The Debt Limit has been reached, and the Treasury is resorting to “extraordinary measures” to keep the government running. While the situation may sound dire, it is the status quo. Since 1960, Congress has acted 78 different times to permanently raise, temporarily extend, or revise the definition of the debt limit. If you fret that this time is different because of the split Congress, have no fear. Both political parties have proven willing to raise the debt cap limit. Of the 78 increases since 1960, 49 occurred under Republican presidents and 29 under Democratic presidents.

From today until they increase the debt limit, the Treasury can still issue debt, but it can’t increase the amount of debt outstanding. Effectively, the Treasury will issue debt commensurate with the maturing debt. Further, the Treasury has nearly $400 billion in its savings account at the Fed. The Treasury forecasts those funds can keep the government running into May. Also, the Treasury will make mandatory payments like social security, welfare, and interest expense on the debt, but it can slow or stop payments for non-mandatory items. Treasury Secretary Janet Yellen is and will continue to warn of default until the cap increases. Negotiating tactics, including default threats, may induce some bond and stock market volatility. But, as we have learned on 78 occasions in the last 62 years, the debt cap limit will be raised.

What To Watch Today

Economics

- 10:00 a.m. ET: Existing Home Sales, December (3.95 million expected, 4.09 million prior)

- 10:00 a.m. ET: Existing Home Sales, month-over-month, December (-3.4% expected, -7.7% prior)

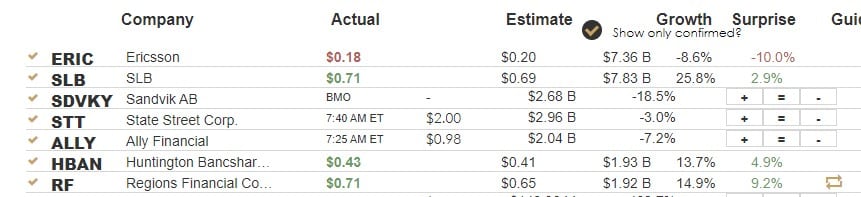

Earnings

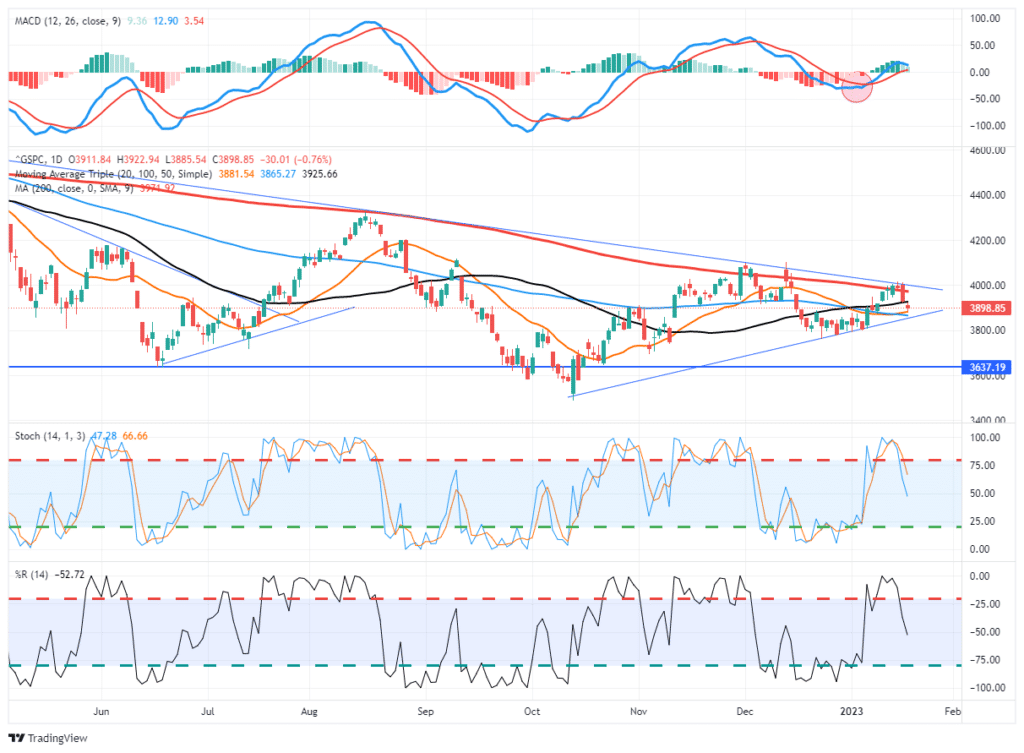

Market Trading Update

The market pullback has been fairly orderly within the current consolidation process. That narrowing wedge is compressing prices for a breakout in one direction or the other. Given that compression, whichever direction the market takes will likely be an outsized move over the short term.

The MACD buy signal remains intact for now, and the recent overbought conditions are getting reversed. If the market can hold above the 20-DMA and 100-DMA moving averages, which the market tested yesterday, then a move back to the 200-DMA is possible. The 50-DMA will act as initial resistance to any move higher. Given the compression in the market, the next few days could be bumpy as the market awaits the next Fed meeting.

The outcome of that FOMC meeting, either hawkish or dovish, will likely resolve the current consolidation process into a directional move for investors to trade. Remain cautious for now until that market tells us where it wants to go next.

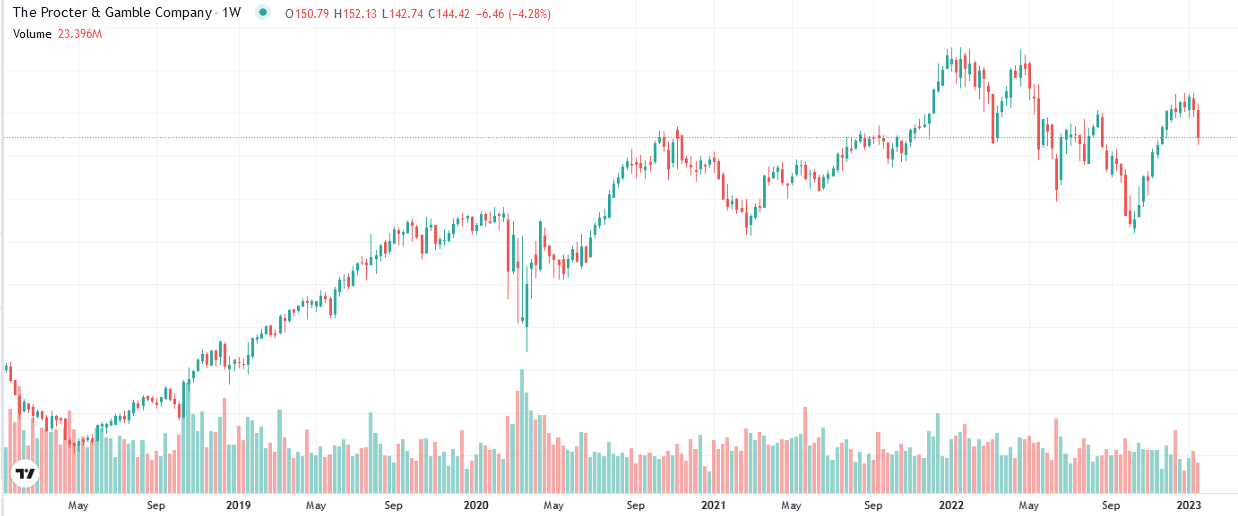

P&G- Inflation is Eating into Profits

Earnings and revenues fell for Proctor Gamble (PG) versus last year, although they beat Wall Street expectations. The stock initially fell on the report as the company expects further margin declines this year. They claim it is becoming increasingly harder to pass on higher inflation to their customers. Per CNBC: “P&G is doubling down on its price hiking strategy even as shrinking consumer demand continues to erode sales volume.” Sales, measured in volume, fell 6% last quarter, making it their largest quarterly drop in years. The obvious question facing many retail facing companies is whether they can continue to pass on higher costs to offset inflation and promote growth if the economy slows, unemployment increases, and personal consumption weakens.

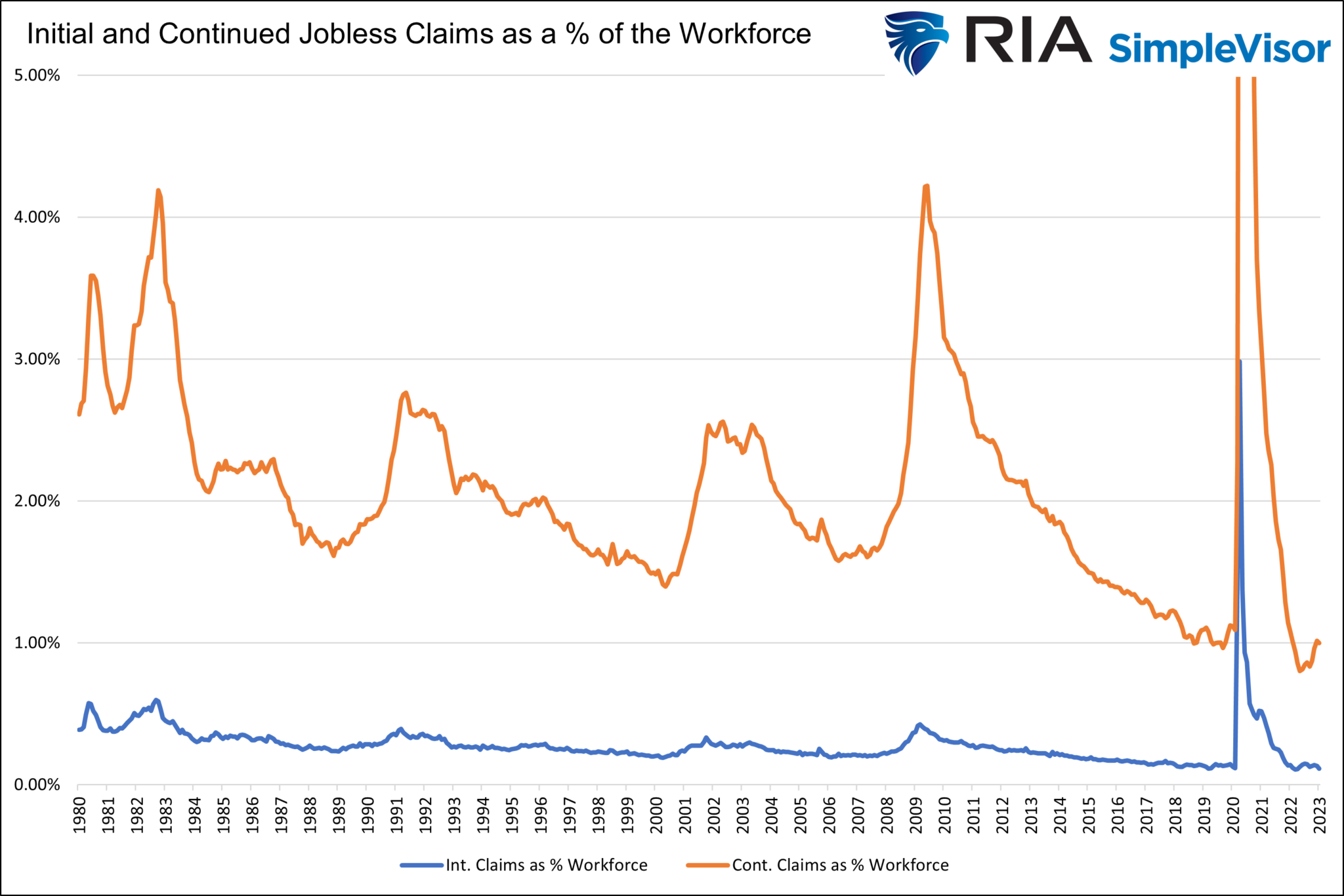

Labor Market Remains Historically Hot

Initial jobless claims fell to 190k, well below the estimated 215k and last week’s 205k. Despite the recent layoffs from major tech companies, few other sectors appear to be cutting staff. Continuing claims, the most real-time indicator of the employment market, ticked up to 1.65 million, but it is still at a very low level.

The graph below shows that initial and continued claims, as a percentage of the workforce, are at 40-year lows. Continued claims as a percentage of the workforce are rising slightly but below the lowest levels attained during periods with the most substantial economic growth.

EPS Estimates Falling Rapidly

The graph below shows that S&P 500 EPS estimates are falling rapidly but still above 2022 levels, portending earnings growth. However, Bloomberg notes that the rate of decline in forecasts is troublesome. Per Bloomberg:

“Profit expectations now stand as arguably the single biggest contrary indicator to the burgeoning optimism. Estimates are moving down at a rate that in recent history has always presaged a recession.”

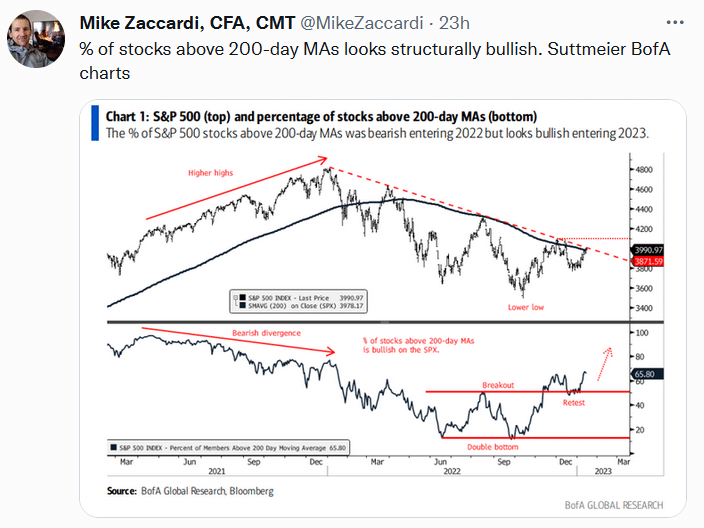

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.