The administration warned that job growth would cool off in last Friday’s employment report. The economy added 315k jobs, slightly better than expectations but short of last month’s +526k. Job growth may be “cooling,” but it is still red hot. As shown below, job growth of 315k is nearly 3x the long-term average and in the upper end of data going back to 1940. The unemployment rate rose 0.2% to 3.7%, but that is good news. It increased because the participation rate jumped from 62.1% to 62.4%. People that have not been working or seeking a job are reentering the job market. The Fed will like that stat as an increasing number of job seekers will reduce the tightness in the labor market.

What To Watch Today

Economy

- 9:45 a.m. ET: S&P Global U.S. Services PMI, August final (44.2 expected, 44.1 prior)

- 9:45 a.m. ET: S&P Global U.S. Composite PMI, August final (45.0 expected, 45.0 prior)

- 10:00 a.m. ET: ISM Services Index, August (55.2 expected, 56.7 prior)

Earnings

- No significant earnings releases today

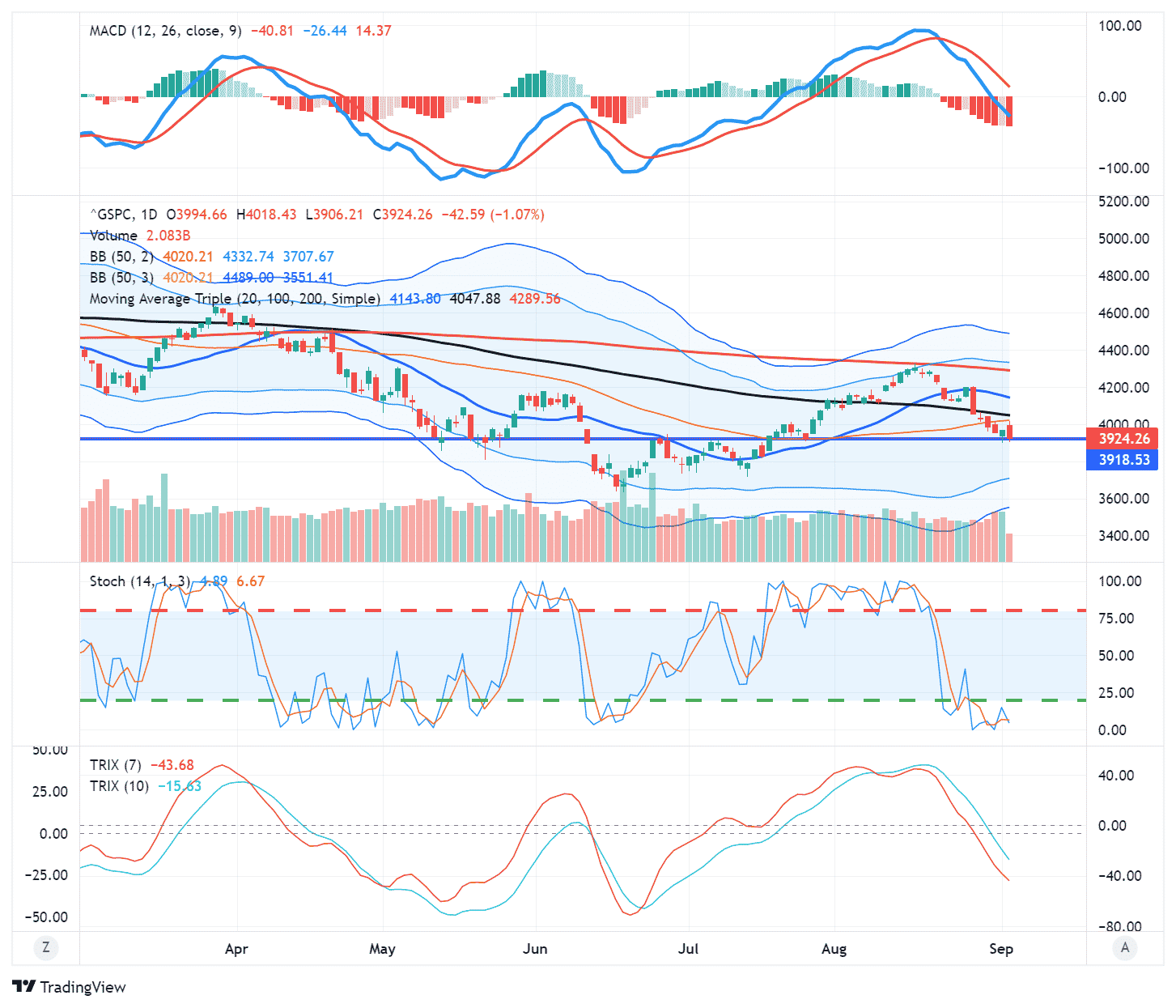

Market Trading Update

The bull rally failed as those stating the rise from the July lows was a “bear market rally” were proven correct. As we said Friday before last:

The break of the 100-dma also sets the market up for a retest of the 50-dma next week. Given the sharp market sell-off on Friday, some follow-through selling on Monday would be of no surprise.”

That was the case as the market sold off sharply all week, taking out the critical 50-day moving average. However, with the markets deeply oversold, a reflexive bounce is likely. The market attempted a test to break above the 50-dma but failed. With the market sitting on important support, an attempt at a rally this week is likely. However, with the MACD on a “sell signal,” we continue to suggest selling any rallies to reduce risk.

Unfortunately, the bull rally’s failure suggests more challenges for the stock market. As noted by Yahoo Finance:

“The historically volatile month of August lived up to its reputation.

Call it par for the course for 2022, as the Federal Reserve’s resolve to fight inflation again beat back the most optimistic bulls holding out for the elusive Powell pivot.

By the numbers: The Nasdaq Composite sank another 4.6% in August, bringing its year-to-date return to -24.5%. Meanwhile, the Dow is now off 4,828 points for the year, or 13.2%, and the S&P 500 is 17% in the hole.”

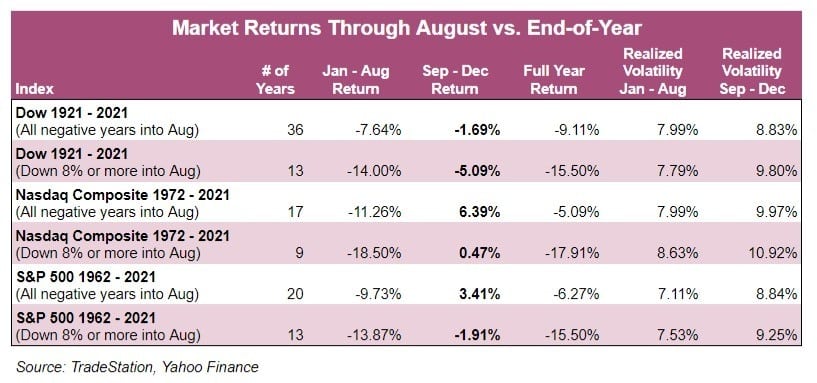

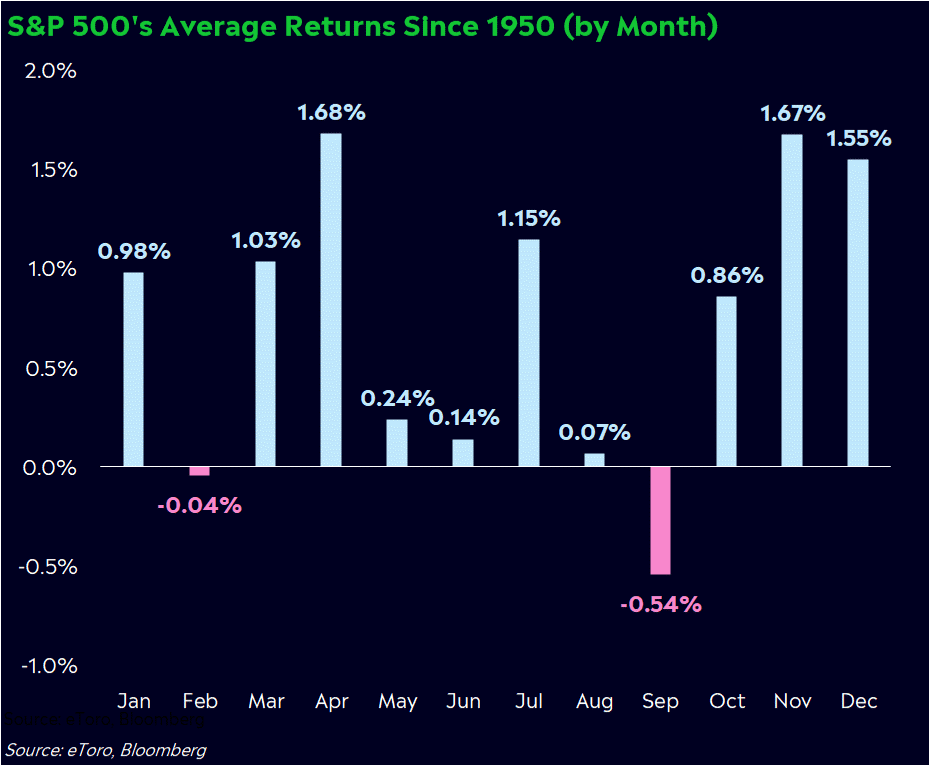

Unfortunately, for investors, the market history books suggest that when markets have negative returns this far into the year, it portends more weakness and volatility into year-end.

Furthermore, while we could certainly see another bull rally from currently very oversold conditions, the month of September offers little hope. October tends not to be kind, either.

The Week Ahead

The holiday-shortened week ahead will be quiet on the economic front. Jobless Claims will get the Fed’s attention as they continue to look for signs that job growth is slowing, and with it, labor market tightness will abate. Jobless Claims tend to lead the payrolls and unemployment data that the market is so keenly focused on. The only other data worth mentioning is ISM for the services industry. Expectations are for a slight tick lower but to a level (55) that is still commensurate with solid economic growth. The prices and employment subcomponents will likely garner the most attention.

We suspect various Fed members will continue to echo Powell’s hawkish rhetoric. While largely unexpected, we have heard a few market pundits wondering if the Fed might surprise markets with an intra-meeting rate hike. Such would undoubtedly get Powell’s point across that inflation-fighting trumps the health of the markets and the economy.

Got Lithium Batteries?

In our Got Lithium Commentary earlier this week, we discussed how the current production levels of lithium are not enough to keep up with global demand, mainly due to the proliferation of electric vehicles (EVs). Given the supply-demand imbalance, investments in lithium producers may be an excellent long-term investment. We follow that analysis up by looking at the lithium battery makers.

Almost 80% of the world’s lithium batteries are made in China. Asia, excluding China, produces 8%, while Europe and the U.S. produce 7% and 5%, respectively. The 10-year trajectory of battery production shifts toward the U.S. and Europe, but China, at 68.8%, will still have a monopoly on production. Given the surging demand for these batteries and yet another round of trade barbs between the U.S. and China, might attaining lithium batteries at fair prices become a problem for EV manufacturers? Shortages of chips in 2020 and 2021 reduced car production resulting in significantly higher prices. China is a crucial cog in EV production, and no doubt they understand their leverage. Investors of auto companies must consider how and when China might use its leverage.

Bear Market Legs

The table below shows that if this is a bear market, the worst may still be ahead. In 11 of the 16 bear markets shown below, the average decline in the last third period was double that of the 1st or 2nd legs. If we are in a bear market, which is not definitive as the market has not broken any longer-term trends, the question becomes its ultimate duration. For instance, are we still in the first third, there is still a lot of pain ahead. Conversely, if the bear market is only a year-long, we might be in the final third.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.