The September NFIB Small Business Optimism Index (blue) fell to 90.8 from 91.3, remaining near the lowest levels since the financial crisis. The forward-looking NFIB business outlook (orange) dropped to -43. Such is above the low registered in mid-2022 but below levels reached during the financial crisis. 23% of small business owners deem inflation as their most important problem. The other big problem almost half of those surveyed by the NFIB face is finding qualified employees.

Within the NFIB report, we found the following quote: “The frequency of reports of positive profit trends was a net negative 24%, up one point from August. Among owners reporting lower profits, 29% blamed weaker sales, 20% blamed the rise in the cost of materials, 15% cited labor costs, 8% cited lower prices, 7% cited the usual seasonal change, and 6% cited higher taxes or regulatory costs.” Losing money on weaker sales is a recipe for job layoffs and other budget cuts. Given small businesses account for almost 50% of the workforce, we fear layoffs may increase to help offset weaker sales and declining or negative profits.

What To Watch Today

Economics

Earnings

Market Trading Update

A few of our readers asked us why bond ETF prices were down Wednesday morning despite bond yields falling sharply. The U.S. bond market was closed Monday for Columbus Day, but the futures and equities markets were open. Bond futures rose sharply Monday as the Israeli war news provoked a flight to quality. Bond ETFs followed futures higher on Monday.

On Tuesday, futures and ETFs opened lower, giving up some of the gains. However, because the bond market was closed on Monday, Tuesday’s opening bond yields were sharply lower, reflecting yield changes on Monday and Tuesday. The two-day changes in futures, ETFs, and bonds are now similar.

Such divergences happen daily, albeit they tend to be small. Bonds stop trading at 2 p.m. ET, while ETFs close at 4 p.m. ET. Accordingly, changes in the bond futures market between 2 p.m. and 4 p.m. cause the prices of ETFs to change while bonds remain fixed at their 2 p.m. closing levels. Again, any differences will be made up the next trading day. Arbitrage between futures, ETFs, and bonds is incredibly easy, meaning that any divergences, like those mentioned above, are only optical.

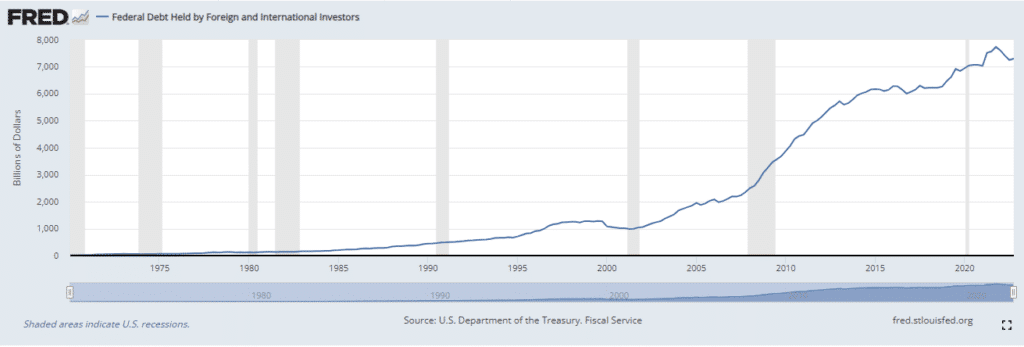

There is also a false narrative about foreign Governments selling U.S. Treasuries as “they don’t want our debt.” As shown, such is clearly not the case. More importantly, in times of war, financial stress, or other events, foreign reserves will seek the safety of U.S. Treasuries, such as we saw these past few days.

Fed Inching Towards A Pause

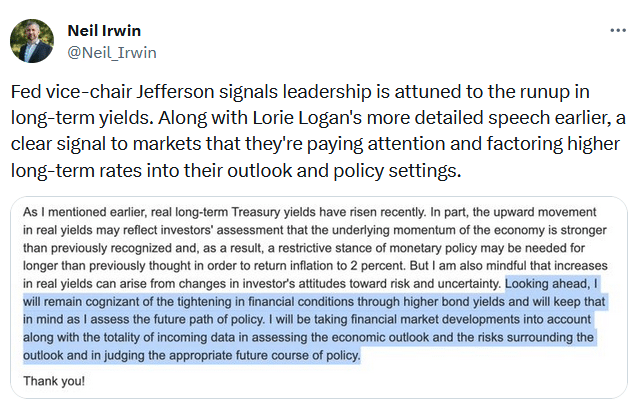

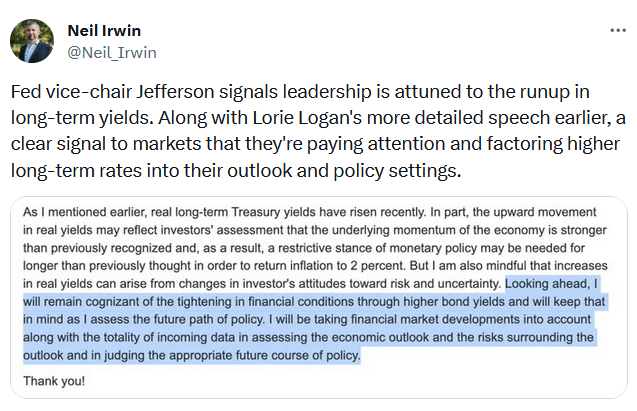

Yesterday, we noted that Fed Dallas President Lorie Logan was explaining how the recent spurt in long-term interest rates was a factor that should further restrict economic growth and, therefore, inflation. On her heels, Vice-Fed Chair Jefferson made similar comments, as we share below.

We believe Fed members’ insistence on repeating “higher for longer” is designed to keep long-term rates high. While unsustainable in the long run, such action would eventually slow the economy and weaken inflation. Based on Logan’s and Jefferson’s recent comments, they seem content that long-term interest rates may be doing their job for them.

On Tuesday morning, Fed President Bostic took the more dovish stances noted above a step further. He said we don’t need to increase rates anymore. This afternoon’s FOMC minutes from their prior meeting may paint a more dovish stance than the market assumed a few weeks ago. While we would like confirmation from Powell, the rumblings from other Fed members may likely mean the Fed will not increase rates anymore this cycle, barring an unforeseen jump in economic activity and or a resurgence in inflation.

The False China Bond Narrative

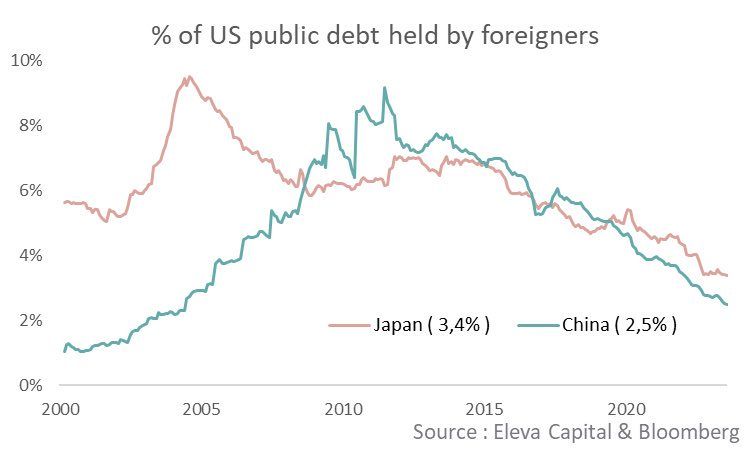

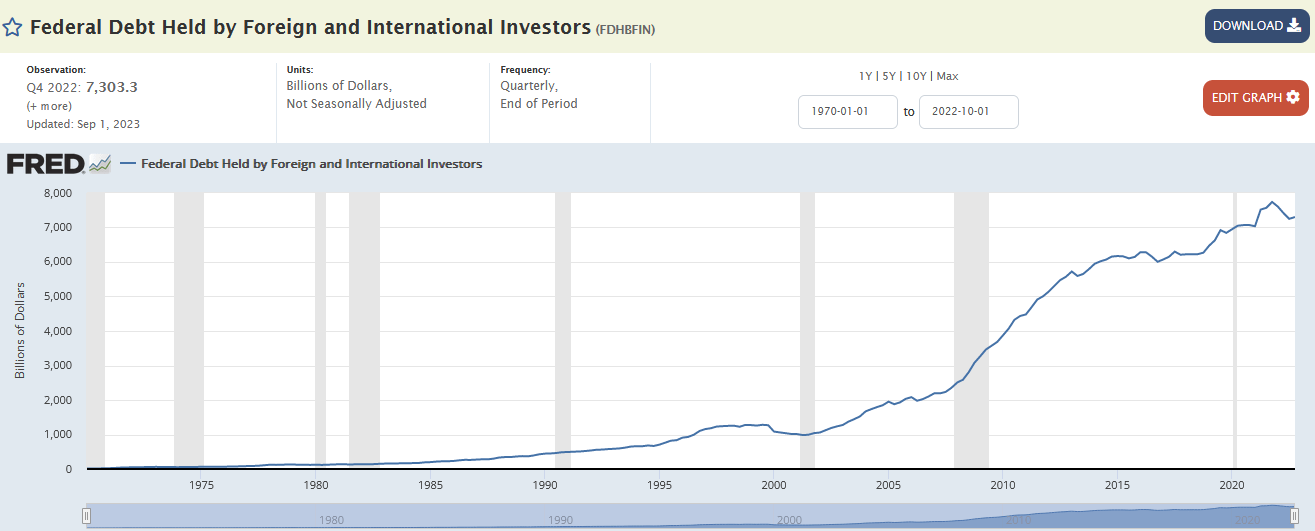

There is a narrative floating around the bond market claiming the Chinese and Japanese are responsible for the recent spate of higher bond yields. Rumor has it they are aggressively selling, resulting in higher yields. Based on U.S. Treasury data, the year-to-date change in Japan’s holdings of U.S. Treasury securities is up by $37 billion, and China’s have declined by $46 billion. The graph below, courtesy of Eleva Capital, shows a steady decline in their holdings. However, remember that the amount of debt has risen significantly while their holdings remain relatively constant. Further, the second graph shows that debt held by all foreigners is stable if not slightly increasing.

We would be remorseful if we didn’t discuss how much they own. Japan and China hold about $1.1 trillion and $800 billion of U.S. Treasuries. While that may seem significant, they pale compared to the largest holder of Treasuries, the Federal Reserve. The Fed owns about $8 trillion. Even if China or Japan were to sell aggressively, the Fed could easily step in and absorb their selling pressure.

Foreign selling doesn’t explain the recent jump in interest rates, and neither does “soaring” debt issuance, as we will address tomorrow.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Post Views: 1

2023/10/11