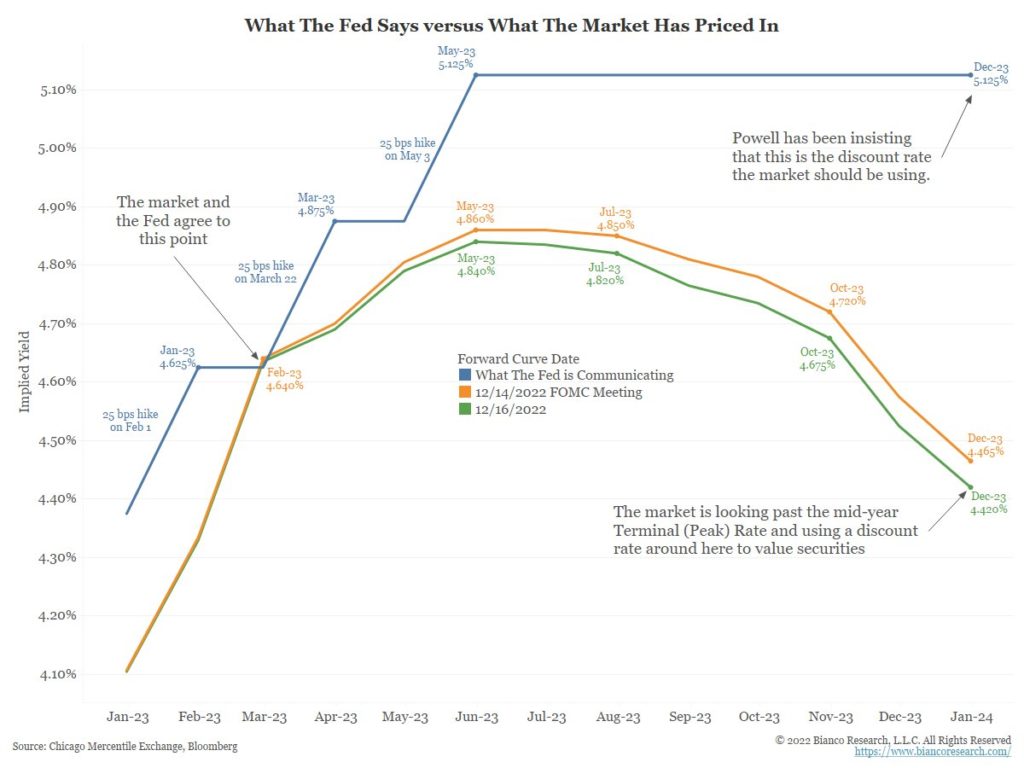

The road map for 2023 may continue to depend heavily on the Fed’s monetary policy stance. In January 2022, we warned readers not to fight the Fed. The Fed was going to raise rates more aggressively than was being acknowledged. The road map for 2023 is different with Fed Funds over 4%, QT is in full operation, and the terminal Fed Funds rate is in sight. The graph below, from Jim Bianco, helps appreciate the road map for 2023. If Powell sticks with the blue line, as he avows, keeping Fed Funds at 5% or greater for the year, the market is underestimating the Fed’s resolve. Therefore, equity weakness will likely continue as investors price in a more restrictive monetary policy. Conversely, if the green line showing the market-implied Fed Funds rate turns out to be the correct road map, 2023 may be a friendlier year for investors.

Our concern is there is a third route not shown in the graphic. If financial instability crops up or the economy weakens much more than expected, both paths in the graph may overestimate where Fed Funds will be in 2023. In the “something breaks” scenario, an aggressively easing Fed may not be the panacea for the weak market investors are hoping for.

What To Watch Today

Economy

- 8:30 a.m. ET: Housing Starts, November (1.400 million expected, 1.425 prior)

- 8:30 a.m. ET: Building Permits, November (1.480 million expected, 1.526 million prior)

- 8:30 a.m. ET: Housing Starts, month-over-month, November (-1.8% expected, -4.2% prior)

- 8:30 a.m. ET: Building Permits, month-over-month, November (-2.1% expected, -2.4% prior)

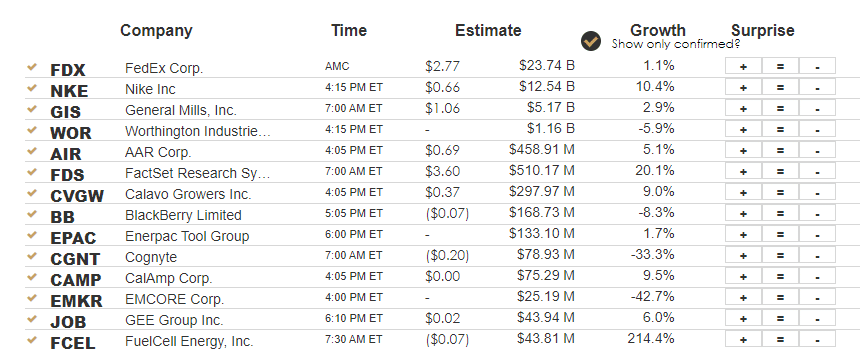

Earnings

Market Trading Update

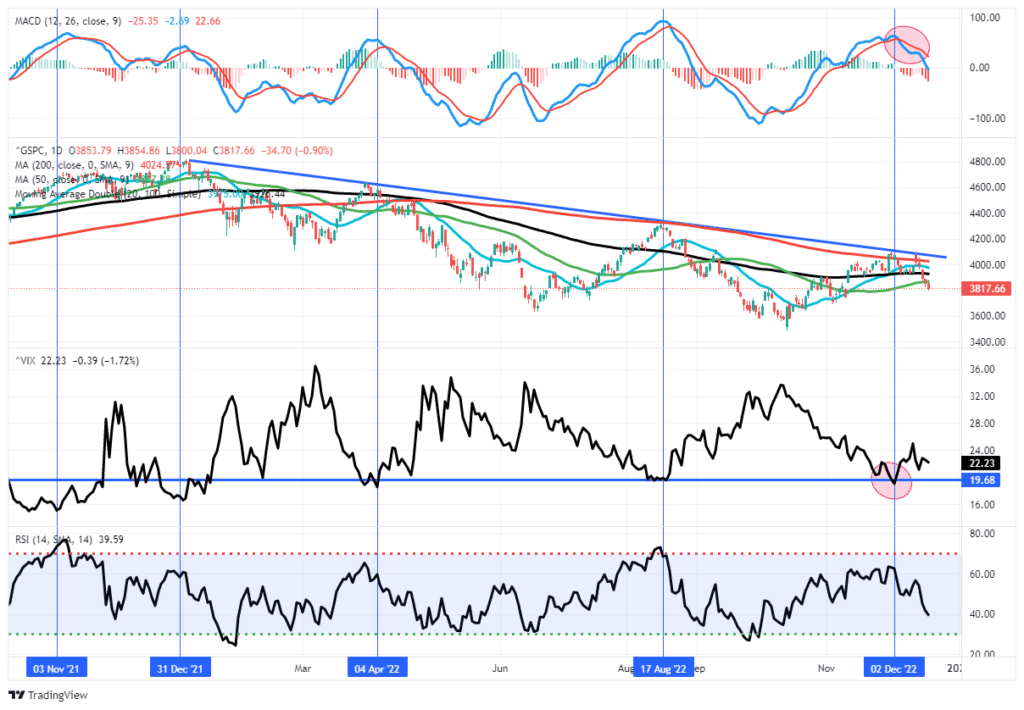

The market traded lower yesterday, confirming the break of the 50-DMA, and is targeting very minimal support at the late October lows. With the market getting decently oversold short-term, it is now or never for the “Santa Rally” to manifest itself. As we have stated previously, there is no guarantee a rally will develop, but the seasonal tendency is strongest over the next few trading days heading into year-end. The big concern is that the market is starting to come to grips with the realization the Federal Reserve is NOT going to pivot any time soon.

Early this morning, futures are lower again as Japan unleashes havoc on the bond market with changes to its “yield curve control” program.

“the functioning of bond markets has deteriorated, particularly in terms of relative relationships among interest rates of bonds with different maturities and arbitrage relationships between spot and future markets… If these market conditions persists, this could have a negative impact on financial conditions.”

The BoJ also increased its bond purchases to JPY9 trillion monthly for January through March.

Remember that the share of Japanese government bonds held by the Bank of Japan has topped 50% on a market value basis for the first time, new data showed Monday.

Technically, the setup suggests we could see additional downward pressure on stocks today. Remain cautious and continue to hold higher levels of cash.

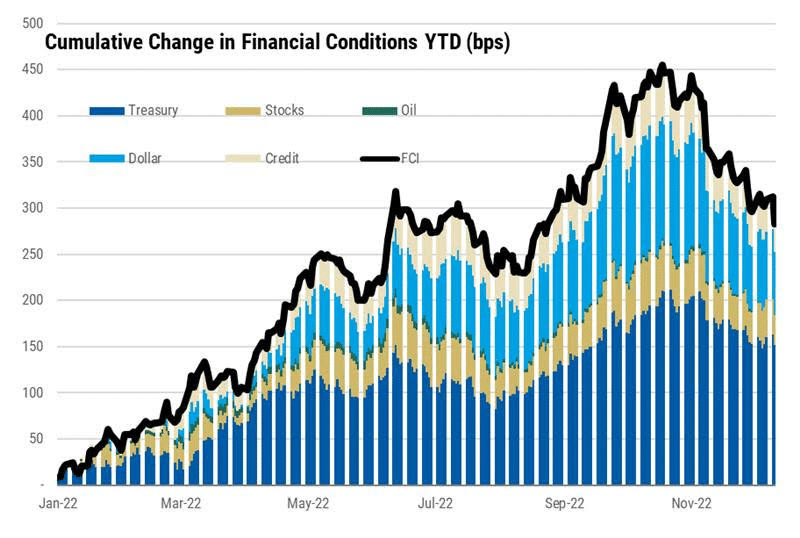

Financial Conditions Ease

The graph below shows that financial conditions have been easing for the past six weeks. While this may help markets and possibly strengthen the economy on the margin, the Fed does not like it. At last week’s FOMC press conference, Powell said it is important for financial conditions to properly reflect the Fed’s monetary policy and inflation goals. The bottom line, the Fed will likely maintain its hawkish rhetoric and try to prevent financial conditions from easing further. In the past, they have said asset prices, including stocks, strongly affect the economy and, therefore, inflation. As such, the Fed will likely adhere to the blue road map for 2023 laid out above unless something breaks.

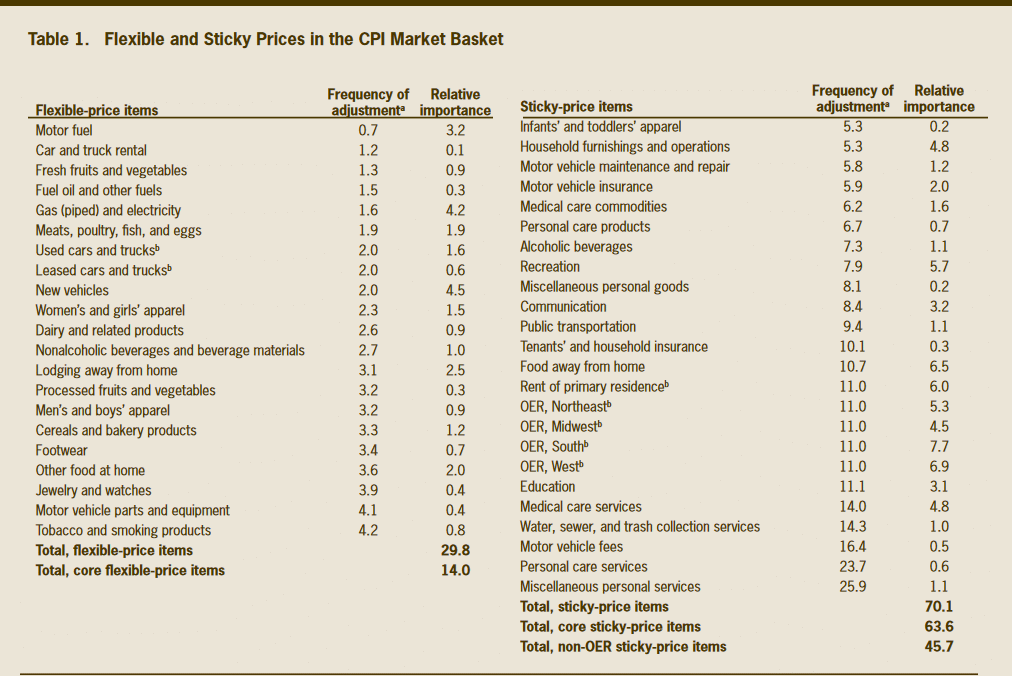

Sticky vs. Flexible Inflation

The graph below from the Atlanta Fed shows the stark divergence between sticky and flexible inflation. Sticky inflation measures prices for products that tend to be less volatile. Conversely, flexible inflation is based on products with prices that vary up and down based on economic conditions. The table below the graph shows how the Atlanta Fed classifies products into both categories.

Many comparisons are currently being drawn to the 1970s, but the graph warns that this inflation outbreak may differ. Forty years ago, flexible and sticky prices were moving in lockstep. Today sticky prices are proving to be sticky while flexible prices decline rapidly. If the trends continue, inflation will likely decline further, but it may not fall as quickly or by as much as the Fed prefers.

BlackRock Warns of a Deep Recession and Volatile Markets

Market Insider shares BlackRock’s economic outlook, and it is not pretty. The article starts as follows:

A worldwide recession is just around the corner as central banks boost borrowing costs aggressively to tame inflation — and this time, it will ignite more market turbulence than ever before, according to BlackRock.

BlackRock thinks this recession will be very different from prior recessions as central bankers are still fighting inflation which precludes their ability to “ride to the rescue” when economic growth and markets falter. They believe corporate earnings expectations, which still point to positive growth in 2023, aren’t reflective of a modest recession. Their advice:

The prospect of limited policy support means investors need more dynamic methods — involving more frequent portfolio changes and taking a more “granular view on sectors, regions and sub-asset classes” — to navigate the volatility ahead, according to BlackRock.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.