies pointed to risks of higher consumer prices and potentially higher interest rates.

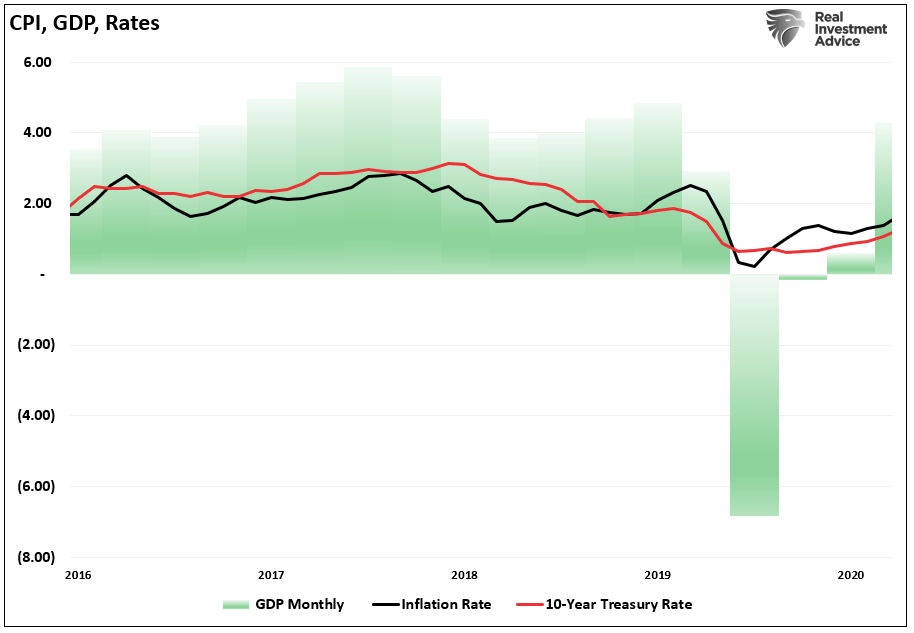

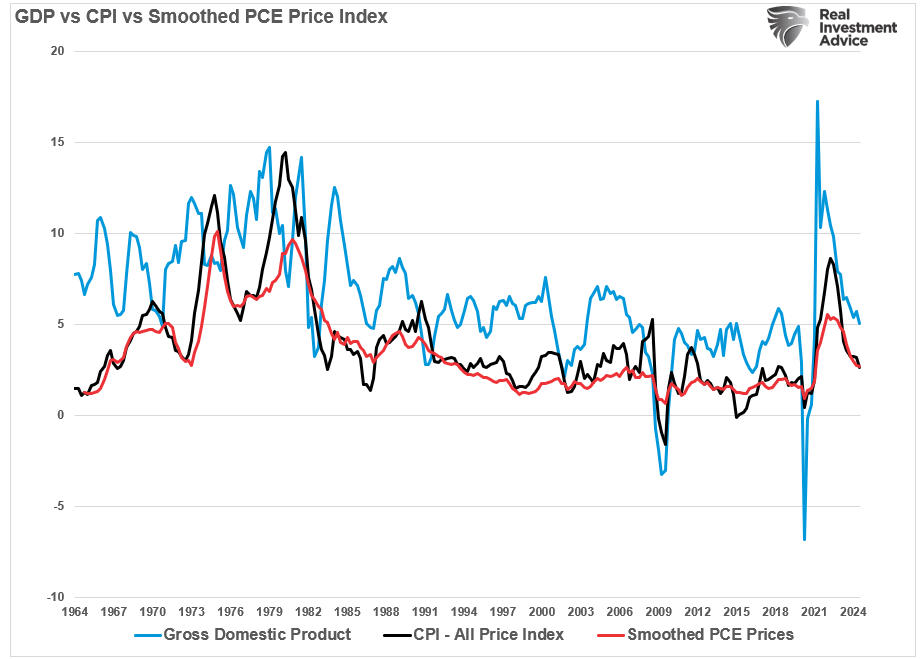

The advantage that we have today is that we can review President Trump’s first term to see if the same policies instituted then led to higher interest rates and inflation. Following his election in 2016, he instituted tariffs on China, cut taxes, and passed regulations that preceded less immigration and increased business investment. The chart below shows his first term’s economic growth, inflation, and interest rates. (Note: The chart below begins on November 1, 2016, and ends on January 20th, when President Biden took office.”

What is crucial to note is that while Trump’s policies led to more robust nominal economic growth (as measured by GDP), inflation and interest rates remained range-bound to roughly 2%. That is until the pandemic arrived in early 2020, which led to a collapse in both rates and inflation.

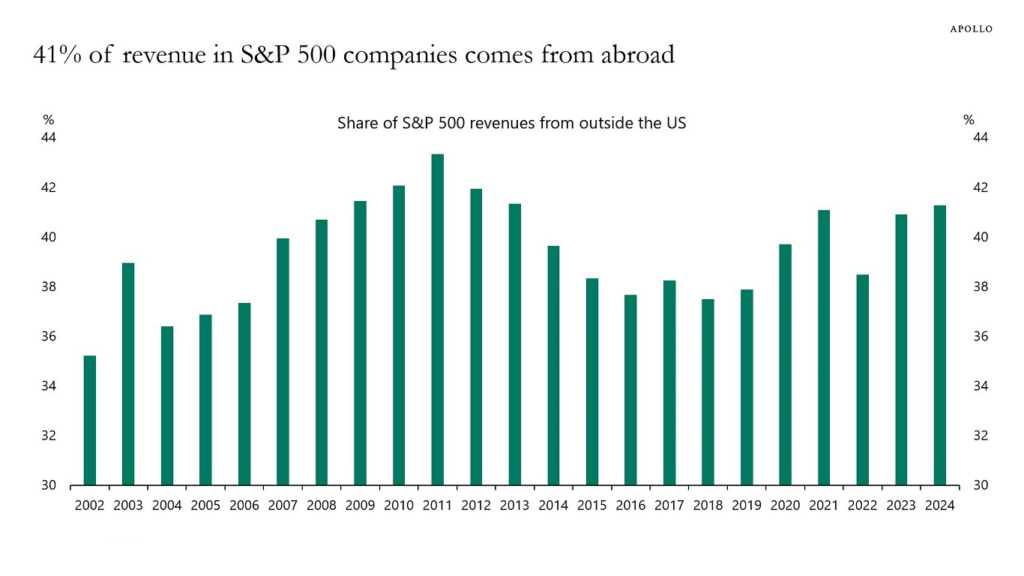

Could this time be different? Sure. However, given that 41% of corporate revenues are derived from international trade, anything increasing international consumers’ costs will negatively impact U.S. economic growth.

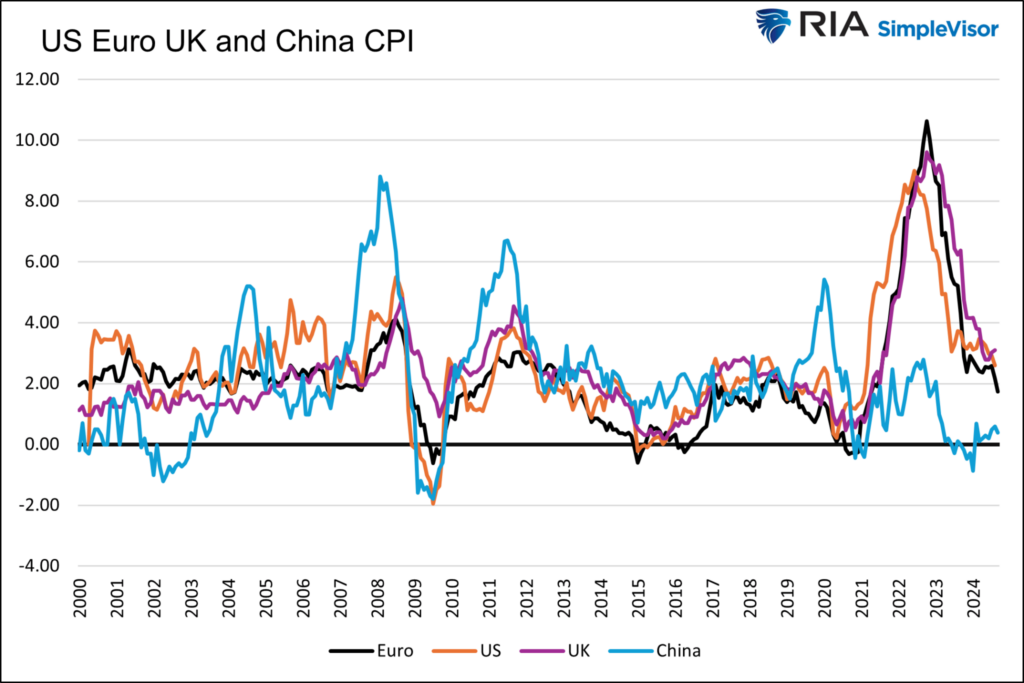

The International Monetary Fund (IMF) has projected a slowdown in global growth over the next year. Tighter financial conditions, a strong dollar, tariffs, and geopolitical uncertainties will drive that decline. A cooling global economy reduces demand for raw materials and commodities, which helps keep inflation in check. Lower import prices from trading partners can also help dampen domestic inflation. The U.S. benefits from cheaper imports if major economies like China and the European Union experience slower growth. As Michael Lebowitz recently wrote:

“Some say we will import inflation. The graph below shows inflation in the Eurozone, China, and the U.K., three of our largest trading partners. Inflation is falling alongside that of the United States. China’s inflation is near zero. Japan, not shown, has seen meager inflation with bouts of deflation for the last 25 years.”

Understanding these dynamics suggests that “Trumpflation” is likely much less of a concern than the media suggests.

Latest CPI Data Remains Contained

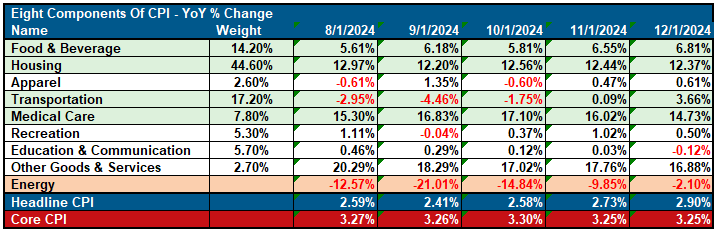

Secondly, the latest Consumer Price Index (CPI) showed inflationary pressures remain contained, with a strong technical bounce in the markets acknowledging this. On Wednesday, the CPI headline report aligned with expectations, rising 0.4%, with core CPI coming in at just 0.2%. Here is a breakdown of the CPI report over the last five months.

Note that “housing,” the most significant contributor to the index, has declined over the last two months as real-time rental rates continue deflating in that sector.

Furthermore, medical costs (healthcare) also showed a second monthly decline. Food and Apparel showed modest increases, which is unsurprising given the holiday season, with the only outlier being transportation. However, the transportation component was impacted by both holiday travel and replacement vehicles from North Carolina and Florida floods. We will likely see continued pressure on used car prices as replacements start for the California wildfires. However, these are temporary anomalies that drag forward future consumption.

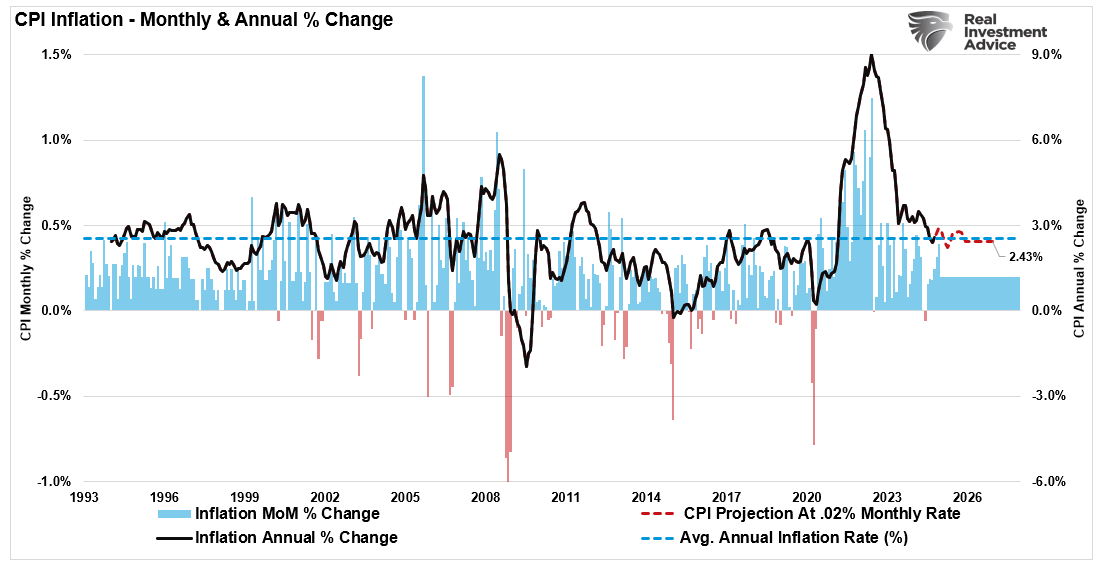

Given those inputs, inflation’s “stickiness” has been evident in recent months, putting the markets on edge about future Fed rate cuts. However, while inflation may remain stuck here for a while longer, the eventual economic dynamics will continue to drag inflation toward the Fed’s goal of 2%. If inflation reverts to just 0.2% monthly increases, the annual inflation rate will fall to 2.4% by the end of 2025. If the economy slows further, as expected, the inflation rate will decline closer to 2%. Given that inflation is never “stable” or “sticky,” a sharper decline of inflation due to economic weakness is far more likely than a strong advance or a “new paradigm.”

That expectation is supported by declining real wages, which are underperforming inflation.

Given that wages are crucial for economic consumption (with spending comprising nearly 70% of GDP), the decline in wages impacts the growth rate of Personal Consumption Expenditures (PCE). The correlation between PCE and GDP is extremely high, suggesting that inflation will decline in the months ahead UNLESS something increases incomes and household consumption rates, such as another round of stimulus checks sent directly to mailboxes.

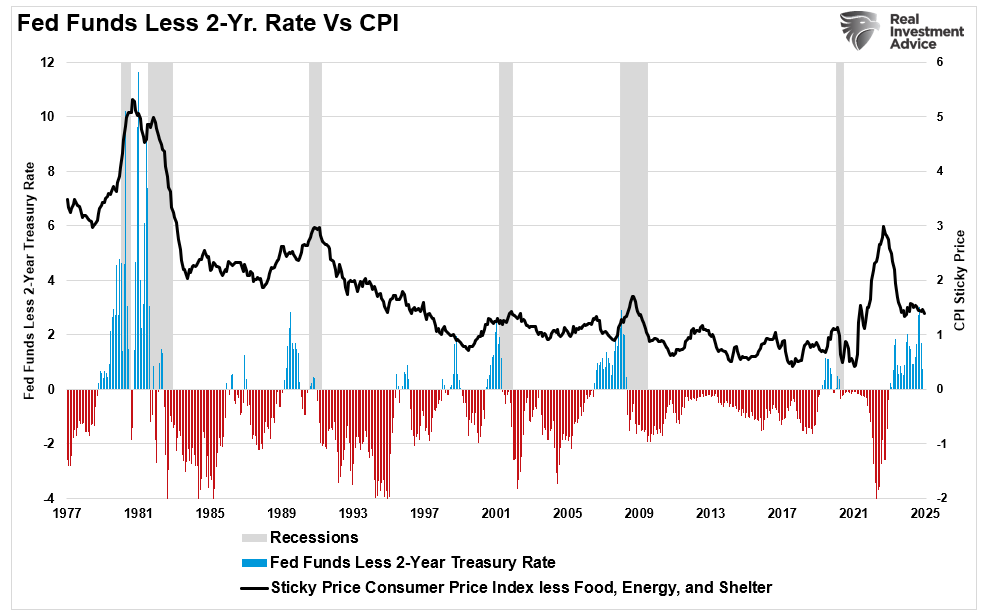

As inflation slows, the Fed will continue to reduce interest rate policy to align interest rates with economic growth and “sticky” inflation. Such is shown in Fed Funds’ deviation above the sticky CPI rate. That reversal of interest rate policy will continue to support technical market bounces on hopes of further rate cuts in the future.

Technical Bounce Or Something More Or Less

While the debate over inflation will continue for a while longer, the market will likely continue to jump from short-term corrections to technical bounces throughout this year. As discussed in “Tactically Bearish.” higher interest rates threaten an overvalued and overly optimistic market.

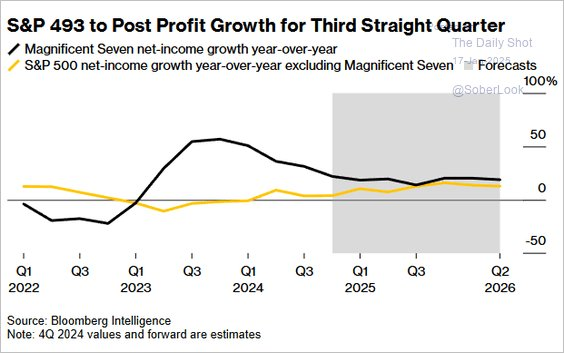

With the Q4 earnings season underway, analysts are optimistic that profit growth from last year will continue this year. More notably, they expect profit growth to slow for the largest U.S. corporations but increase for the rest.

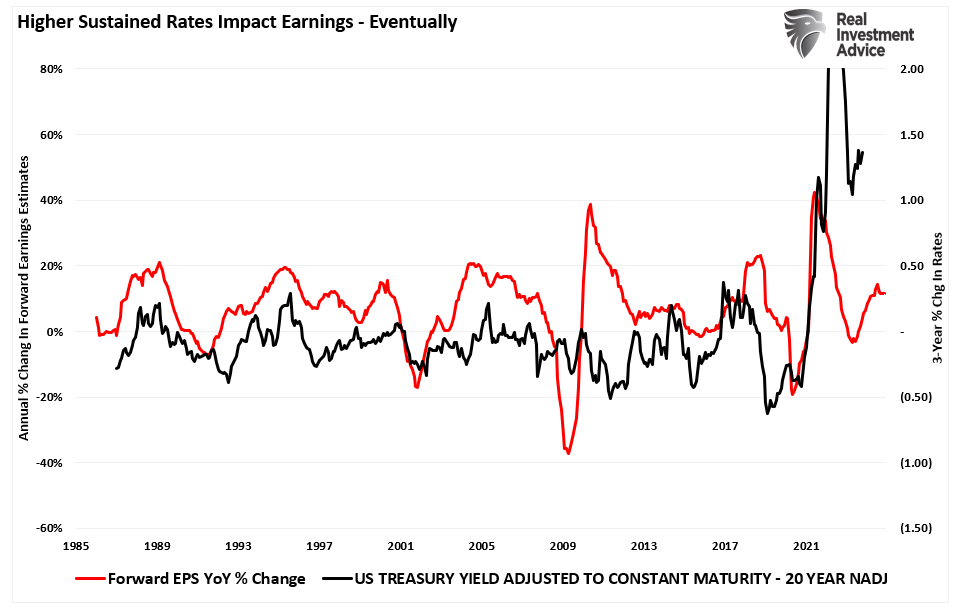

However, they may be a hitch in the optimism. As shown, interest rates are a function of economic growth and inflation. Inflation is a byproduct of economic growth. Despite falling interest rates and stable economic growth last year, the bottom 493 companies failed to grow profits strongly. With interest rates rising, it will be more difficult for smaller companies more sensitive to economic weakness to expand profit growth and earnings. Such is because higher rates negatively impact corporate earnings as borrowing costs increase. Therefore, while rising interest rates do not immediately impair earnings growth, eventually, they do as economic growth slows.

Lastly, valuations are a function of earnings growth and investor sentiment. Therefore, rate increases pose a significant threat if earnings growth becomes impaired due to higher costs and slowing economic demand. Historically, rising interest rates have triggered more significant mean reverting events. This is because investors must reprice assets for lower expected earnings growth rates. With valuations at the highest level since the stimulus-induced frenzy in 2021, the risk of a reversion has increased. Such is particularly true if Wall Street’s bullish forecasts fail to become reality.

While valuations are a terrible market timing tool in the short term, they tell us much about future growth. The earnings growth rate needed to continue justifying current multiples will be much harder to achieve at current levels.

How We Are Trading It

As discussed in “Curb Your Enthusiasm,” investors should likely consider approaching 2025 with an increased risk-managed approach. While current bullish optimism faces challenges, the solution is not abandoning the market altogether. Instead, investors can take practical steps to navigate these uncertainties.

I published our annual “gardening guide” on Friday and linked it below for better investing outcomes. While you should read the entire article for full context, here are the following tenets.

To have a successful and bountiful garden, we must:

- Prepare the soil (accumulate enough cash to build a properly diversified allocation)

- Plant according to the season (build the allocation based on the current market cycle.)

- Water and fertilize (add cash regularly to the portfolio for buying opportunities)

- Weed (sell losers and laggards; weeds will eventually “choke” off the other plants)

- Harvest (take profits regularly; otherwise, “the bounty rots on the vine”)

- Plant again according to the season (add new investments at the right time)

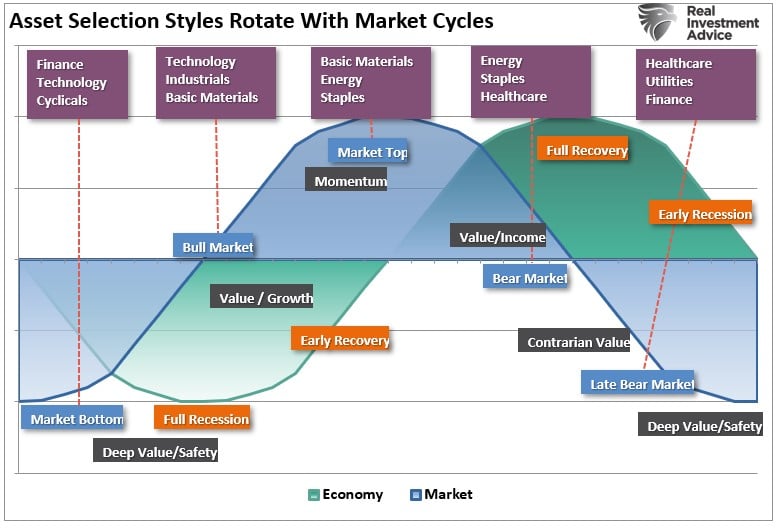

Like everything in life, there is a “season” and a “cycle.” When it comes to the markets, “seasons” are dictated by the “technical and economic constructs,” and the “cycles” are dictated by “valuations.” The seasons are shown in the chart below.

Investing in 2025 will require a blend of optimism and caution. With slowing economic growth, fiscal policy uncertainties, global challenges, overconfident sentiment, and ambitious earnings expectations, investors have plenty of reasons to approach the markets carefully. There will be a time to raise significant cash levels. A good portfolio management strategy will ensure exposure decreases and cash levels rise when the selling begins.

It is essential to take advantage of bullish advances while they last. Don’t become overly complacent, believing, “This time is different.”

It likely isn’t.

Feel free to reach out if you want to navigate these uncertain waters with expert guidance. Our team specializes in helping clients make informed decisions in today’s volatile markets.

Have a great week.

Research Report

Subscribe To “Before The Bell” For Daily Trading Updates

We have set up a separate channel JUST for our short daily market updates. Please subscribe to THIS CHANNEL to receive daily notifications before the market opens.

Click Here And Then Click The SUBSCRIBE Button

Subscribe To Our YouTube Channel To Get Notified Of All Our Videos

Bull Bear Report Market Statistics & Screens

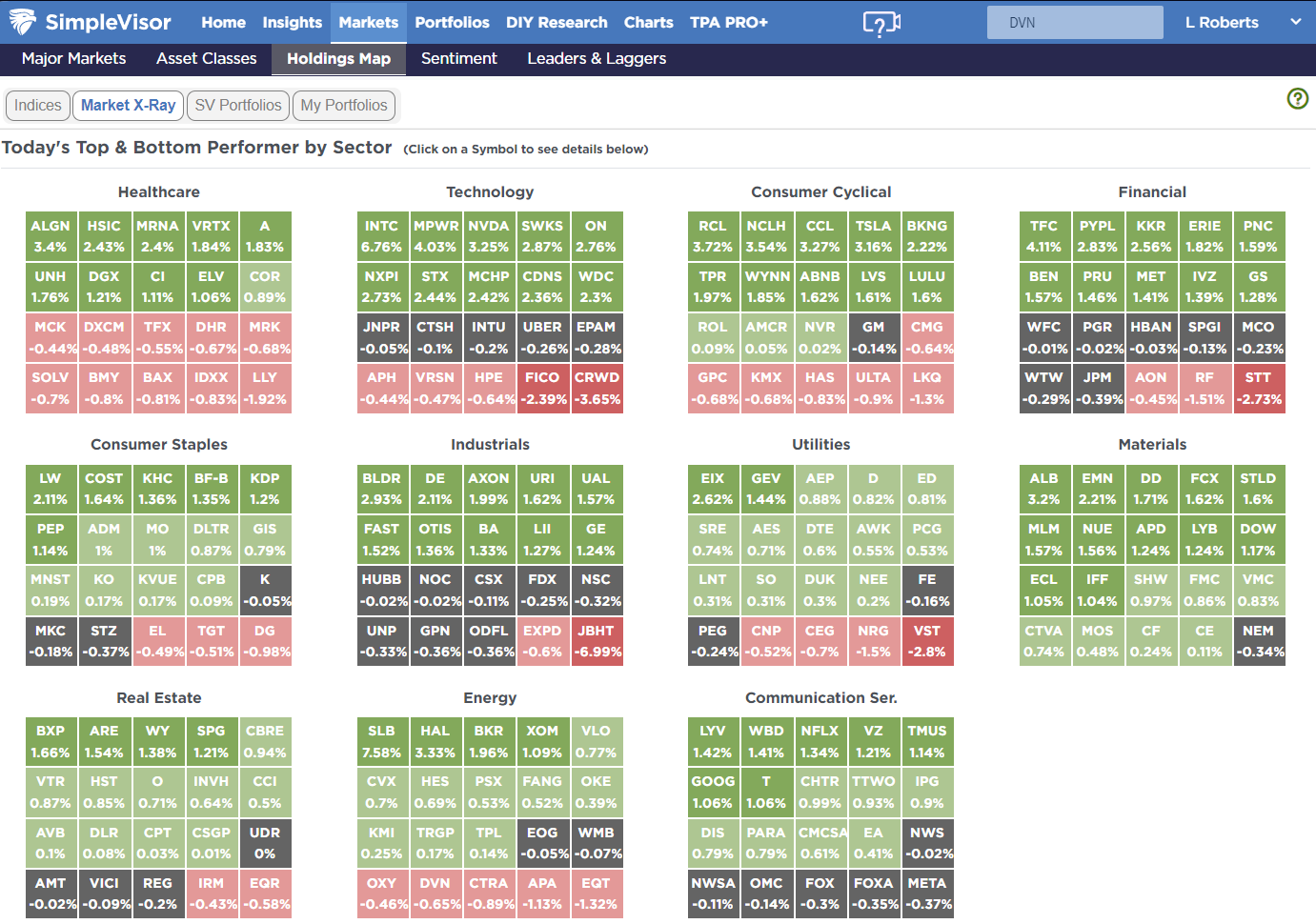

SimpleVisor Top & Bottom Performers By Sector

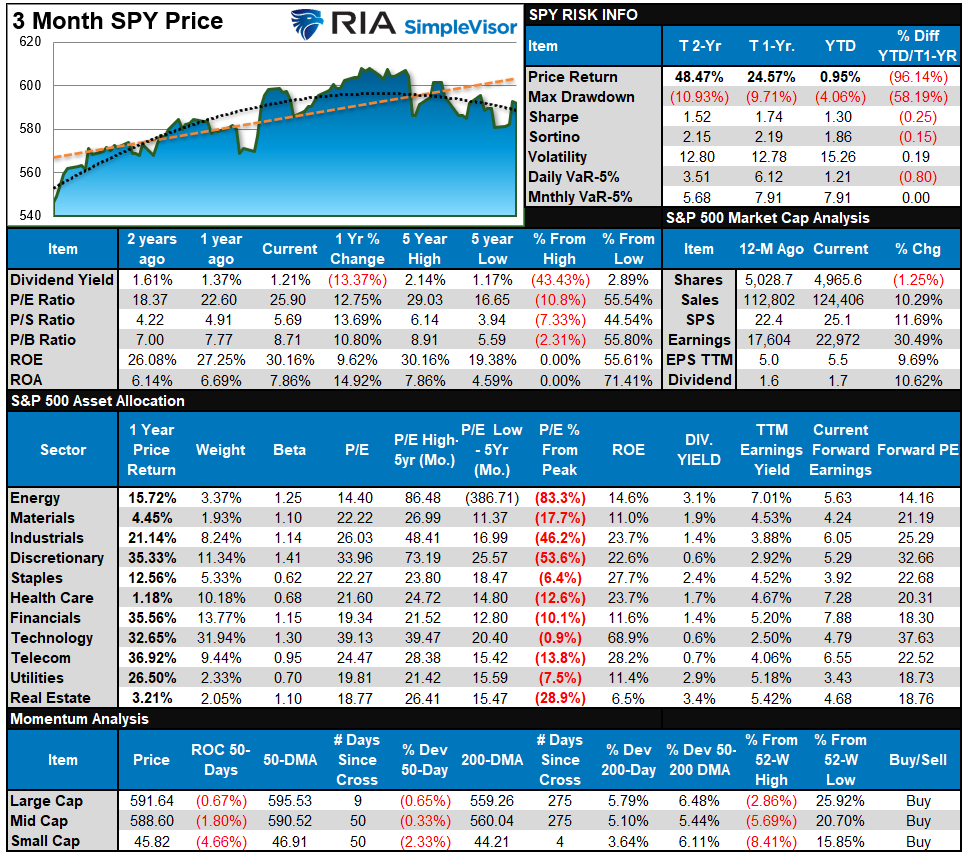

S&P 500 Weekly Tear Sheet

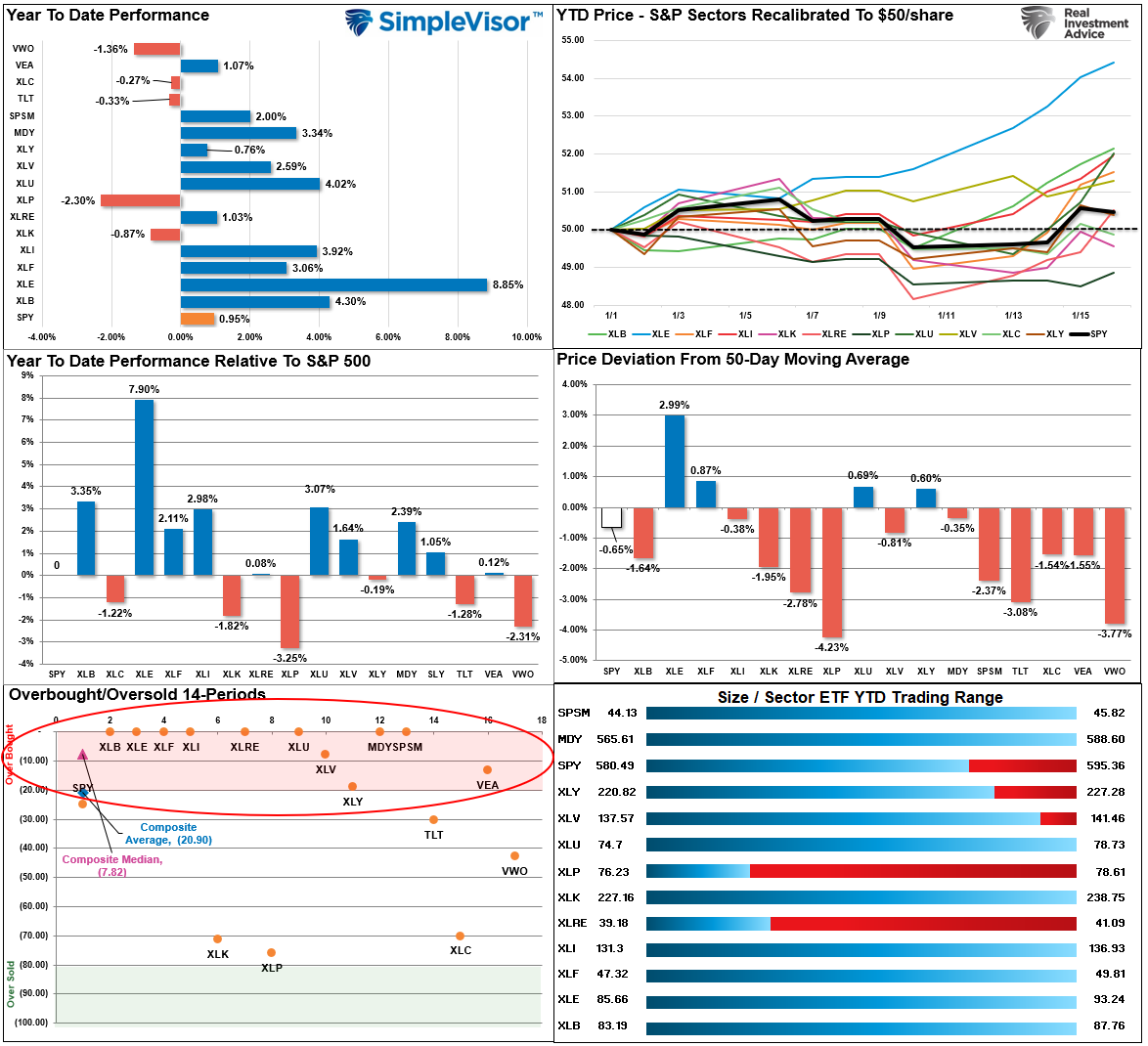

Relative Performance Analysis

In last week’s newsletter, we noted that the market was extremely oversold, slipping almost 1% for the year.

“As shown in the bottom left panel, almost every sector and market, except for Healthcare and Energy, are deeply oversold. This suggests that we will likely see a decent reflexive rally over the next week to rebalance portfolio risks. A weaker-than-expected inflation print or other soft economic data will likely provide the catalysts for the rally.”

Such is precisely what happened, and that furious rally has now reversed the majority of that previous oversold to overbought. Use this rally to rebalance risks as needed, as we are likely not fully past the recent volatility we have seen.

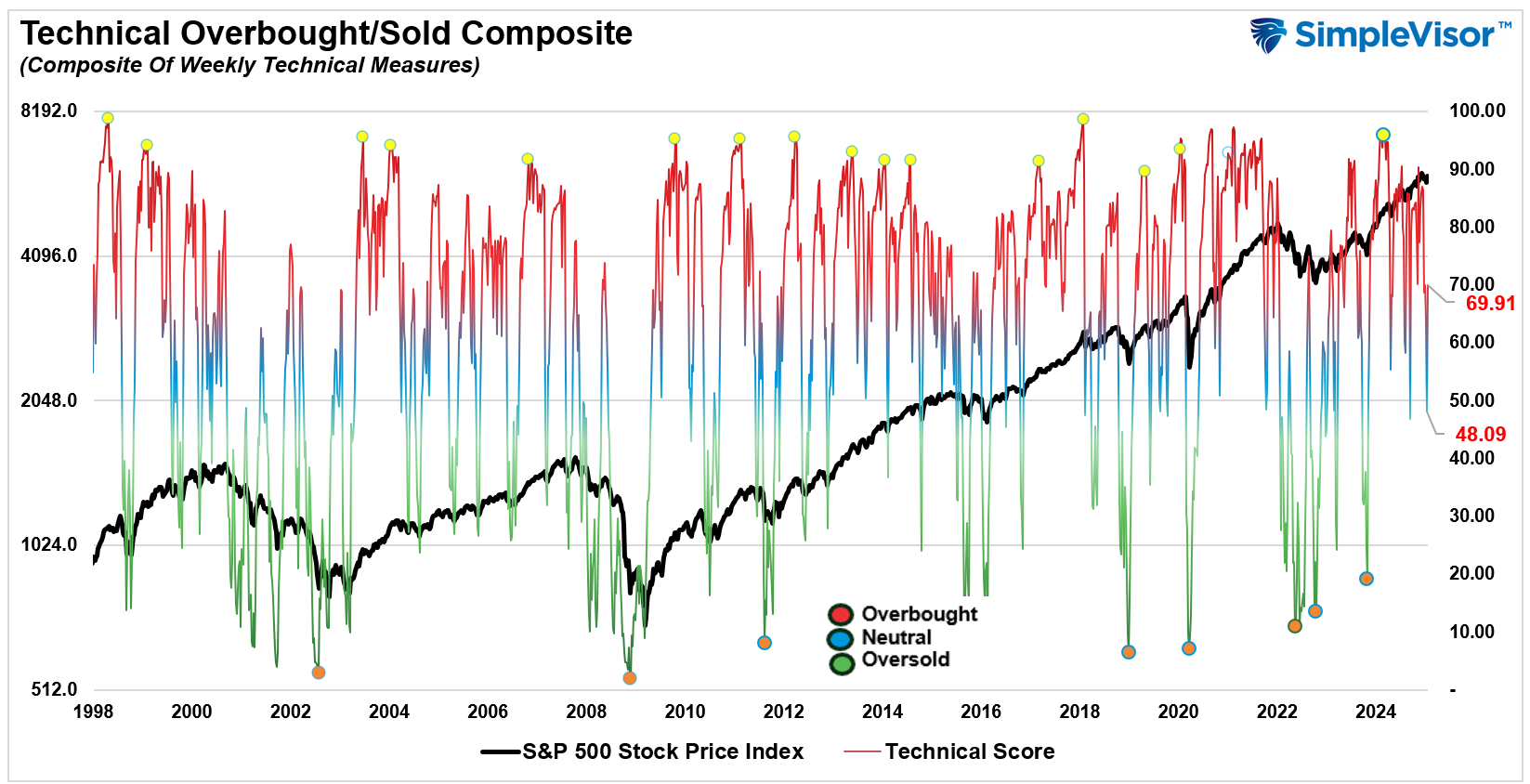

Technical Composite

The technical overbought/sold gauge comprises several price indicators (R.S.I., Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. The market peaks when those readings are 80 or above, suggesting prudent profit-taking and risk management. The best buying opportunities exist when those readings are 20 or below.

The current reading is 69.91 out of a possible 100.

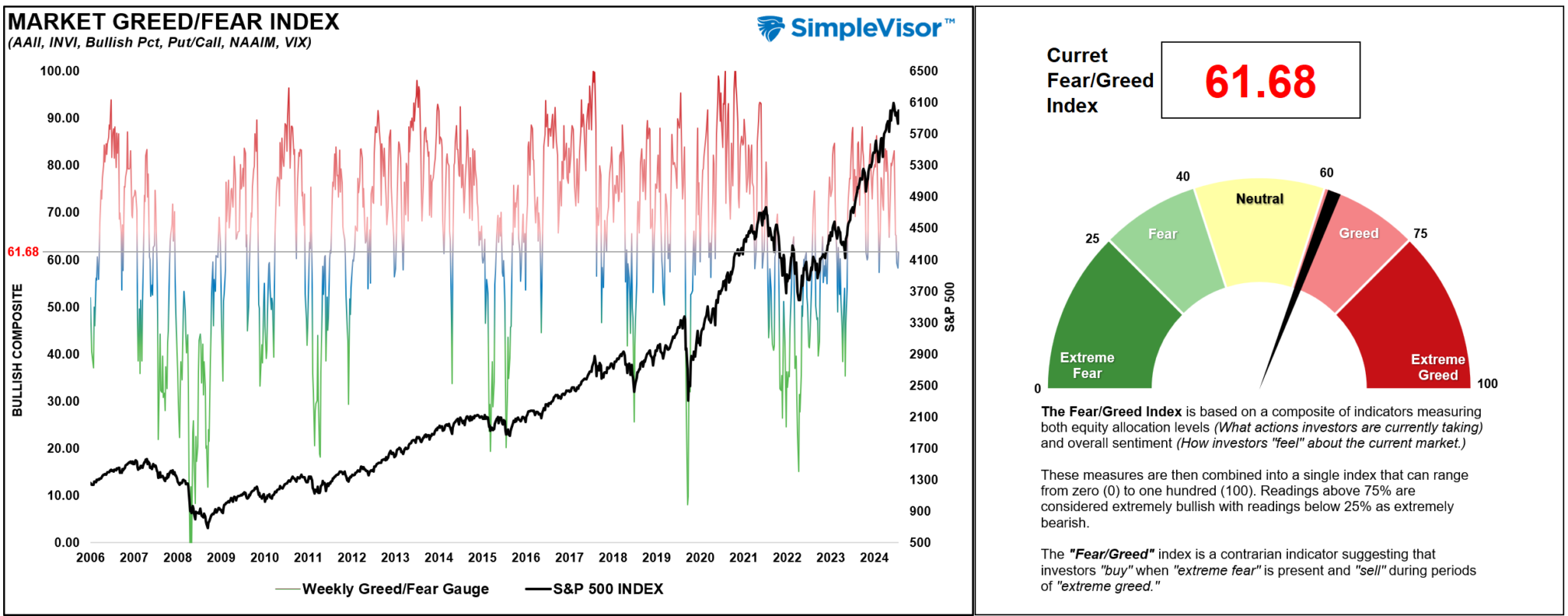

Portfolio Positioning “Fear / Greed” Gauge

The “Fear/Greed” gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, the more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0 to 100. It is a rarity that it reaches levels above 90. The current reading is 62.28 out of a possible 100.

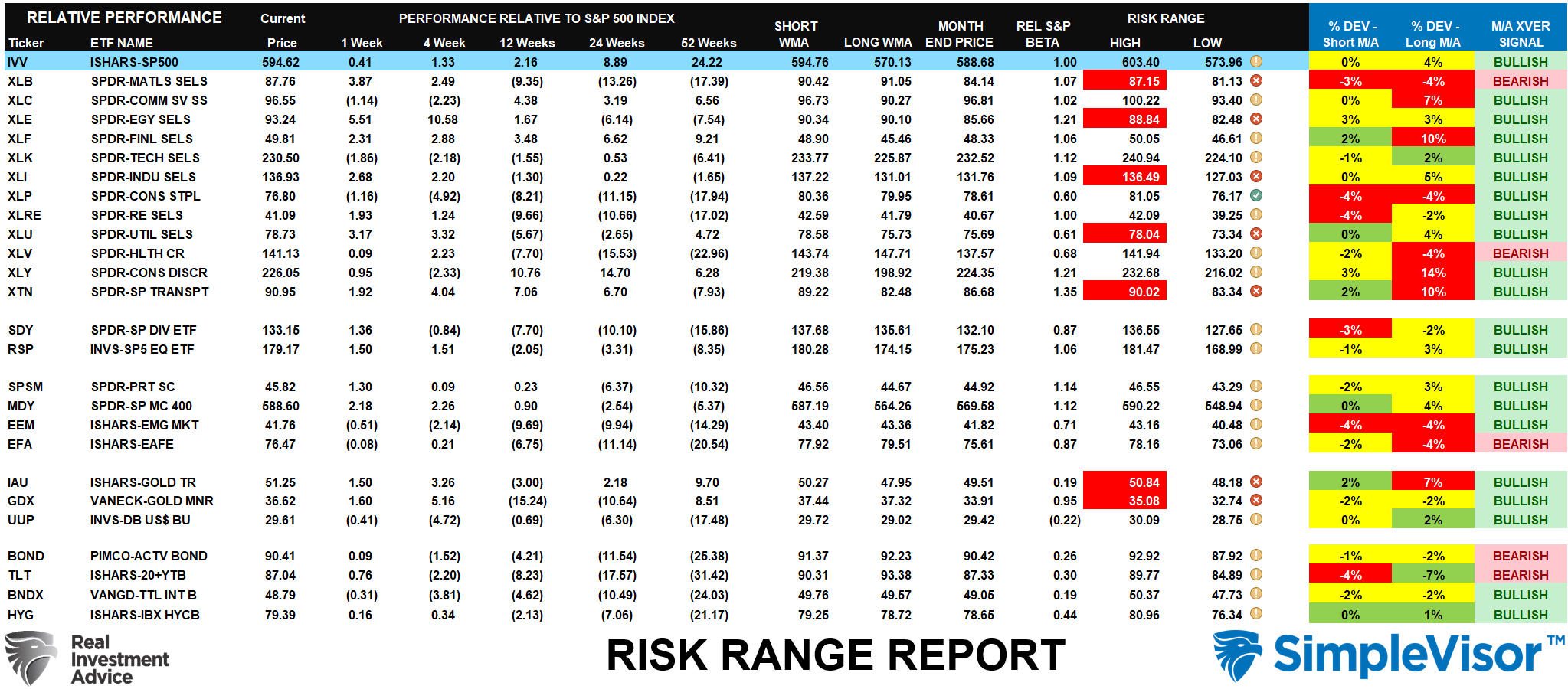

Relative Sector Analysis

Most Oversold Sector Analysis

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares the relative performance of each sector and market to the S&P 500 index.

- “MA XVER” (Moving Average Crossover) is determined by the short-term weekly moving average crossing positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- The table shows the price deviation above and below the weekly moving averages.

Last week we noted that:

“The market selloff this past week moved many sectors and markets into more oversold conditions. Notably, due to the rise in interest rates, real estate is trading well below its risk range, while gold miners are trading well above it. If there is any weakness in economic data over the next week, seeing a rotation between overbought and oversold sectors would be unsurprising. The S&P Dividend Index, Bonds, and Staples are also at levels normally consistent with short-term tradeable bottoms.“

This week, we did indeed see a rather furious rush back into equities, which has now pushed several sectors (noted in red) above their normal risk ranges for the month. Notably, the sharp drop in rates this past week led to a sharp rise in rate-sensitive sectors such as Utilities and Real Estate. This technical bounce is likely just that. Take profits and rebalance risk as needed.

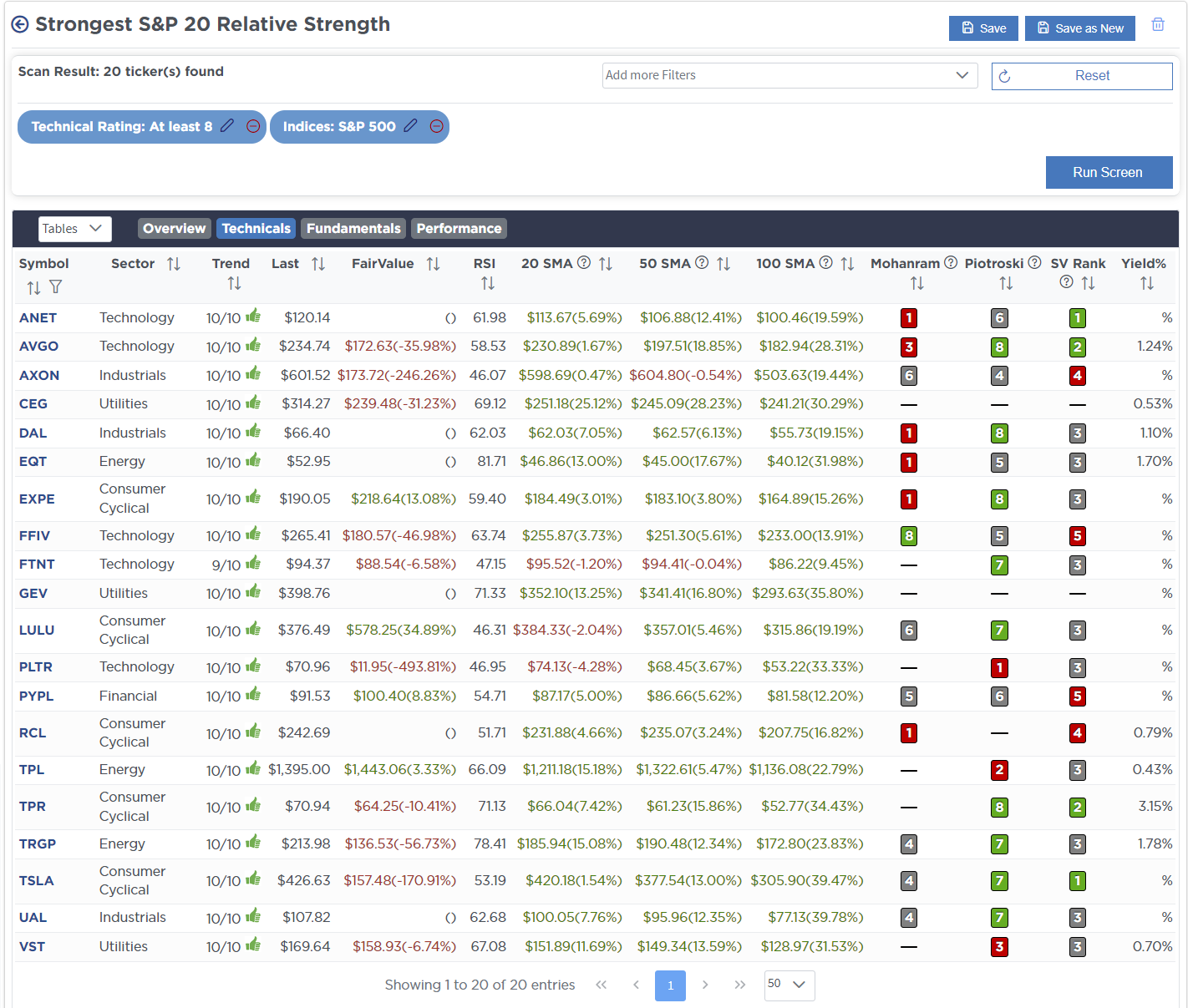

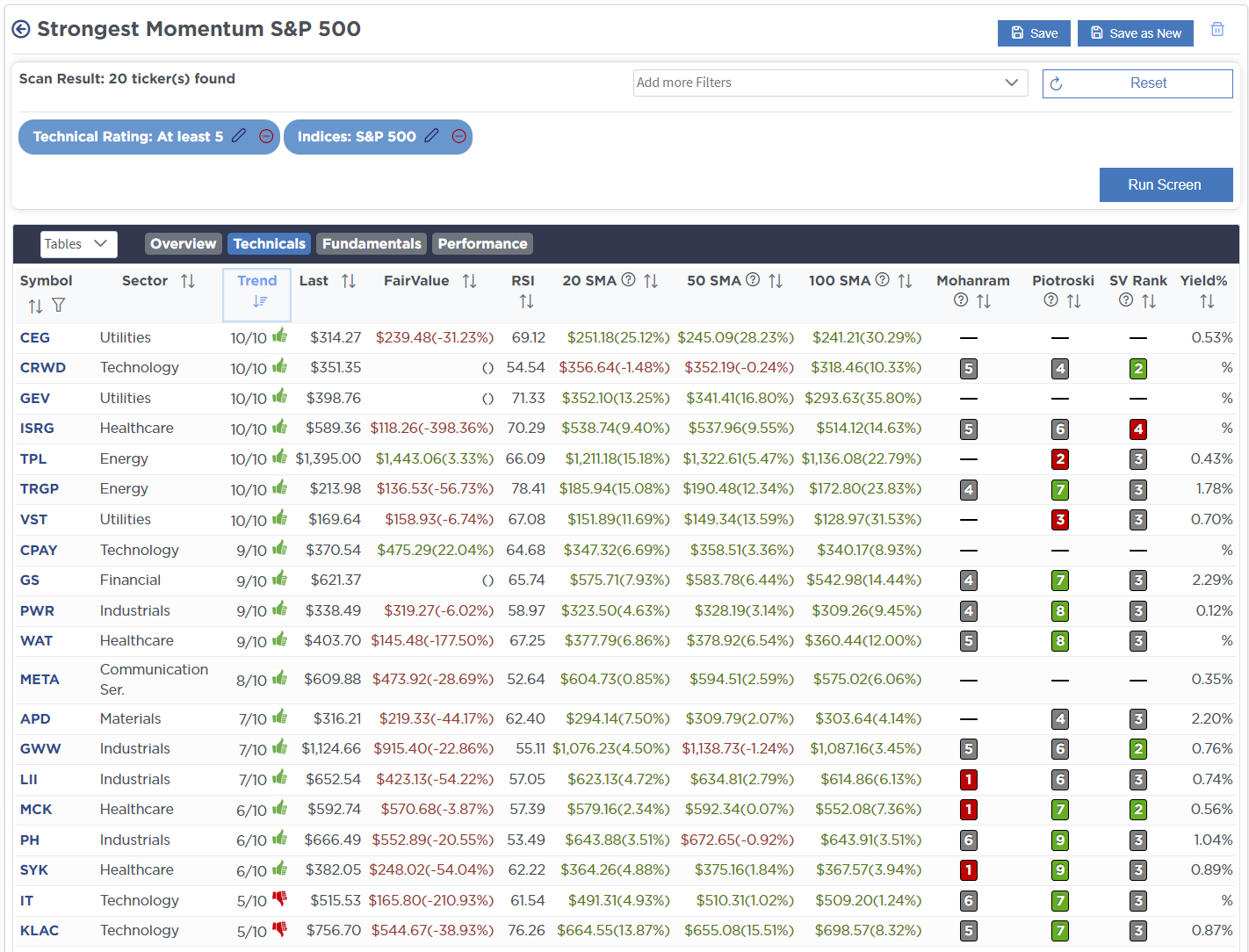

Weekly SimpleVisor Stock Screens

We provide three stock screens each week from SimpleVisor.

This week, we are searching for the Top 20:

- Relative Strength Stocks

- Momentum Stocks

- Fundamental & Technical Strength W/ Dividends

(Click Images To Enlarge)

RSI Screen

Momentum Screen

Technically Strong With Dividends

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

Jan 14th

“On this morning’s RealInvestmentShow we discussed the need to be somewhat more “tactically bearish” as we head into 2025. As such, this morning, we made a few changes to both portfolios to slightly reduce our equity exposure via rebalancing a few positions to model or reducing their model weights.

In aggregate, including all the trades, we reduced our net exposure in both models, We have wanted to buy Palantir (PLTR) for a while but have been patiently waiting on a correction. It is down almost 20% from highs, giving us a chance to add a starter position. We may add to PLTR if the correction isn’t over. Below are the following changes and the new model weights:”

Equity Model

- Add to AMD to rebalance up to model weight 2%

- Initiate a starter position in PLTR of 1% of the portfolio.

- Reduce NVDA and GOOG by 0.5% to 2% and 3.5% of the portfolio, respectively.

- Take profits in FANG and reduce the weight of the position by 0.5% to 1.5%.

- Trim JPM by 0.25% to 1.75% of the portfolio.

ETF Model

- Rebalance XLC to the target model weight of 7%.

- Take profits in XLE and reduce exposure by 0.5% to 3.5% of the portfolio.

- Reduce XLF to 4% of the portfolio.

The net equity reduction in the SimpleVisor accounts is 1.3% in the equity model and 1.9% ETF model.

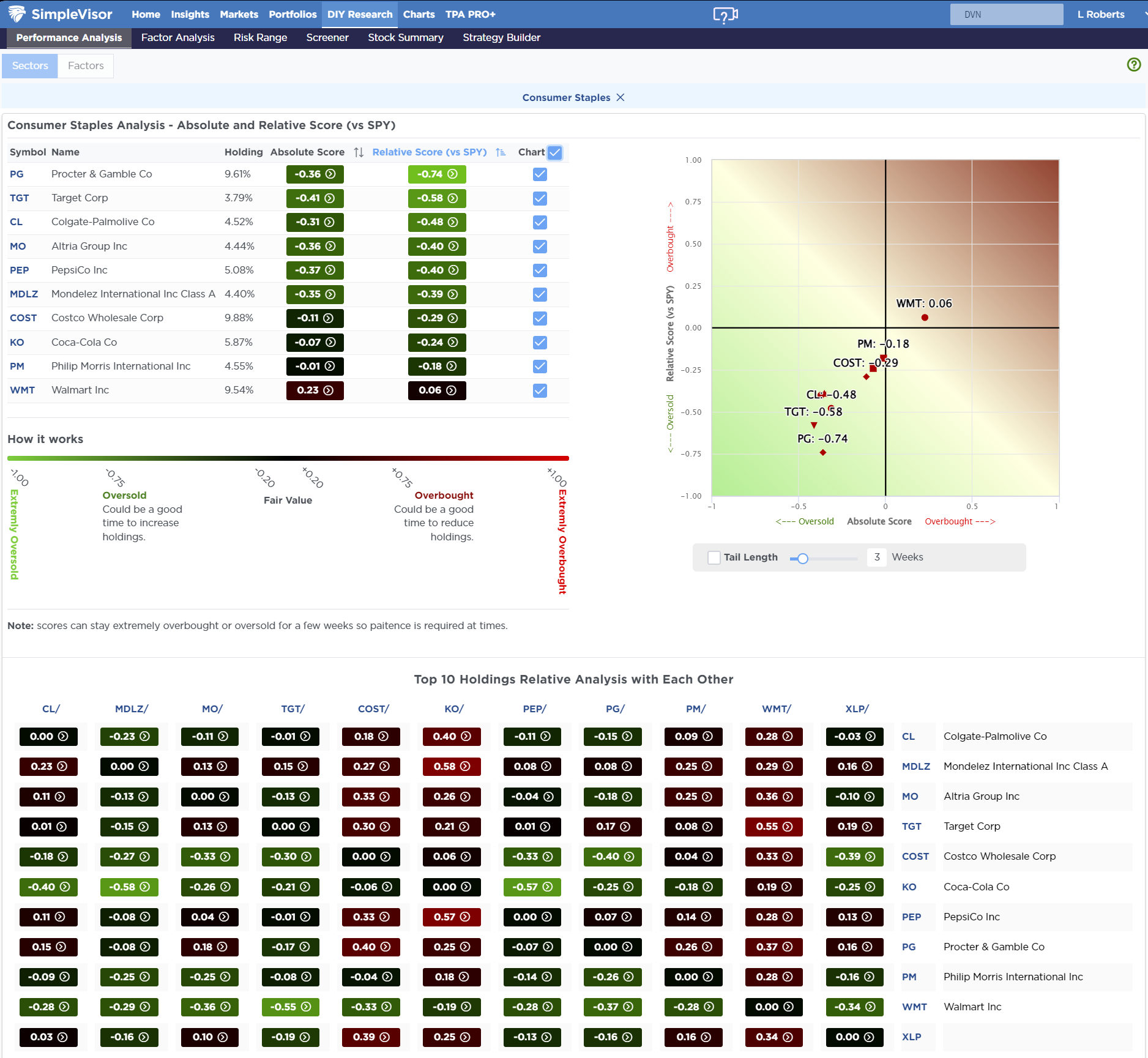

Jan 17th

“In our latest analysis of relative performance, staples have become extremely oversold relative to the rest of the market, while energy, which we trimmed earlier this week, is now more overbought. This is shown in the relative analysis section of SimpleVisor and above.

Of the Staples sector, Proctor and Gamble (PG) is the most oversold on a relative basis. Therefore, this morning, we added .5% to PG and 1% to XLP. With staples turning to strong buy signals, we could see a rotation to this sector, which has some of the strongest fundamentals. Notably, this addition is also a defensive move and will likely accompany further portfolio shifts in the coming weeks and months.”

Equity Model

- Increase PG to 3.5% of the portfolio.

ETF Model

- Increase the iShares Staples ETF (XLP) to 7% of the portfolio

Lance Roberts, C.I.O., RIA Advisors

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)