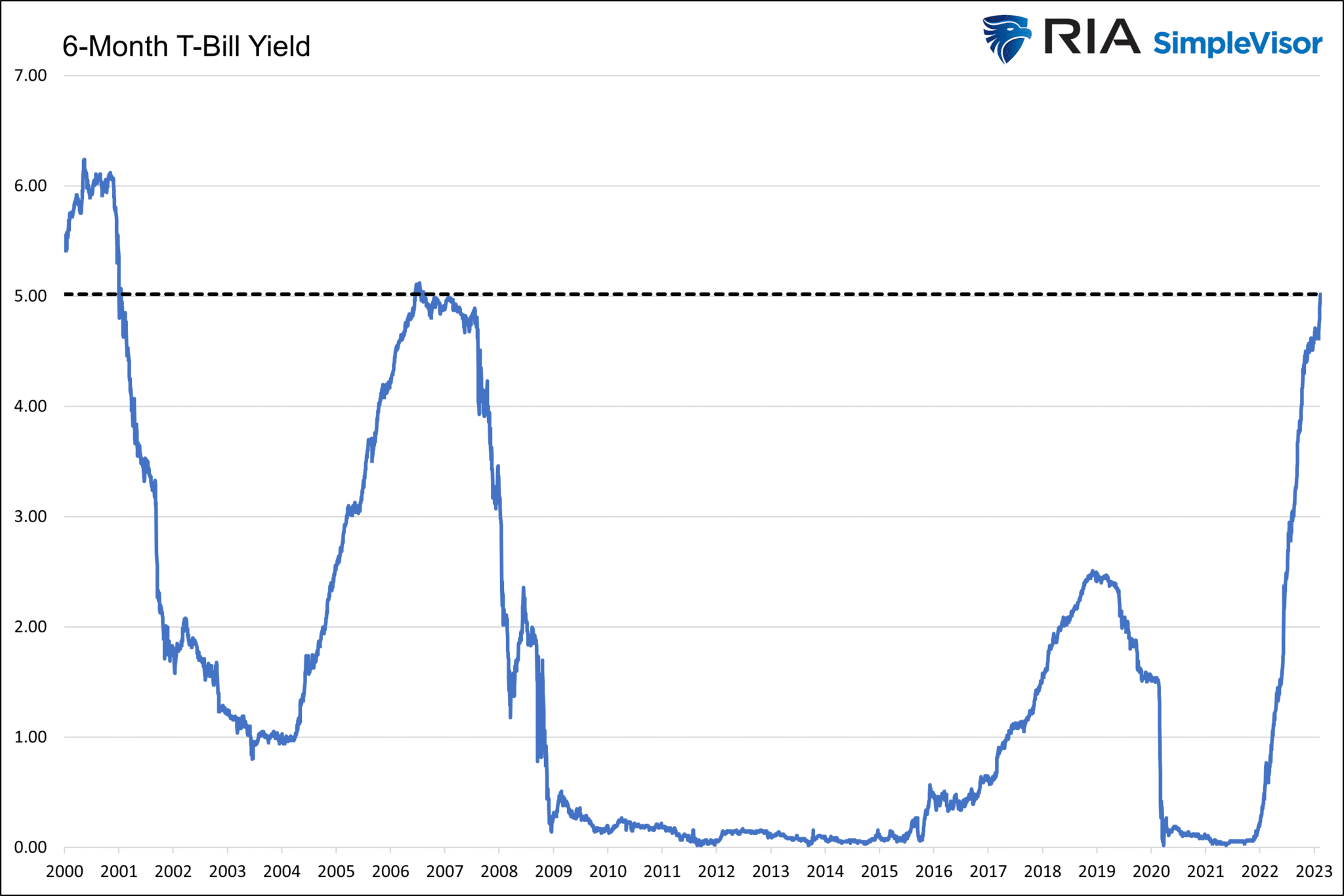

6-month and 1-year Treasury bills yields are above 5 percent, marking the first time a Treasury yield was over 5% since 2006. Savers are enthused at the prospect of earning a historically excellent risk-free return. On the other side of the coin are stock investors. Their decision-making is becoming more complex. Are they willing to bet that stocks will post a return of greater than 5 percent? Since 1970, the average annualized return on the S&P 500 is 7.39%, and about two-thirds of the annual returns were above 5%.

Statistically speaking, the logic of chasing stocks appears to make sense even when you can invest at a 5% risk-free rate. But we must consider that the Fed is raising rates and purposely trying to slow economic growth. Since 1970, the average annual returns were 3.9% and 5.0% in years in which the Fed increased or decreased rates by more than 50bps. Years in which the Fed was inactive averaged 11.8%. If the Fed increases rates at least one more time or pivots and lowers them considerably later this year, odds argue the risk-free 5 percent bond is a better option than stocks.

Further, consider risk-free yields at levels where professional money managers can over-allocate to cash or short-term Treasuries and earn competitive yields with potential equity returns. Such an environment will lead some to sell stocks and move to Treasuries.

What To Watch Today

Economy

- 8:30 a.m. ET: PPI Final Demand, month-over-month, January (0.4% expected, -0.5% prior)

- 8:30 a.m. ET: PPI Excluding Food and Energy, month-over-month, January (0.3% expected, 0.1% prior)

- 8:30 a.m. ET: PPI Final Demand, year-over-year, January (5.4% expected, 6.2% prior)

- 8:30 a.m. ET: PPI Excluding Food and Energy, year-over-year, January (4.9% expected, 5.5% prior)

- 8:30 a.m. ET: Housing Starts, January (1.353 million expected, 1.382 prior)

- 8:30 a.m. ET: Building Permits, January (1.350 million expected, 1.330 million prior)

- 8:30 a.m. ET: Housing Starts, month-over-month, January (-2.1% expected, -1.4% prior)

- 8:30 a.m. ET: Building Permits, month-over-month, January (1.0% expected, -1.62% prior)

- 8:30 a.m. ET: Initial Jobless Claims, week ended Feb. 11 (200,000 expected, 196,000 prior)

- 8:30 a.m. ET: Continuing Claims, week Feb. 4 (1.689 million expected, 1.688 million prior)

- 8:30 a.m. ET: Philadelphia Fed Business Outlook Index, February (-6.9 expected, -8.9 prior)

- 8:30 a.m. ET: New York Fed Services Business Activity, February (-21.4 prior)

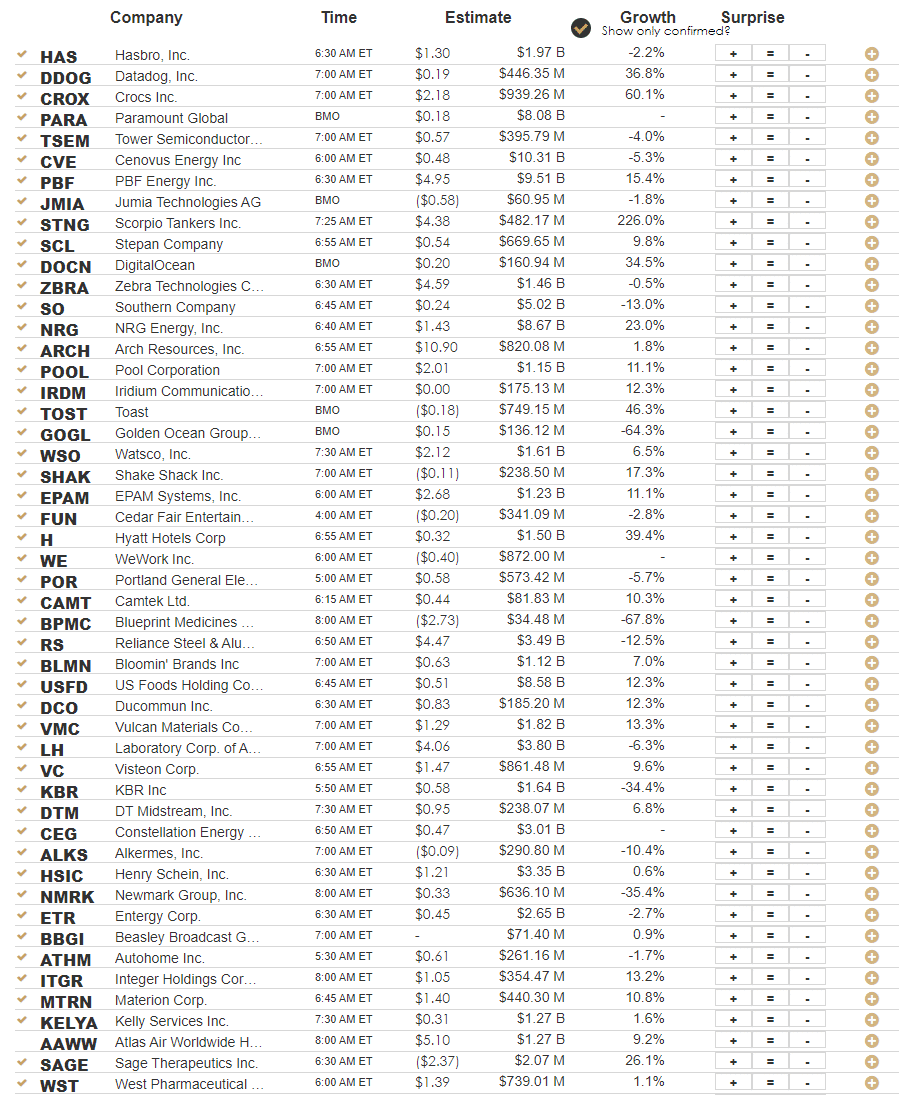

Earnings

Market Trading Update

While the market continues to hold support above the 20-DMA as key initial support, going nowhere is working off some short-term overbought conditions. While the market remains clearly bullish, with buyers stepping in and buying dips, bonds have worked much further through its sell signal and overbought conditions.

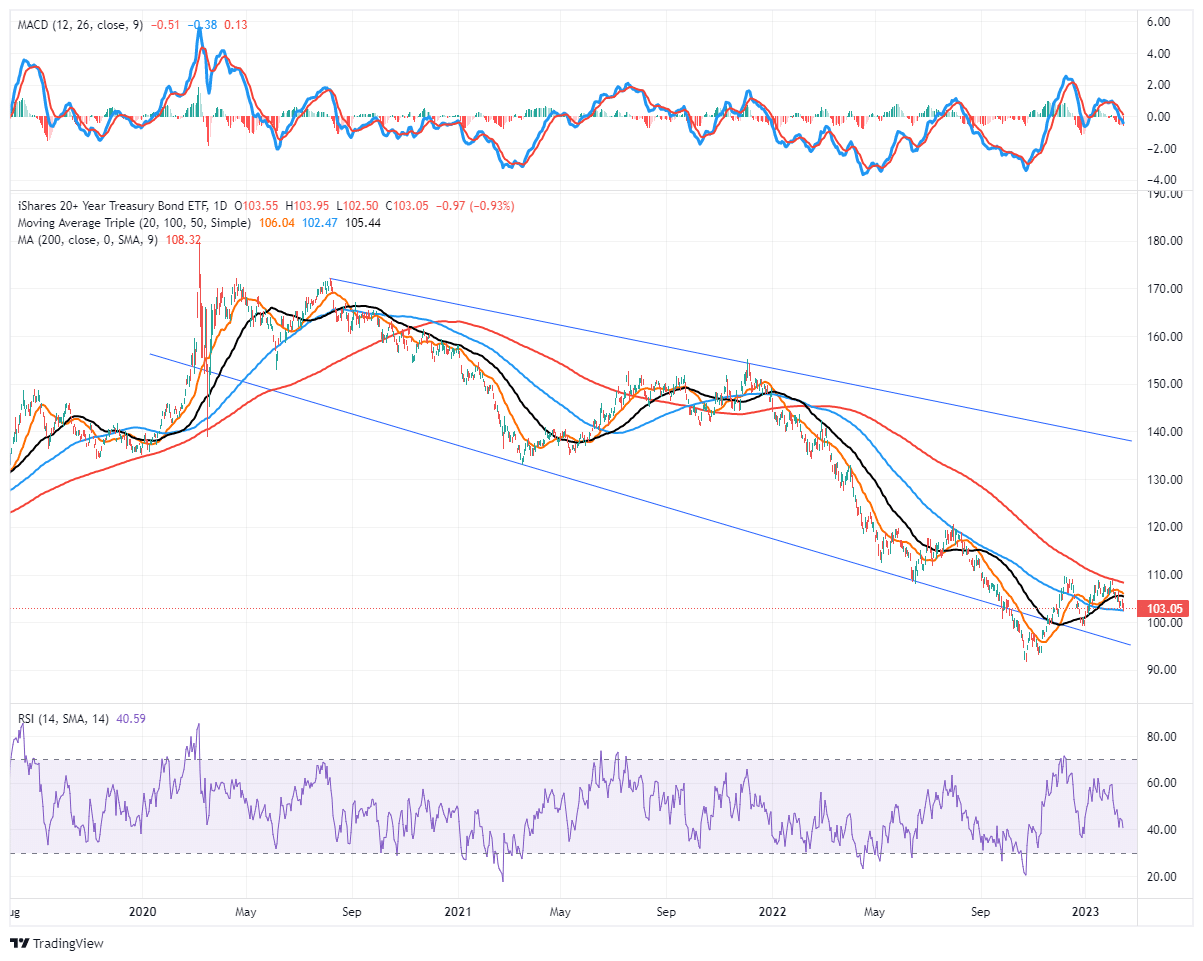

With respect to bonds, we are using TLT as a proxy for the Treasury Bond market. The support level 100-DMA continues to provide key support. The 50-DMA has not crossed above the 200-DMA yet, but such will likely happen on the next rally in bond prices. That could very well happen in the next month or two as economic weakness becomes more prevalent following the lag of the Fed rate hikes from last year.

We are watching closely for the next buying opportunity for bonds. While we are not there just yet, that opportunity is likely coming fairly soon. With the Fed still hiking rates, it may not be long before we get a key bond entry point. However, when the Fed eventually pivots, that will likely be the bottom for bond prices for quite some time.

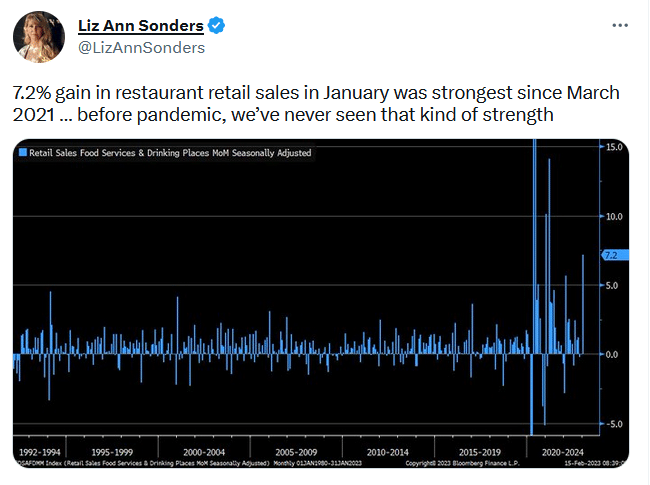

January Retail Sales Were Enfuego

Retail sales surged in January by 3%, almost double the +1.8% expectation. The strength was led by department store sales rising 17.5% and restaurants and bars climbing 7.2%. Both figures are monthly changes! All 13 of the broad categories were higher. Such was the first time that occurred since covid. While the data is great there is an important consideration. As Zero Hedge notes:

“Adjusting nominal retail sales for CPI shows that Americans’ real spending has gone practically nowhere for ten straight months..”

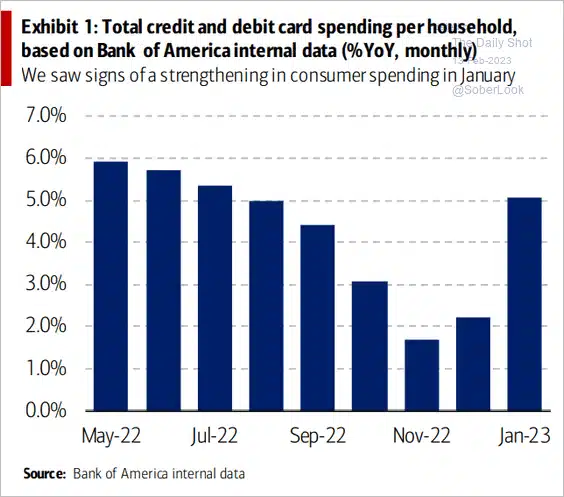

In Monday’s Commentary, we shared the following graph. Putting two and two together, it appears many consumers are borrowing to continue buying the same amount of stuff, thereby keeping up with inflation. Inflation will not fall quickly to the Fed’s liking if consumers can continue to borrow and spend.

Will China Consumer’s Generate an Inflationary Impulse?

Much ado is being made about China lifting its strict covid protocols and the potential spending boom that will ensue. If Chinese consumers spend as Americans did in 2021, global inflationary pressures would again rise. However, while a surge in spending commensurate with the easing of covid restrictions makes sense, the graph below argues that Chinese consumers may not be as quick to spend as is commonly believed.

HOPE

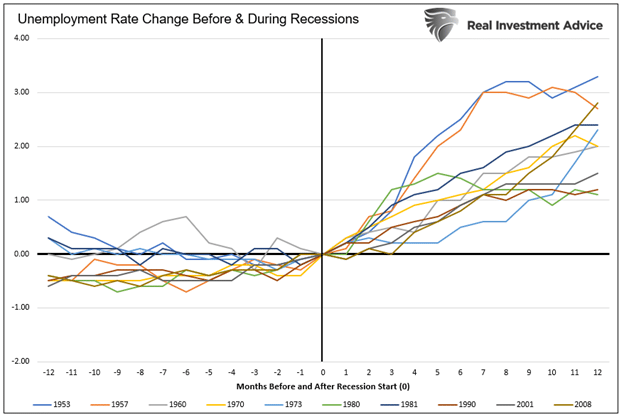

The Fed is tightening monetary policy at the fastest pace in over 40 years. Furthermore, the economy is more leveraged now than at any time in history and, therefore, more sensitive to interest rate increases. It seems naïve to assume a recession is not probable because a lagging economic indicator, like employment, is robust.

The following quote comes from our recent article- Janet Yellen Should Focus on HOPE. The article is a rebuttal of sorts to the following comment made by Treasury Secretary Janet Yellen: “You don’t have a recession when you have the lowest unemployment rate in 53 years.”

Employment is a lagging indicator that often deteriorates once a recession has started. The article works through the HOPE framework to appreciate the monetary policy lags and the sequence in which economic activity typically weakens before a recession. The E in HOPE is employment. As the graph shows, the unemployment rate didn’t rise during the last 11 recessions until the recession started.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.