As expected, the FOMC increased the Fed Funds rate by 25bps to 4.50%. They also anticipate that “ongoing increases in the target range will be appropriate.” Doing so would likely leave the Fed Funds rate at 5.00% or higher when they stop hiking rates. If all goes according to the Fed’s plan, markets could get interesting in May. The Fed is transparent that it is willing to stall hiking the Fed Funds rate, but they show no interest in reducing rates. Conversely, the markets imply 50bps in cuts in the second half of 2023. Such a divergence of views often leads to market volatility as either the Fed shifts toward market views or vice versa. As Bloomberg depicts on their current magazine cover, the bulls and Powell are going head to head.

Also of note, the Fed is not making any changes to QT. QT drives liquidity for financial markets in conjunction with its reverse repurchase (RRP) repo program. In the last quarter, the Fed’s RRP program offset a significant amount of the decline in liquidity due to QT. Will the Fed continue to use RRP to manage financial system liquidity? If so, the Fed may be able to manage stock prices to meet their goals.

What To Watch Today

Economy

- 7:30 a.m. ET: Challenger Job Cuts, year-over-year, January (129.1% prior)

- 8:30 a.m. ET: Unit Labor Costs, Q4 Preliminary (1.5% expected, 2.4% prior)

- 8:30 a.m. ET: Nonfarm Productivity, Q4 Preliminary (2.4% expected, 0.8% prior)

- 8:30 a.m. ET: Initial Jobless Claims, week ended Jan. 28 (195,000 expected, 186,000 prior)

- 8:30 a.m. ET: Continuing Claims, week ended Jan. 21 (1.684 expected, 1.675 million prior)

- 10:00 a.m. ET: Factory Orders, December (2.3% expected, -1.8% prior)

- 10:00 a.m. ET: Factory Orders Excluding Transportation, December (0.2% prior)

- 10:00 a.m. ET: Durable Goods Orders, December Final (5.6% prior)

- 10:00 a.m. ET: Durables Excluding Transportation, December Final (-0.1% expected, -0.1% prior)

- 10:00 a.m. ET: Non-defense Capital Goods Orders Excl. Aircraft, December Final (-0.2% prior)

- 10:00 a.m. ET: Non-defense Capital Goods Shipments Excl. Aircraft, December Final (-0.4% prior)

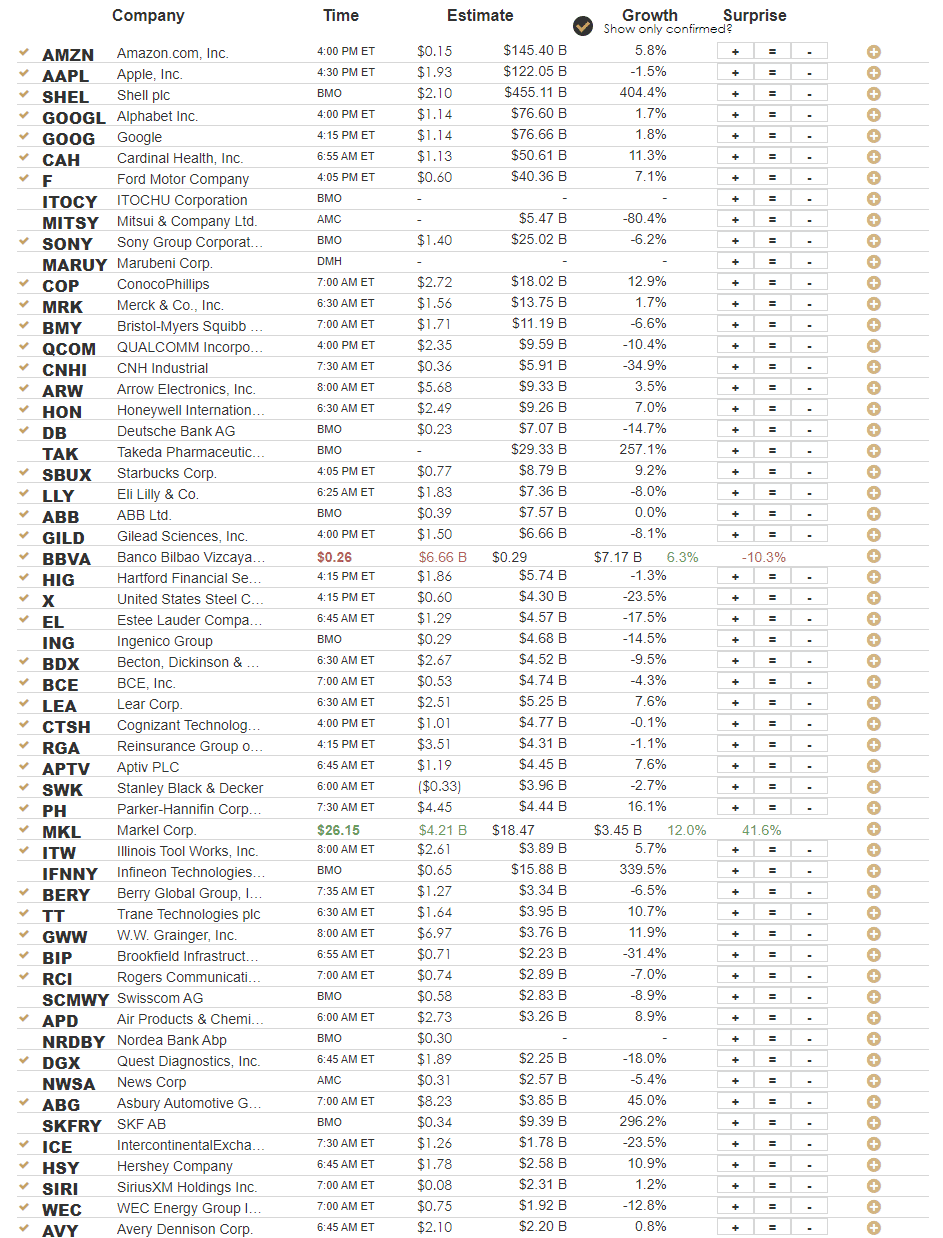

Earnings

The Bull Market Is Back!

Despite what you may have heard, the bull market is back. Good news is good news, bad news is good news, and the Fed no longer matters. As such, it is just time to pony up and buy the dips and, more importantly, buy the stuff with the worst possible fundamentals because that is where the money is to be made.

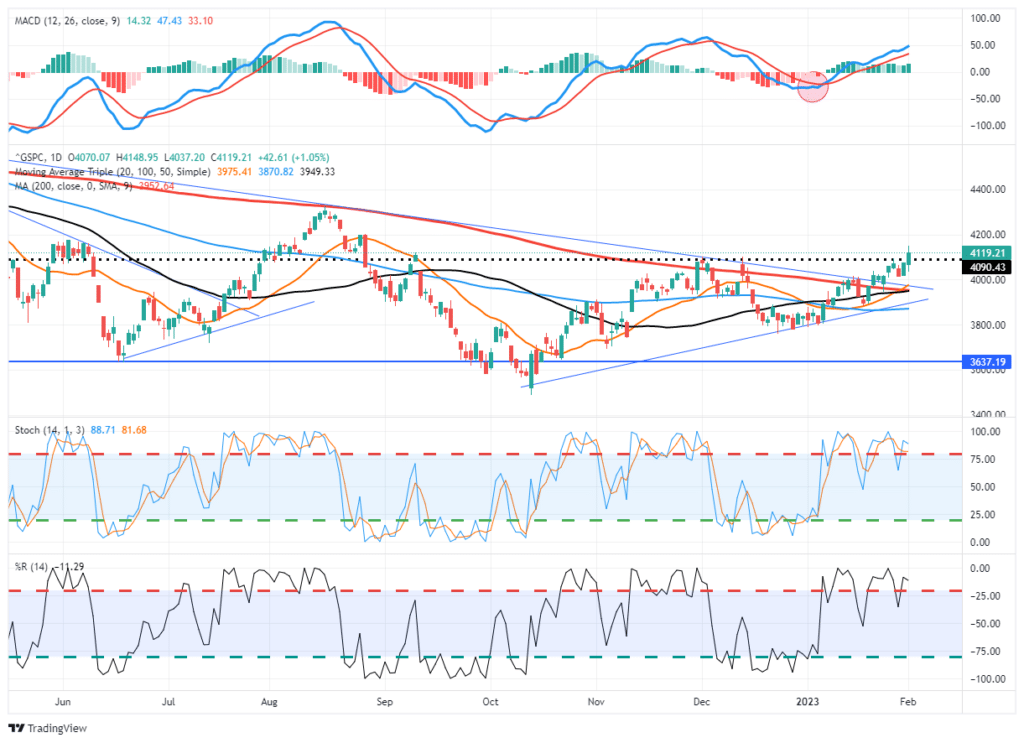

While you may detect sarcasm, the message isn’t wrong. The breakout above the downtrend line, the confirmed inverse head-and-shoulders bottom, and the approaching “golden cross” all suggest that the bulls are in charge for now. Yesterday’s move confirmed the recent breakout by taking out the November highs. Such now puts the 4200-4350 as the next logical target for the market.

The market is getting decently overbought now, with many companies driving the market now trading well into 3-standard deviation territory. While earnings are getting downgraded, companies are beating lowered estimates which are good enough for the bulls. It is important not to fight the market but let the market tell you what it wants to do. For now, we are back to buying the dips until that changes.

What’s Powell Thinking?

The following quotes from yesterday’s press conference help better appreciate Jerome Powell’s views on the economy, inflation, and monetary policy.

- “Despite the slowdown in growth, the labor market remains extremely tight.”

- “Labor demand far outweighs supply.”

- The employment cost index (ECI) is a crucial report the Fed follows to understand how high wages pressure inflation. Tuesday’s ECI report was encouraging, but it is still too high.

- They can’t allow a price-wage spiral to form.

- “Inflation remains well above goal.”

- “Restoring price stability will require maintaining a restrictive stance for some time”

- “Shifting to a slower pace (rate hikes) allows the FOMC time to assess progress.”

- “It is important that financial conditions (stock prices, yields, and the dollar) continue to reflect the policy restraints we have imposed.”

- Core services, representing 56% of inflation, are not yet showing signs that prices are coming down. They “have a lot of work left to do” until core service prices slow. Until core service prices decrease, they will remain vigilant to ensure they “complete the job.“

- “This disinflation process has started.” – “Primarily in goods, but that’s only about a quarter of the PCE index.”

- The Fed sees disinflation in the pipeline for rent and the housing market.

- The committee spent “ample time” debating when they might pause rate hikes.

- Three month measures of inflation are low, but it’s primarily due to unsustainable “transitory” declines in good prices.

- “We are in the early stages of disinflation.”

- “Covid is no longer playing an important role in our economy.”

Our Takeaway

Powell really didn’t break new ground, but he did appear more flexible about the possibility the Fed eases once they are comfortable inflation is slayed. He remains vigilant that the tight labor market keeps upward pressure on inflation. The Fed is very concerned with core service prices. Likely when non-housing services show disinflation, the Fed will get more comfortable. He stressed on numerous occasions that this is a unique environment to forecast inflation and growth. Thus, a highly restrictive policy is warranted to ensure inflation gets to 2%. “This is not a standard business cycle.” “Certaninty is not appropriate.“

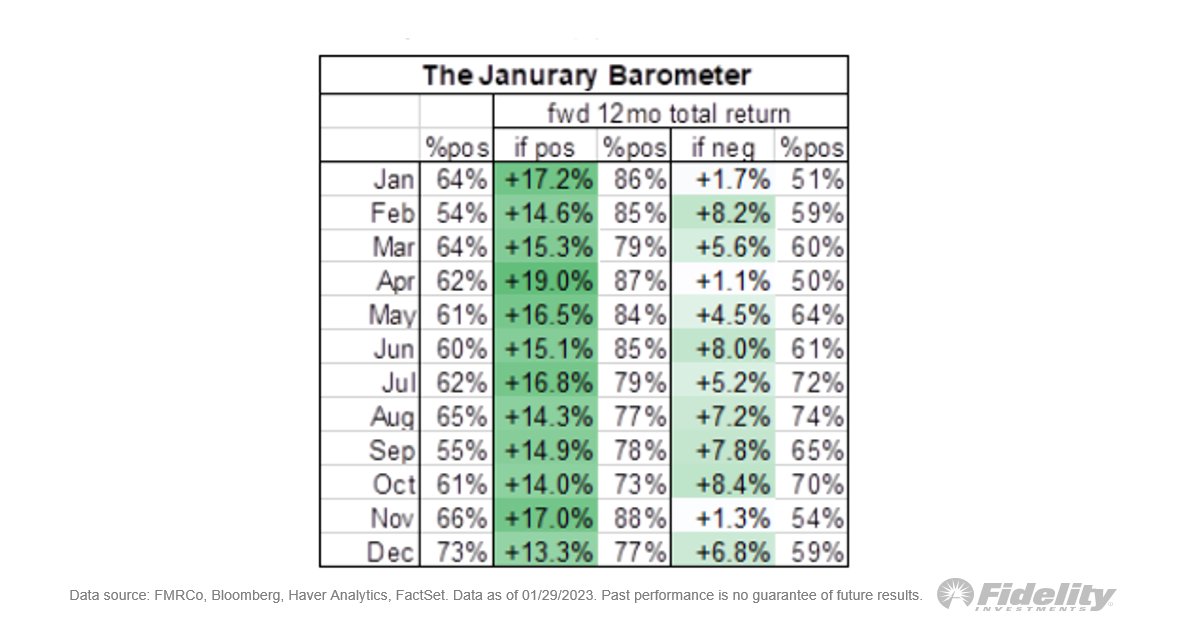

Is the January Effect Real?

The S&P 500 was up 7% in January, prompting some investors to assume 2023 will be a good year. The January effect, a Wall Street myth, assumes that as goes January as goes the year. While the January effect may sound good in theory, the same theory works for every month. The fact is that stock prices most often trend higher. As such, the momentum in January is also part of the same momentum that fueled stocks in the prior months and the coming months. As the table shows, the January effect is, on average, bested by the April and November effect. Even in the worst month historically, October, a gain for the month results in a gain for the next 12 months three-quarters of the time.

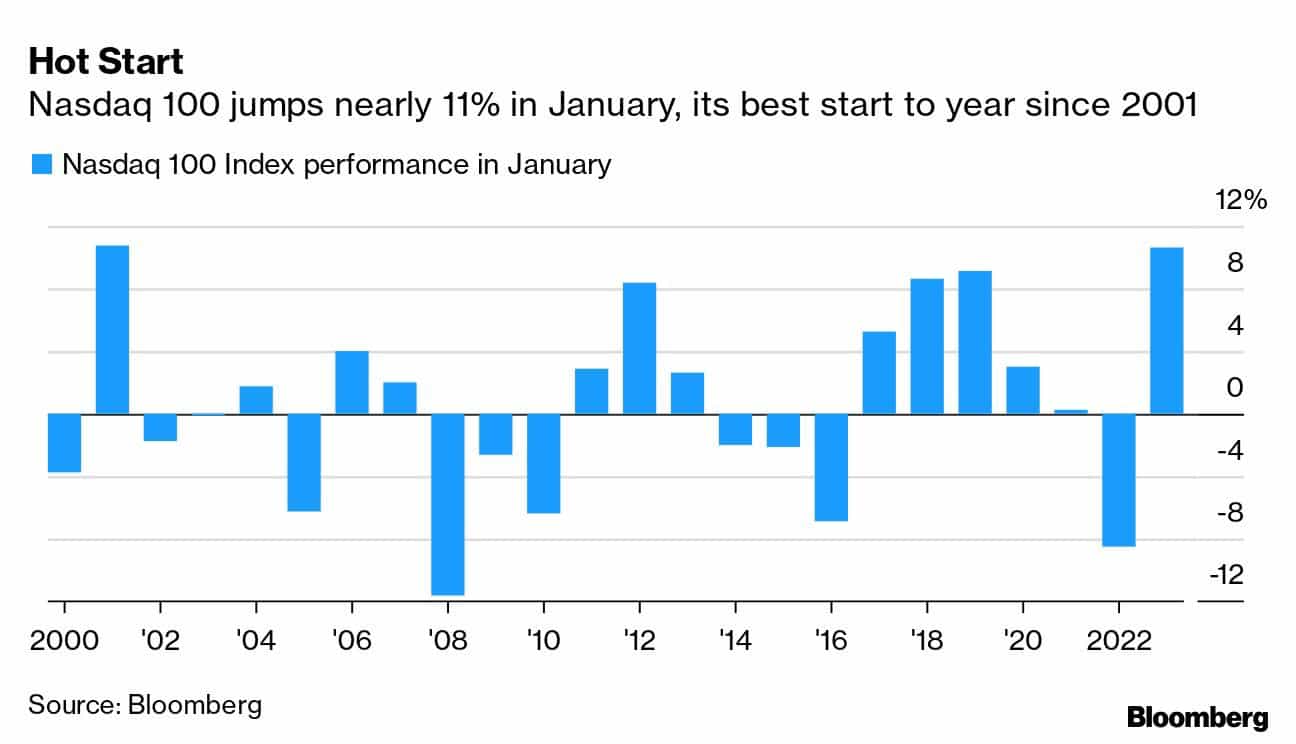

The second graph provides a little food for thought for those looking at January 2023 returns and getting bullish. In 2001, the Nasdaq started the year with an 8% gain in January. By September, it was down 54% year to date. It rallied to close the year down 35%, resulting in a lot of pain for those following the January effect.

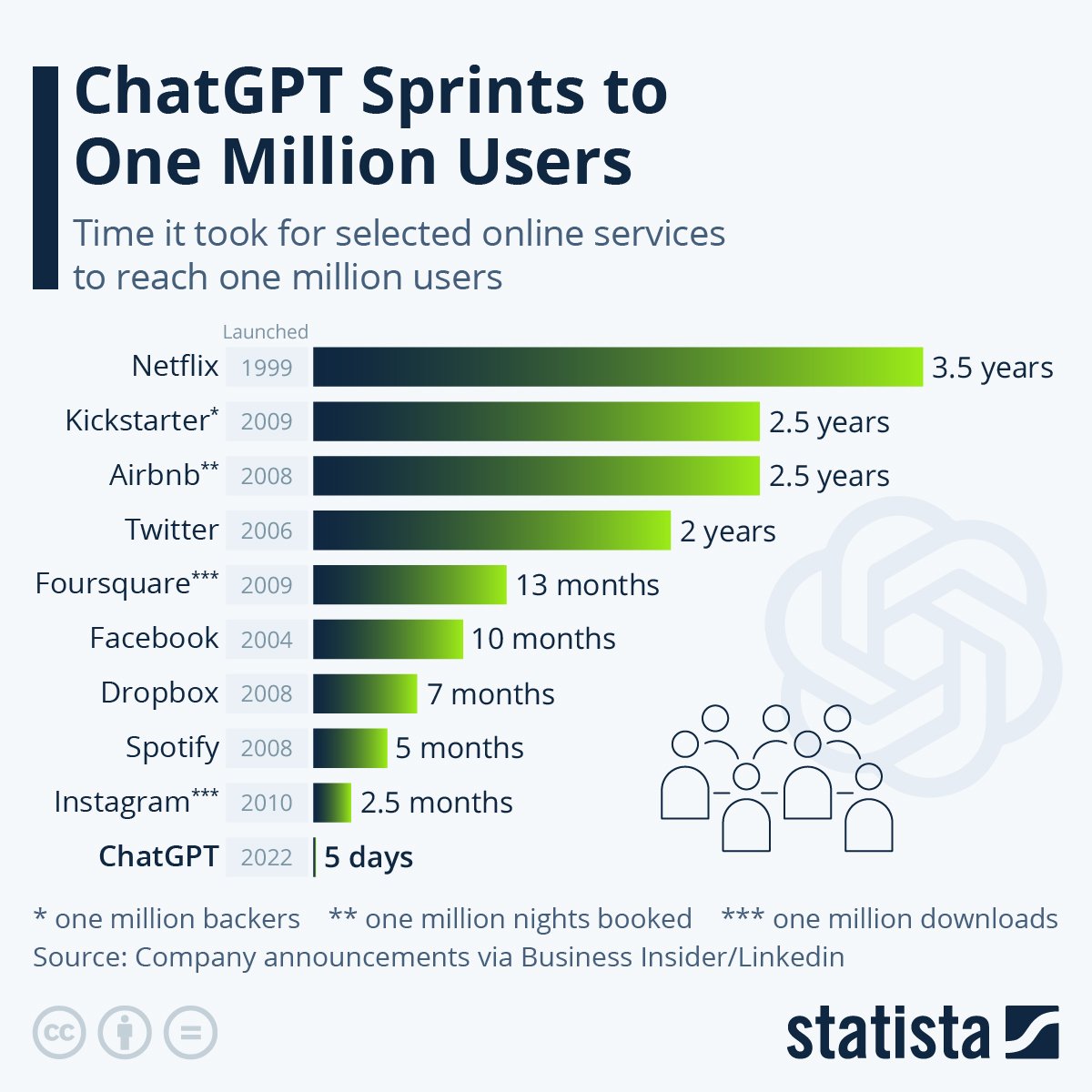

ChatGPT is Off to a Great Start

In our Commnetary from January 27, we discussed how Microsoft’s recent purchase of part of ChatGPT would benefit the company. The graph below shows that the uptake of ChatGPT AI technology is off to an amazing start. Facebook took ten months to reach one million users, and Twitter took two years. ChatGPT reached one million users in less than a week! As we wrote a week ago:

The potential Chat GPT applications are immense, and the benefits will likely flow to Microsoft shareholders.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.