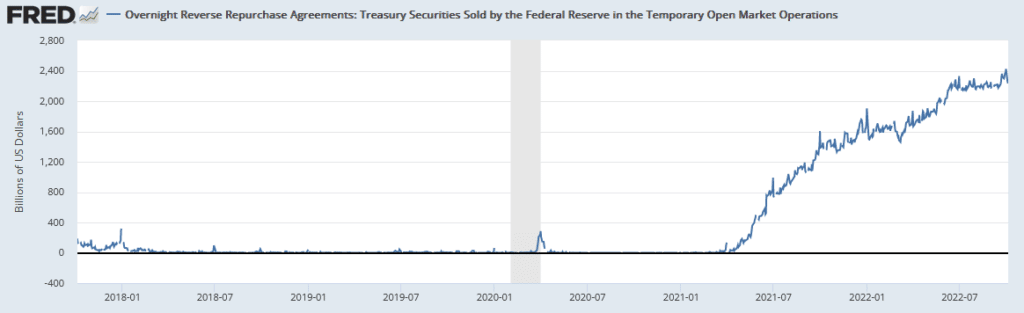

The Federal Reserve has a big hand when it comes to market liquidity. While the Fed’s balance sheet, via QE and QT, garners a lot of attention from investors, its overnight reverse repo program is not closely followed. The Fed’s repo program has been around for almost 20 years, but until late 2021, it was rarely used. The program allows banks and large institutional investors to park cash overnight at the Fed. The Fed uses the repo program to help manage the Fed Funds rate toward its target rate.

As we share below, the Fed’s repo program has become an enticing place to invest cash overnight. The problem, however, is that the cash, aka liquidity, is essentially removed from the banking system. Therefore, the liquidity is unavailable as collateral to buy other assets. As the program grows, liquidity declines. The Fed’s repo book peaked at $2.425 trillion on September 30. As of Tuesday, it stands at $2.233 trillion. We would like to see the program decline. In doing so, it will push liquidity back into the markets.

What To Watch Today

Economy

- 8:30 a.m. ET: Two-Month Payroll Net Revision, September (-107,000 prior)

- 8:30 a.m. ET: Change in Nonfarm Payrolls, September (260,000 expected, 315,000 prior)

- 8:30 a.m. ET: Change in Private Payrolls, September (275,000 expected, 308,000 prior)

- 8:30 a.m. ET: Change in Manufacturing Payrolls, September (20,000 expected, 22,000 prior)

- 8:30 a.m. ET: Unemployment Rate, September (3.7% expected, 3.7% prior)

- 8:30 a.m. ET: Average Hourly Earnings, month-over-month, September (0.3% expected, 0.3% prior)

- 8:30 a.m. ET: Average Hourly Earnings, year-over-year, September (5.0% expected, 5.2% prior)

- 8:30 a.m. ET: Average Weekly Hours All Employees, September (34.5 expected, 34.5 prior)

- 8:30 a.m. ET: Labor Force Participation Rate, September (62.4% expected, 62.4% prior)

- 8:30 a.m. ET: Underemployment Rate, September (7.0% prior)

- 8:30 a.m. ET: Wholesale Inventories, month-over-month, August final (1.3% expected, 1.3% prior)

- 8:30 a.m. ET: Wholesale Trade Sales, month-over-month, August (0.5% expected, -1.4% prior)

Earnings

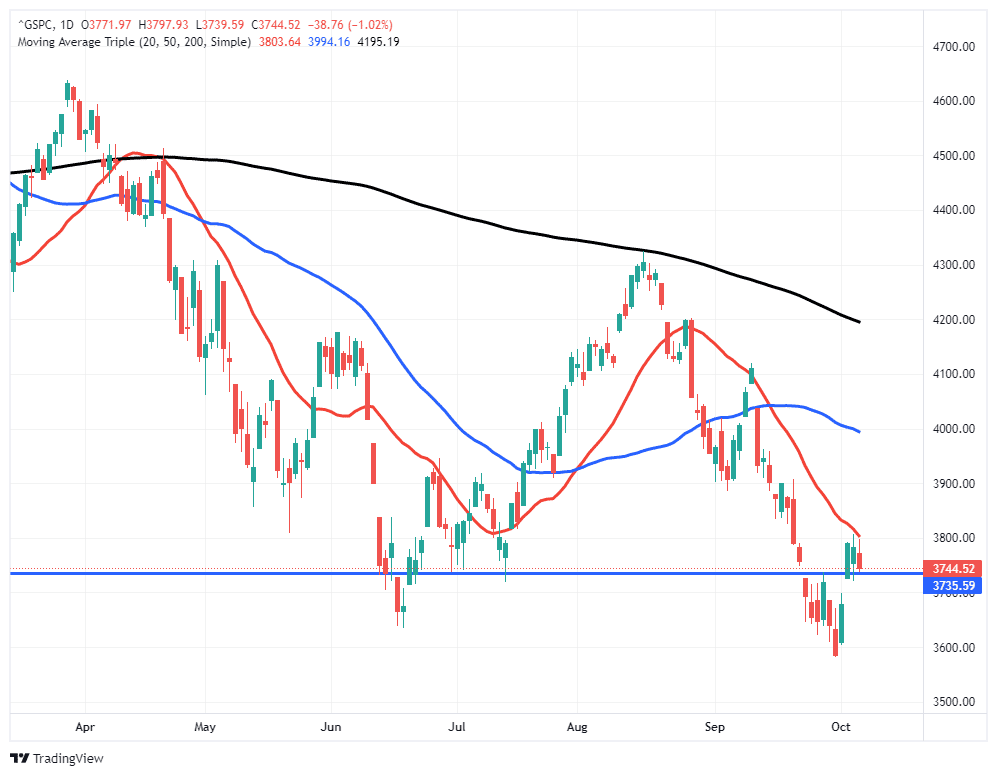

Market Trading Update

During a relatively quiet session heading into this morning’s “employment” report, the market gave back some of its recent gains yesterday. A strong job number will likely lead to a sell-off in equities as investors think the Fed will remain aggressive on rate hikes. (Next week is the September CPI Report as well). A weak jobs number, bad economically, could boost stocks as investors believe the Fed will “pivot.”

The market ran into first resistance at the 20-dma but held support at the June and July lows. A breakdown that fills the Tuesday gap will be a bearish take for the rally, suggesting a retest of lows is likely. Regardless of outcomes, we are looking to use whatever rally we get to reduce exposure and raise cash further.

By the Numbers: Mid-Term Elections + Stock Market

What’s up for grabs: Midterm elections 2022

- All 435 House seats and 35 of the 100 Senate seats (source: Jefferies)

- 36 out of 50 states will elect governors (source: Jefferies)

What stocks tend to do around midterm elections

- Since 1942, the median equity market returns in the first three-quarters of midterm election years were -1%, 2%, and 5%, respectively. 4Q returns jumped to 8%. (Source: U.S. Bank)

- The average annual return of the S&P 500 in the 12 months before a midterm election is 0.3%, below the historical average of 8.1%. (Source: U.S. Bank)

- The S&P 500 has historically outperformed in the 12-month period after a midterm election, with an average return of 16.3%. (Source: U.S. Bank)

- The last time the S&P 500 Index produced negative returns 12 months after a midterm election was 1939 (see Great Depression World War 2). (Source: U.S. Bank)

What Wall Street Is Saying on the Mid-Terms and Stocks

- “Our analysis shows that the economy’s health is a much more important factor than midterm election results.” — U.S. Bank.

- “The higher cost of living and an aggressive rate tightening cycle complicates the voting picture. A lot will depend on voter turnout on the day.” — Jefferies.

- “But irrespective of the result, there’s a consistent market signal in all 19 midterm elections since WWII: The S&P 500 has ALWAYS been higher exactly a year after the vote.” — Deutsche Bank.

“There are myriad unknowns heading into this period, not the least of which is how the midterms will impact the legislating calculus, but we expect movement on the annual defense bill, a federal funding package that could become a Christmas tree carrying numerous ornaments, and possibly a targeted tax bill.” — BTIG

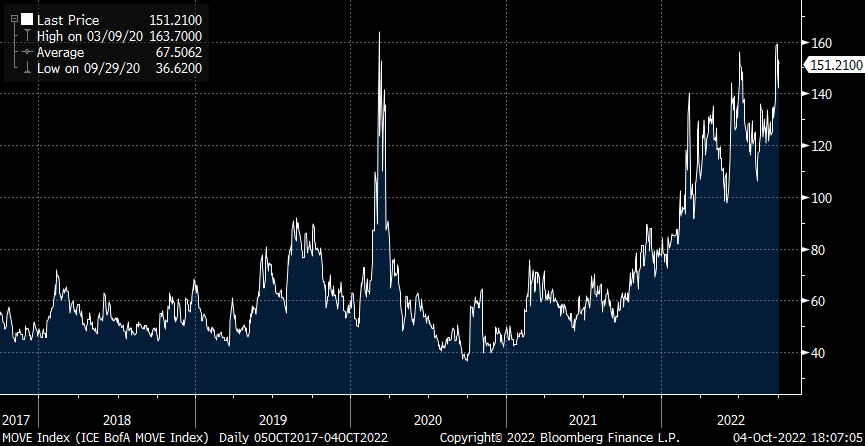

Bond Market Volatility Warns of Illiquidity

The graph below is the MOVE index. It is the bond market’s equivalent of the stock market’s VIX index. Both indexes measure the amount of expected price change. As we show below, the MOVE index is near its highest level when the pandemic started. While many investors look at the graph and see market expectations for significant price moves, we look at it differently. In Liquidity and Volatility, we discussed how volatility is not just a measure of price expectations but, more importantly, a liquidity gauge. The article provides an example to grasp this critical point. Per the article:

Liquidity is variable. Changes in sentiment or policies, for example, can quickly alter liquidity. When liquidity is high, many buyers and sellers are poised to act on prices at or very close to current market prices.

As we discussed in our earlier example, selling or buying 20 shares of Apple, even if done repeatedly, will have little to no effect on price. In such an environment, the price will move up and down as factors change, but the movement will be gradual.

Now consider a market in which each 20-share purchase of Apple moves the stock by a nickel or more. In this circumstance liquidity is weak, and prices are susceptible to a motivated buyer or seller. In such instances, daily price moves in Apple are much more elevated than in the liquid market example. Accordingly, Warren Buffett could easily introduce significant downside pressure in such a market.

This example shows how liquidity is the critical determinant of volatility.

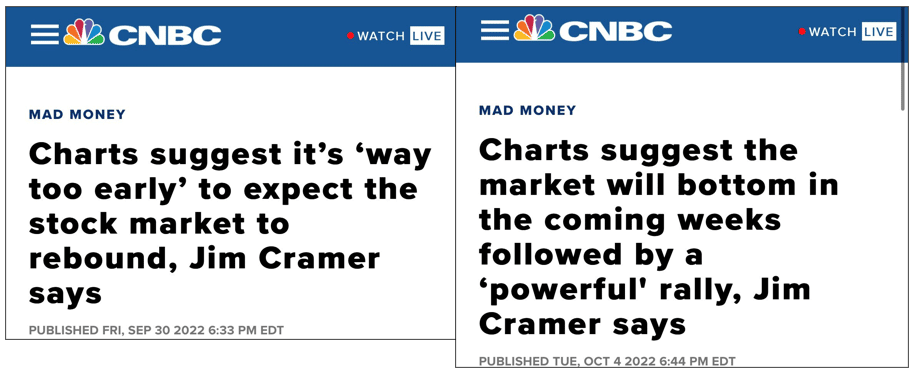

Follow Jim Cramer at Your Own Risk

Jim Cramer of CNBC commands one of the largest audiences in the financial media. His bubbling personality and the consistent barrage of investment ideas and market guidance make him powerful. While some may put trust in Jim, we offer caution. He tends to be wishy-washy during periods of volatility. As we show below, in the span of just two days, Cramer went from a bear to a mighty bull. While the price action leading to his change of heart was bullish, the fundamentals leading the market lower have not changed. Follow Jim with caution!

“Not So Fast”

For those investors thinking a Fed pivot is in the works, you may want to reconsider. Atlanta Fed President Bostic, along with his colleagues, seems to squash that narrative on a daily basis. In a speech given Wednesday, entitled Staying Purposeful and Resolute in the Battle against Inflation, Bostic states:

“I am not advocating a quick turn toward accommodation. On the contrary. You no doubt are aware of considerable speculation already that Fed could begin lowering rates in 2023 if economic activity slows & inflation starts to fall.

I would say: NOT SO FAST.”

He ends the speech by reiterating, as clearly as possible, the Fed has one purpose today- bringing down inflation.

I hope I’ve made it clear that I will be purposeful and resolute in the quest to bring down inflation. We cannot waver because price stability is necessary for us to achieve sustained maximum employment and to pursue an economy that works for everyone.

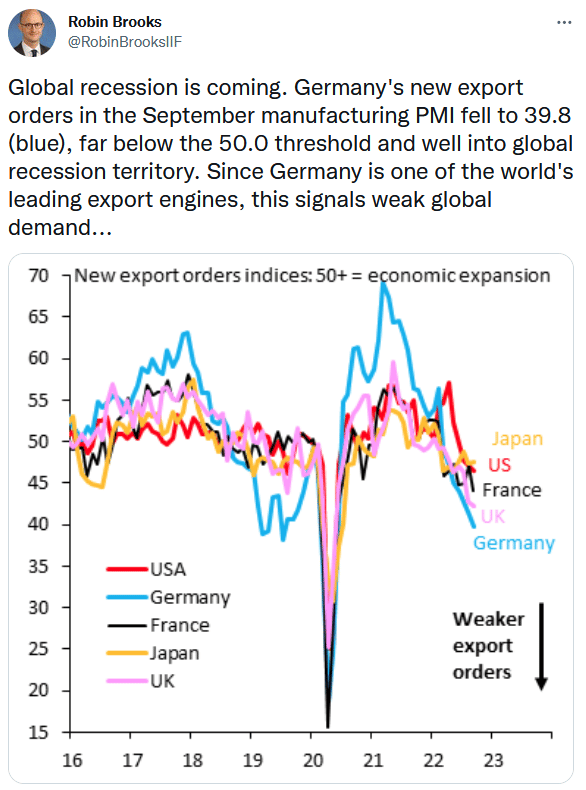

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.