Ford (F)

In our latest article, Cash Cows and Treasury Bonds we explore a handful of higher dividend, slow growth stocks to see what they can tell us about the future direction of Treasury yields. Within the analysis are a few stocks with higher-than-average dividend yields compared to their history and Treasury yields. Accordingly, shareholders may benefit from price appreciation if the dividend yield on those stocks reverts to their respective historical averages.

One of these stocks is Ford (F).

This analysis builds on the Friday Favorites Campbell Soup article from two weeks ago.

Dividend Yield Analysis

Ford has a dividend yield of 5.67%, almost 2.50% higher than its five-year average. Furthermore, its dividend yield is 1.84% more than the 10-year UST yield. Such is .23% higher than its average dividend yield spread to Treasuries over the last five years. On average, the fifteen stocks we highlight in the Cash Cow article are trading with dividend yield spreads to Treasuries of .80% below the average.

Ford shares plummeted by nearly 20% in July on a poor earnings report. As a result, its dividend yield jumped by 1.10%, as shown below.

Typically, higher bond yields imply greater default risk. In the case of F, the credit risk, as measured by the credit default swap market, jumped after the earnings announcement but has since settled back to where it has been for much of the year, as shown below. Furthermore, its perceived credit risk is well below the levels of the last two years.

Fundamentals

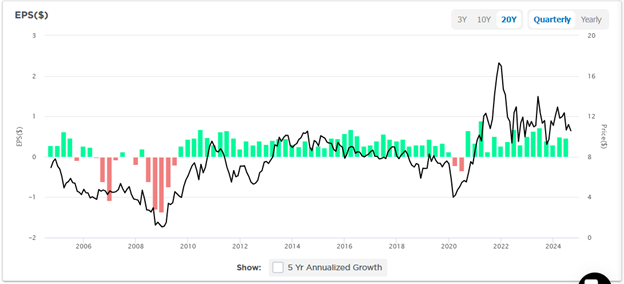

The first two graphs below show Ford’s revenues and earnings per share have stagnated for the last 20 years. Likewise, its debt outstanding, which has risen over the previous two years, is still below the peak in 2020 and levels seen before the financial crisis.

An essential question for Ford’s shareholders is whether they can continue to afford to pay the current dividend. Over the last ten years, excluding the early part of the pandemic, Ford’s payout ratio, or the proportion of earnings it pays shareholders in the form of dividends, has varied between 25-50%. Ergo, barring a sharp slowdown in earnings or an aggressive capital spending plan, Ford should maintain the ability to pay its dividend.

Another way to gauge its ability to continue its current dividend is its free cash flow yield. This measures its free cash flow as a percentage of its market cap. The company should have adequate funds to pay the dividend if it is higher than its dividend yield. As the chart from Zacks shows, its free cash flow yield has been well above its dividend yield.

Further, Ford has significant debt. If interest rates continue to fall, this should allow the company to refinance some of its recently issued higher-yielding debt at lower rates.

We should not expect meaningful earnings or revenue growth because of its track record. This is reflected in its valuations. Ford has a forward P/E of 5.50 and a price to sales of 0.24. Its price-to-book value is slightly below 1.0, the lowest in the last ten years, excluding 2020.

As highlighted by the blue lines in the first graph, the stock has been rangebound for the last two years. At times, it has popped above the channel, and like today, it has traded below the channel. Its MACD in the upper graph is turning into a bearish signal, but its RSI is relatively low, so the downside may be limited.

The second graph shows the stock has been volatile but has gone nowhere for the last 25 years. Using both graphs, we might expect it to move upward toward the middle of the short-term channel. Still, we highly doubt that considerable upside is possible, barring significant changes to their business model.

Tying the dividend yield analysis to the fundamentals is interesting. Currently, five-year Ford bonds yield 5%. The stock dividend yield is 5.67%. The extra yield doesn’t seem like enough, given bondholders will do much better than stockholders in the case of default. However, the upside potential in the stock price, albeit limited, and the extra dividend yield make Ford a compelling investment for those seeking income.

We caution you that it is a risky investment, and as we saw with GM, a default is not out of the question.

We recommend using tight stop loss levels if you buy the stock.

Disclosure

This report is not a recommendation to buy or sell the named securities. We intend to elicit ideas about stocks meeting specific criteria and investment themes. Please read our disclosures carefully and do your own research before investing.