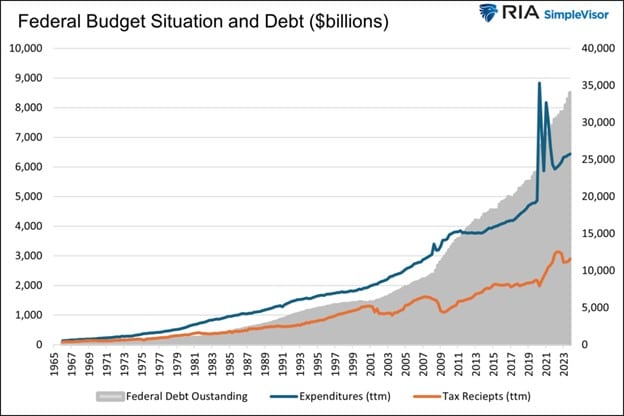

With inflation remaining sticky well above the Fed’s 2% target and the economy showing few signs of weakness, the Fed will find it difficult to cut rates meaningfully. Furthermore, ending QT and re-starting QE is much less likely in this environment. The problem with the Fed’s anti-inflationary stance is that it forces the government to pay higher interest expenses, further increasing deficits and debt issuance. A new version of QE, let’s call it QE Light, might be the solution. Our latest article, QE By A Different Name, dives into a QE Light rumor floating around the street.

QE Light could allow the Fed to support the Treasury while maintaining a hawkish bias. To do so, the bank regulators could remove all capital and leverage requirements on Treasury holdings for the largest banks. Next, they could employ a new version of the BTFP program, which they recently retired. Per the article:

In a new scheme, bank regulators could eliminate the need for GSIBs to hold capital against Treasury securities while the Fed reenacts some version of BTFP. Under such a regime, the banks could buy Treasury notes and fund them via the BTFP. If the borrowing rate is less than the bond yield, they make money and, therefore, should be very willing to participate, as there is potentially no downside.

What To Watch Today

Earnings

- No notable earnings releases

Economy

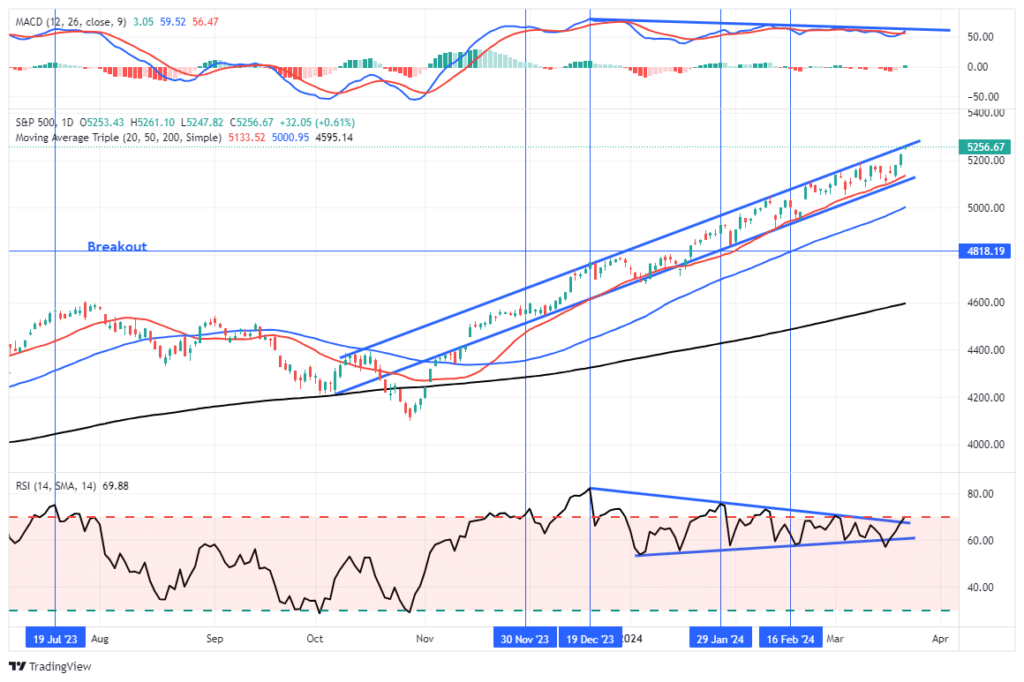

Market Trading Update

The most perfect trading trend continues uninterrupted.

Despite some previous deterioration in momentum, that was reversed quickly on Wednesday and Thursday following the FOMC announcement. Perceived as dovish, stocks got a strong bid from the 20-DMA and rallied to the top of the market’s ongoing “perfect trend.” As I noted yesterday morning on Twitter,

“If you can goal seek a market move…this is what it would look like. Trips to the bottom of the channel at the 20-DMA continue to get bought. Tops get sold. The algos remain in control for now.”

While the market has moved back onto a buy signal, it is back to overbought on both an RSI and MACD basis. There is no reason to be overly cautious as the bullish trend continues. The upside likely remains limited without a bigger correction first. However, we won’t need to worry about that until the 20-DMA is violated. That should trigger more selling as the computer algos switch from “buying dips” to “selling rips.”

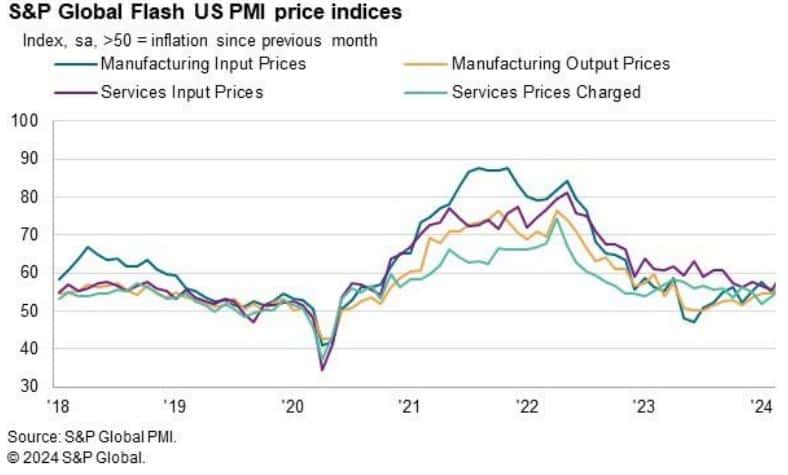

Flash PMIs Signal We’re in Good Shape

The S&P Global Flash PMIs for March indicate that the first quarter is ending on a positive note. The Services PMI fell to 51.7, slightly missing estimates but still sitting comfortably in expansionary territory. Meanwhile, the Manufacturing PMI rose to 52.5, its highest level in nearly two years, blowing past estimates of 51.7. The employment component of the indices was the highest yet in 2024. Perhaps the one drawback is the Prices component, which signaled that inflationary pressures picked up in March. Per the report:

The rate of input cost inflation quickened to a six-month high amid faster increases across both monitored sectors. Service providers indicated that higher operating expenses generally reflected increasing wages, while rising oil and gasoline costs were often mentioned by manufacturers. In turn, companies in the US raised their own selling prices at a faster pace. In fact, the rate of inflation was the sharpest in just under a year and stronger than the series average. Respective rates of output price inflation accelerated sharply across both manufacturing and services, quickening to 13- and eight-month highs as companies passed through higher input costs to their customers.

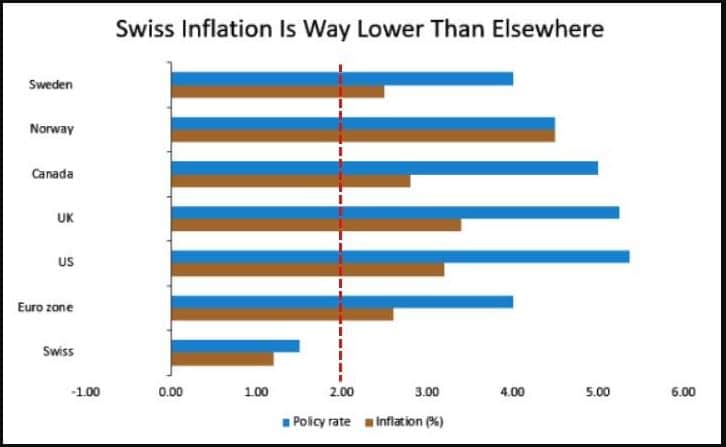

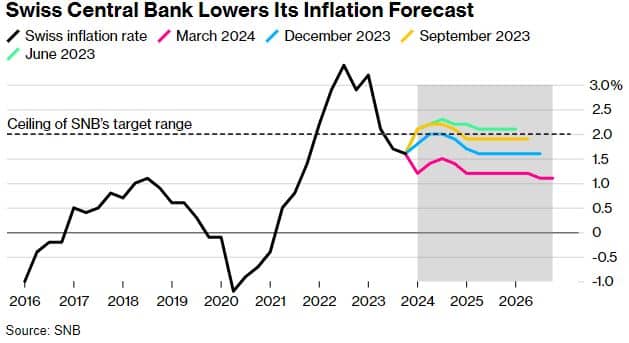

Swiss National Bank Surprises with a Rate Cut

The Swiss National Bank became the first developed market central bank to cut rates in this inflationary cycle. In the decision for the 25bps cut, the Swiss cited the country’s relatively low inflation after an effective fight over the past few years. In fact, the economy is experiencing significantly lower inflation than other developed market economies, as shown in the first chart below, courtesy of Zero Hedge. The action is supported by a significant revision lower to the Swiss National Bank’s inflation forecasts, as shown in the second chart below from Bloomberg. The Swiss Franc fell sharply against the USD and EUR following the news, depreciating 1.2% and 1%, respectively.

While the SNB was the first to cut rates, it doesn’t necessarily mean other developed economies will soon follow suit. The Fed and ECB are the key players to watch, and once they begin cutting rates, a broader trend could emerge. As we wrote yesterday, recent Fed projections assume we will see three rate cuts in 2024. However, a resilient economy and sticky inflation have the potential to derail those expectations. If so, QE Light could be the next trick up the Fed’s sleeve.

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Post Views: 3

2024/03/22