The market’s short-term memory problem – Today’s Magnificent 7 was yesterday’s Maleficent 7.

Market watchers like to hang their hats on easy-to-discuss pegs. This year’s favorite might be Magnificent 7 or the high performers: NVDA, META, TSLA, AMZN, AAPL, MSFT, and GOOGL. These 7 stocks have been dragged out to highlight what is wrong with today’s rally. The rally is too narrow. Most stock are not participating.

The problem with looking at just this year and not the long term is that it ignores reality.

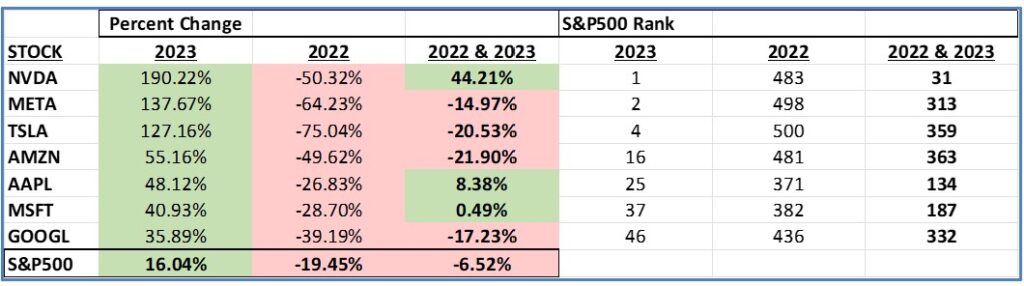

Looking at the performance table below of 2022 and 2023, we can see that:

- The Magnificent 7 were among the worst performers in 2022.

- All of the Mag 7 stocks underperformed the S&P500 by a wide margin last year

- NVDA, META, and TSLA, which rank 1,2, and 4 this year, ranked 483, 498, and 500 in 2022

- Only 3 of the Mag 7 stocks are positive over the 2022 and 2023 period

- The highest-ranked stock of the Magnificent 7 in the 2022 + 2023 period is NVDA at 31

- The average ranking of the Mag 7 stocks in the 2022 + 2023 period is 246 or right in the middle of the entire S&P500

(All relative performance charts are provided below)

The pundits will point to the fact that the average S&P500 stock is only up 8.15% this year, while the S&P500 is up 16% because of the heavy weighting of the Mag 7. These same analysts were wringing their hands last year when the S&P500 was down 19%, but they did not mention that the average stock was only down 10% last year. Why does the worry about index weightings only cut one way? Because fear sells news.

In fact, In a recent WSJ/Marketwatch article, it was noted that most Wall Street analysts started the year predicting trouble for stocks. They also recommended cash, treasuries, and commodities. For stock sectors, they liked Energy and Financials. All of these predictions proved inaccurate as stocks soared, with TECH and Consumer stocks leading the way.

The truth is that large money managers utilize the largest cap stocks for 2 logical reasons:

- Since these large stocks make up much of the benchmark indexes and investors do not want to risk underperforming their benchmarks, they have to be in these stocks.

- The largest cap stocks are the most liquid and, therefore the easiest to get in and out of. They are the first stocks investors pile into at the sign of a bull market and the first stocks they sell when there is trouble.

Jeff Marcus founded Turning Point Analytics (TPA) in 2009 after 25 years on trading desks and 13 years as a head trader to provide strategic and technical research to institutional clients. Turning Point Analytics (TPA) provides a unique strategy that works as an overlay to clients’ good fundamental analysis. After 10 years of serving only large institutions, TPA now offers its research services to mid and small managers, RIA’s, and wealthy sophisticated individuals looking for a way to increase their returns and outperform their peers.

Subscribe 2 Week Trial

Customer Relationship Summary (Form CRS)