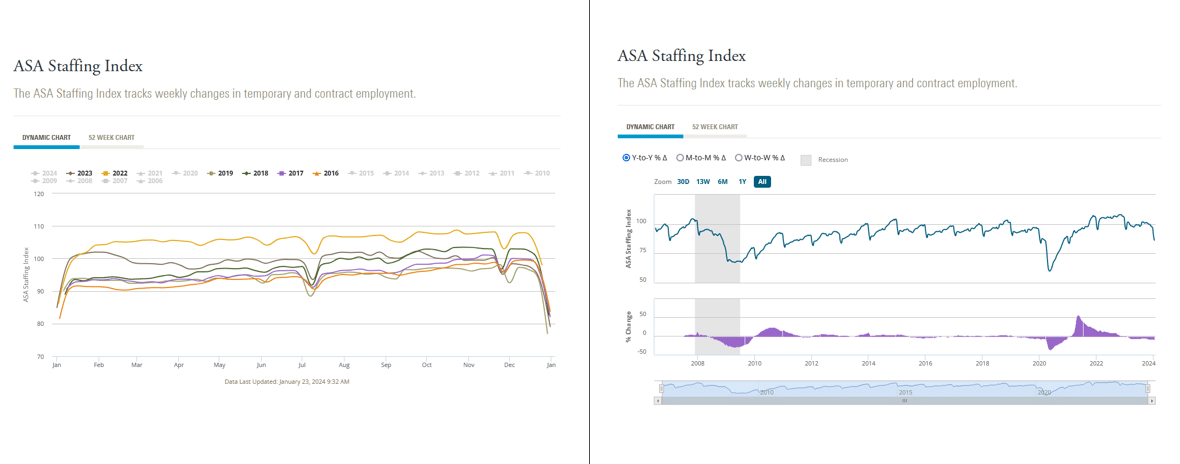

We believe that the clearest sign of a coming recession is weakness in the labor markets. Thus far, we haven’t seen anything overly concerning in employment data. Hence, to help us assess the labor markets, we follow many government and private employment gauges. The ASA Staffing Index was recently brought to our attention. A reader asked if we thought that the ASA Staffing Index might be a warning of trouble ahead. The American Staffing Association (ASA) Staffing Index tracks weekly changes in temporary and contract employment via surveys of hiring managers.

The ASA Staffing Index graph on the right accompanied our reader’s question. As shown, the current index has fallen sharply and sits below many of the pre-pandemic prior troughs. First, note that the index is not seasonally adjusted. Therefore, Christmas holiday-related employment decisions create anomalies in November and December, when many people are hired, and in January, when they are no longer needed. The graph on the left helps us appreciate the seasonality and answer the question. As shown, in 2022 (yellow), the index was well above 2023 levels and pre-pandemic norms. Conversely, 2023 is in-line to slightly below the pre-pandemic years. We characterize the recent data as normalizing to prior trends and not necessarily weak. However, further deterioration of the ASA Staffing Index may change our minds.

What To Watch Today

Earnings

Economy

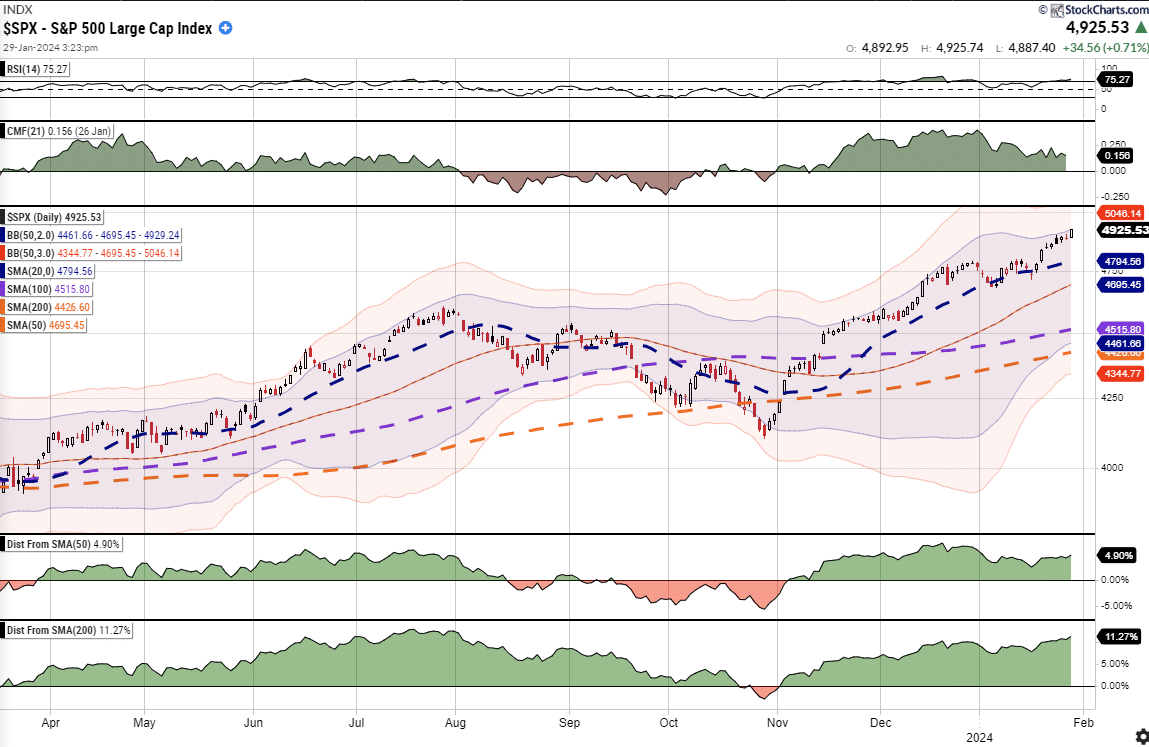

Market Trading Update

Yesterday, markets started out the day a bit sluggishly, until the afternoon when stocks exploded higher following comments from Elizabeth Warren and three other Democrats to Jerome Powell. Warren urged Fed Chair Jerome Powell to bring down interest rates at the upcoming meeting to, wait for it, “expand affordable housing.”

The irony, just in case it was missed on you, is that lower rates make housing prices go up, and housing is less affordable even at lower interest rates. Notably, this has been the issue with housing going back to the turn of the century when Alan Greenspan pushed adjustable-rate mortgages so more people could be housing. Lower rates and easier lending standards followed, pushing more people who couldn’t afford it into housing, driving prices higher, requiring more accommodations and lower rates. (I am going to write an article on this soon.)

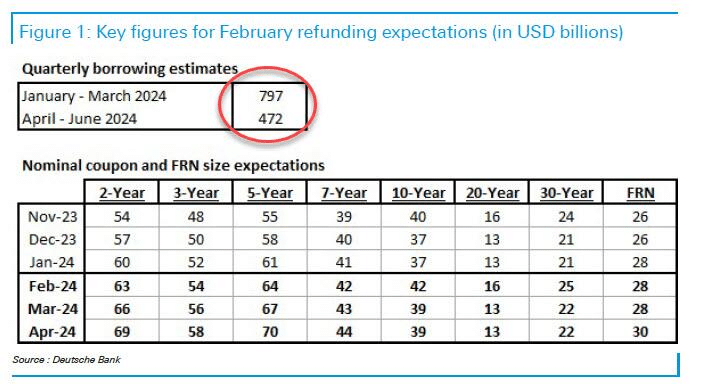

Also, adding to the surge was an announcement from the Treasury that slashed their borrowing estimates. That announcement sent bond yields tumbling and added to the stock market rally.

Nonetheless, from the market perspective, any hopes of more aggressive rate cuts, sooner rather than later, are bullish. As such, the comments sent stocks, or rather the “Mega-7” soaring higher. Such led to a fresh all-time high while creating a bigger deviation from the 50-DMA. The deviation must be corrected soon, which I suspect we will see in early February. Continue to hold equity exposures, but taking some gains from big winners isn’t the worst idea.

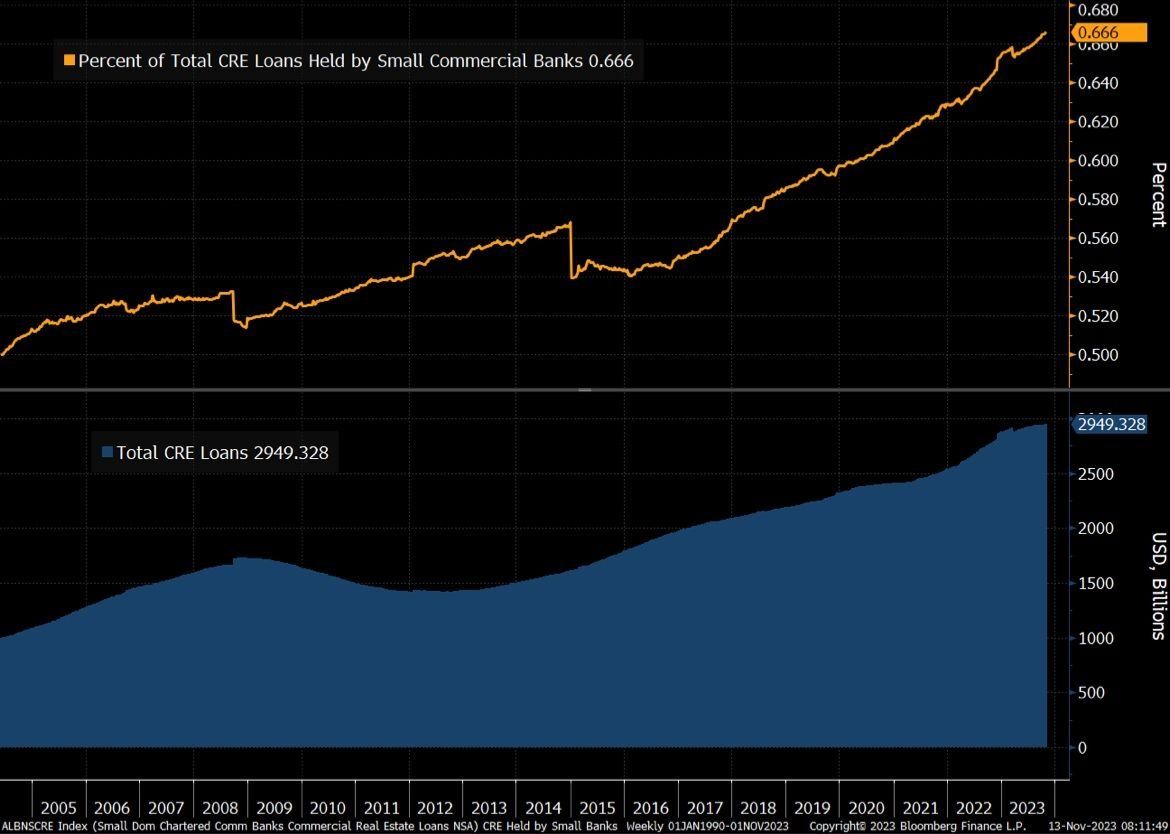

Smaller Banks Are On The Hook For CRE Losses

Commercial Real Estate (CRE) prices are plummeting throughout much of the nation. The work-from-home movement is resulting in a sharp increase in office vacancies. Further, workers aren’t returning to their offices in meaningful numbers despite the pandemic ending. Additionally, higher interest rates and pre-pandemic overbuilding (due to low interest rates) are dragging on CRE prices materially.

Quite often, buyers of CRE use leverage. For instance, they may purchase a $30 million building with $5 million in cash and $25 million in debt. Accordingly, if the owner needs to sell and the price of the building has fallen by more than $5 million, then the lender is often on the hook for any additional loss. As shown below, two-thirds of those lenders are smaller banks. Further troubling is that CRE loans are often for 5-7-year terms. As those loans come up for refinancing, the higher interest rates and or low vacancy rates may force some owners to default, thus leaving the bank with the property and, in many cases, a weak market to sell the property into to minimize a loss.

The following information comes from the Kobeissi Letter:

14% of all commercial real estate (CRE) loans and 44% of office building loans are now in “negative equity.” In other words, the debt is now greater than the property value on all of these properties. Currently, US banks hold over $2.9 trillion of CRE debt, the majority of which is held by regional banks. Office building prices are down 40% from their highs and CRE as a whole is down over 20%. All as rates rise and many of these loans are due to be refinanced. CRE is beyond bear market territory.

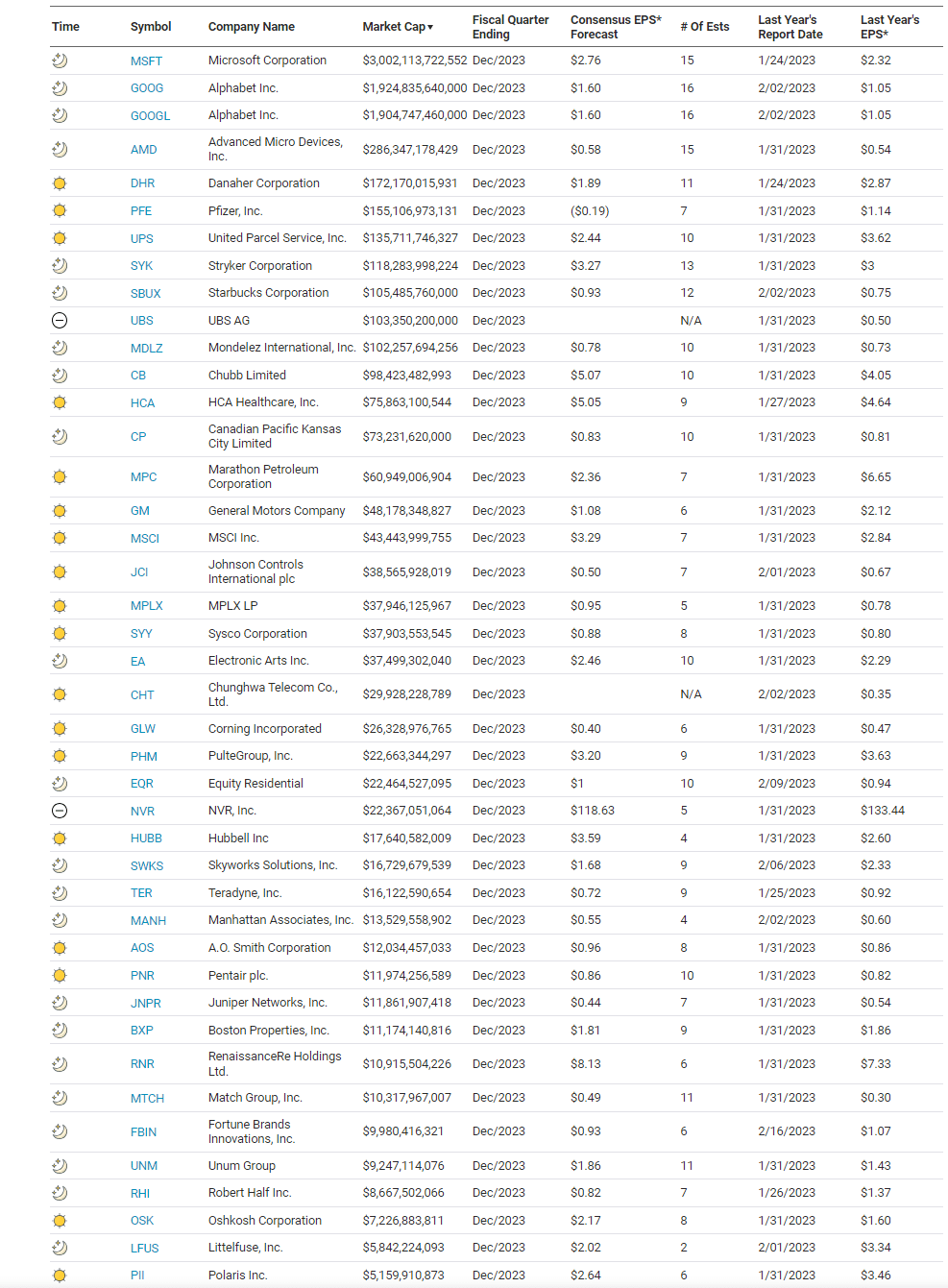

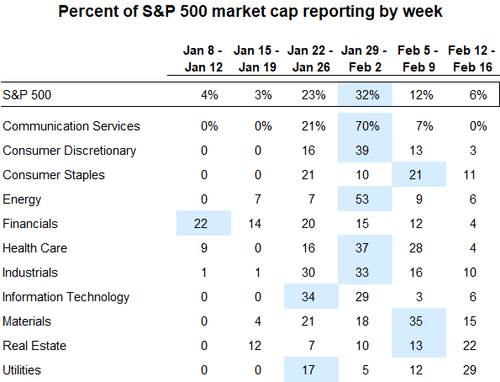

Big Week For Earnings

This will be the most important week of the Q4 2023 earnings season! Per the Goldman Sachs table below, a third of the S&P 500 market cap reports this week. The communications sector will get earnings announcements from 70% of its constituents by market cap. Five of the Magnificent Seven stocks, which have been leading the market, will report. Between employment data and the Fed meeting on Wednesday, the sectors highlighted in blue will likely get an additional jolt of volatility as earnings are released.

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Post Views: 3

2024/01/30