By Lance Roberts | September 30, 2023

Inside This Week’s Bull Bear Report

- Summer Weakness, And October Rallies

- How We Are Trading It

- Research Report – Fed’s Soft Landing Hope Is Optimistic

- Youtube – Before The Bell

- Market Statistics

- Stock Screens

- Portfolio Trades This Week

Market Update & Review

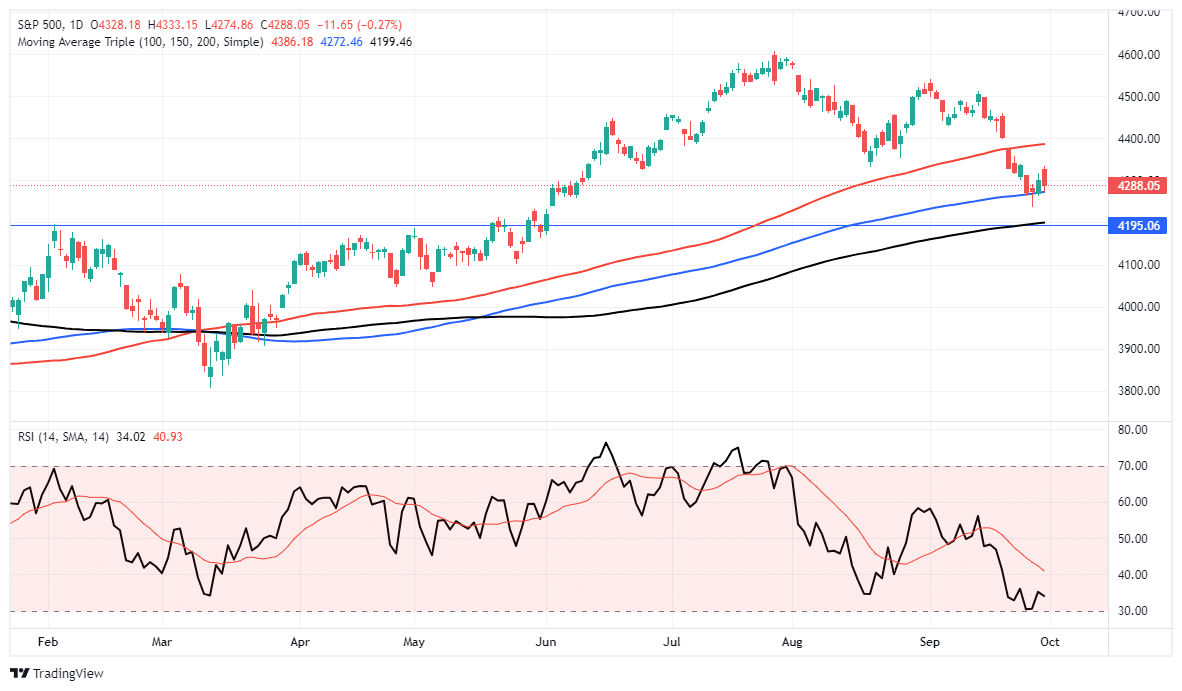

The market took a hit this week once again as the summer weakness continued. While many attributed the decline in stocks and rise in bond yields to the recent Fed projections of “higher for longer,” the action this week seemed more akin to end-of-the-quarter rebalancing for fund managers. Furthermore, September 30th marked the fiscal year-end for about 20% of fund managers who needed to make distributions and redemptions. Nonetheless, the market declined this week, with only minor support holding the market in place.

The market held support at the 150-DMA, which is acting as minor support. A violation of that level will see the markets quickly test the 200-DMA. If this market will maintain its bullish footing, it must hold support and begin to firm up next week.

As we stated last week:

“While there was much handwringing and teeth-gnashing over the decline, it was normal within any given year. As we noted in June: “Notably, in any given year, bullish or bearish, a 5-10% correction is entirely normal and healthy. Such corrective actions are opportunities to increase portfolio equity risk.”

As we will discuss in today’s commentary, the decline was expected and, so far, has remained confined to expectations. Given the reduction in asset prices, a drop in bullish sentiment, and technically oversold conditions, the summer weakness has set the markets up for a potential year-end rally.

Need Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

Summer Weakness As Expected

As noted above, September lived up to its history of summer weakness, one of the weaker months of the year.

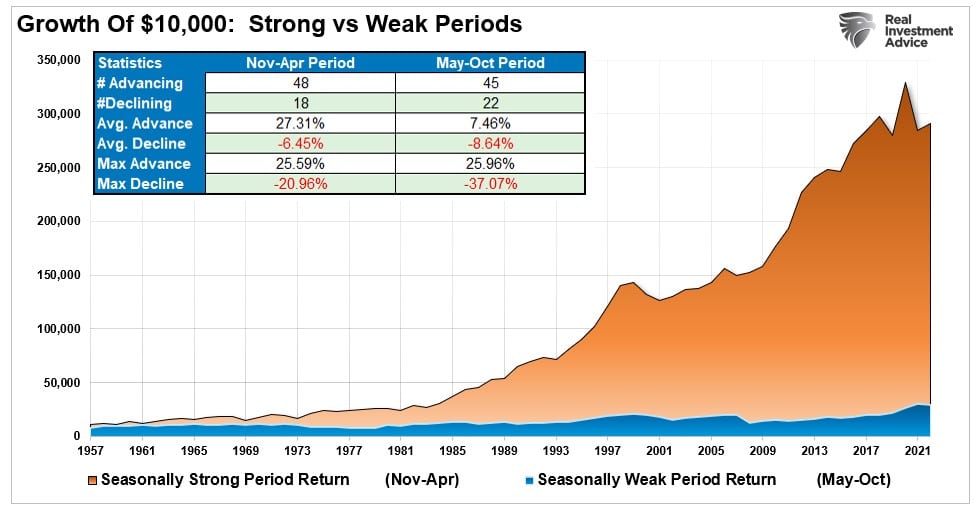

“Just as a reminder, the historical analysis suggests summer months of the market tend to be the weakest of the year. The mathematical statistics prove this as $10,000 invested in the market from November to April vastly outperformed the same amount invested from May through October. Interestingly, the max drawdowns are significantly larger during the ‘Sell In May’ periods. Previous important dates of major market declines occurred in October 1929, 1987, and 2008.”

So far this year, the summer weakness from May through September remains average, with a return of just 2.5%. However, once we remove the weighting bias of the “Top-7” mega-capitalization stocks from the calculation, the equal-weighted S&P index is down nearly 3% over the same period. Given that most portfolios own more than just seven stocks, the performance of most portfolios, mainly if they are diversified in any manner, is likely closer to zero than not.

As stated above, the summer weakness was mostly as expected. In “Bull Trap Or Bear Market,” we noted that a 5-10% correction should be expected. To wit:

“If we assume a correction started from the market high on June 14th, 2023, the retracement sequence provides mathematical levels of potential support during a retracement. A roughly 5% correction would reach the initial 23.6% retracement. At that level, it will likely intersect with the 50-day moving average. The next level of a corrective process would require a 7% decline to the 38.2% retracement and a nearly 10% decline to the 50% retracement to the 200-day moving average.

Notably, in any given year, bullish or bearish, a 5-10% correction is entirely normal and healthy. Such corrective actions are opportunities to increase portfolio equity risk.”

We were a bit early as the high for the market came in July. However, while the retracement levels differ, the correction has fallen within that historical range.

The good news is that the summer weakness sets the markets up for a more substantial year-end rally.

October Rallies Follow Summer Weakness

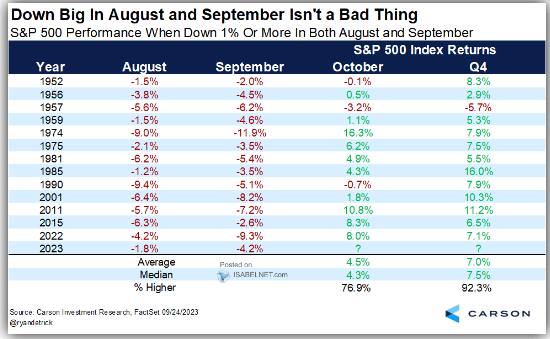

As shown in the table below, There were three occasions where October continued to sport weak market returns following a negative return in the previous two months. However, there was only one occasion following summer weakness in August and September, where the fourth quarter also yielded a negative return.

On average, when summer weakness prevailed in August and September, October tended to be higher by 4.5%, with the fourth quarter averaging a 7% return.

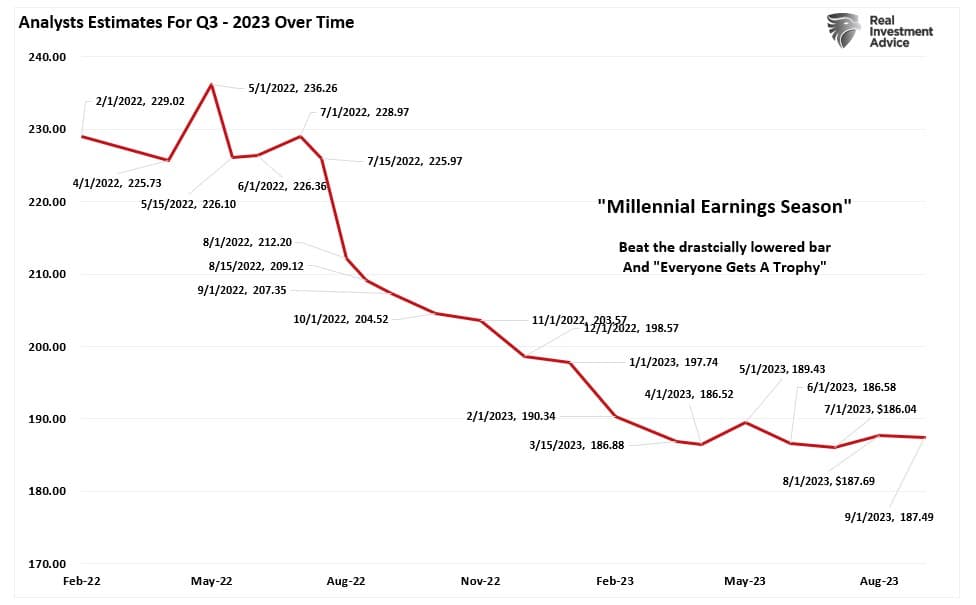

While there is much concern about the Federal Reserve hiking rates, potentially weaker economic growth, and inflationary pressures, there is no sign of a recession yet. Those immediate concerns will likely fade as October gets underway, which will kick off the Q3 earnings season. Since analysts have lowered the bar quite dramatically for the third quarter, the market should have a reasonably high “beat rate” of earnings to rally off of.

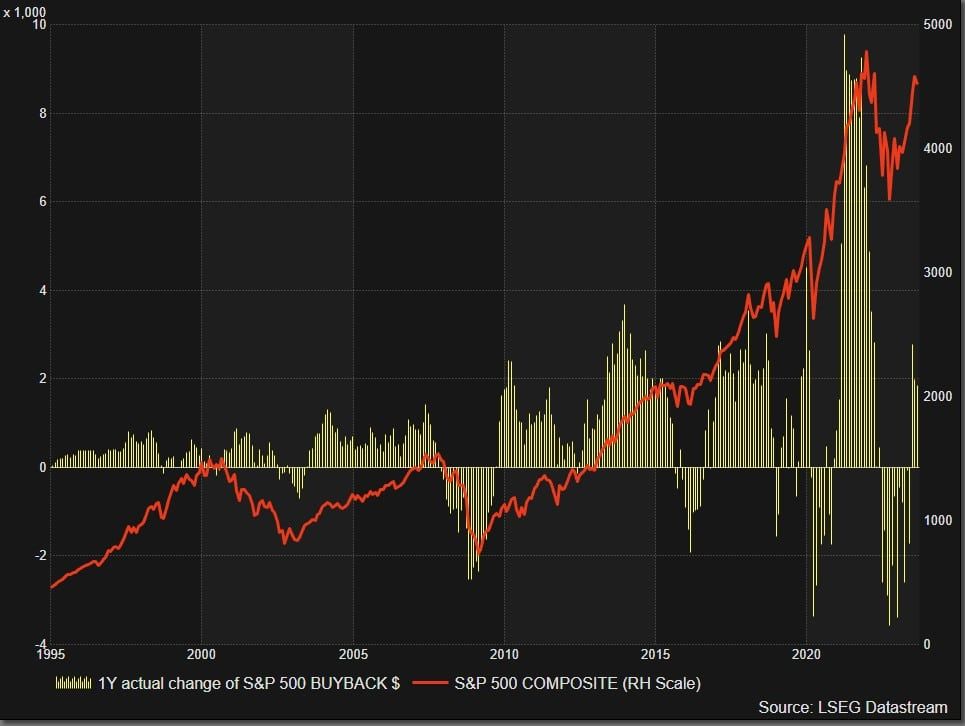

Then, just as earnings season winds down, the “blackout period” for corporate share buybacks will end. As noted by Goldman Sachs, there could be as much as $5 billion a day in repurchases through the end of the year. Historically, those buybacks have provided a solid tailwind for stock prices, particularly in the large-capitalization companies that execute the most significant transactions.

Lastly, as we head into year-end, the summer weakness provided much-needed relief to the exuberant bull market run from the beginning of the year. The previously overly optimistic, over-bought, and over-allocated measures of the market have been essentially reversed. From a contrarian point of view, this is precisely the kind of technical backdrop that provides the “buying power” to the markets in the short term.

The Technical Setup For A Year-End Rally

As a contrarian investor, excesses get built when everyone is on the same side of the trade.

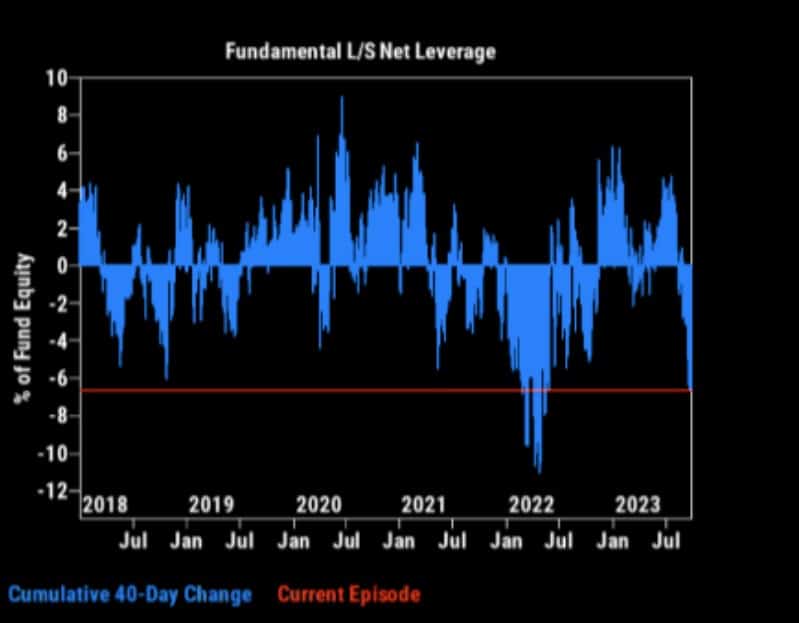

With that said, everyone is so bearish the markets could respond in a manner no one expects. As shown below, portfolio managers are extremely short on equities.

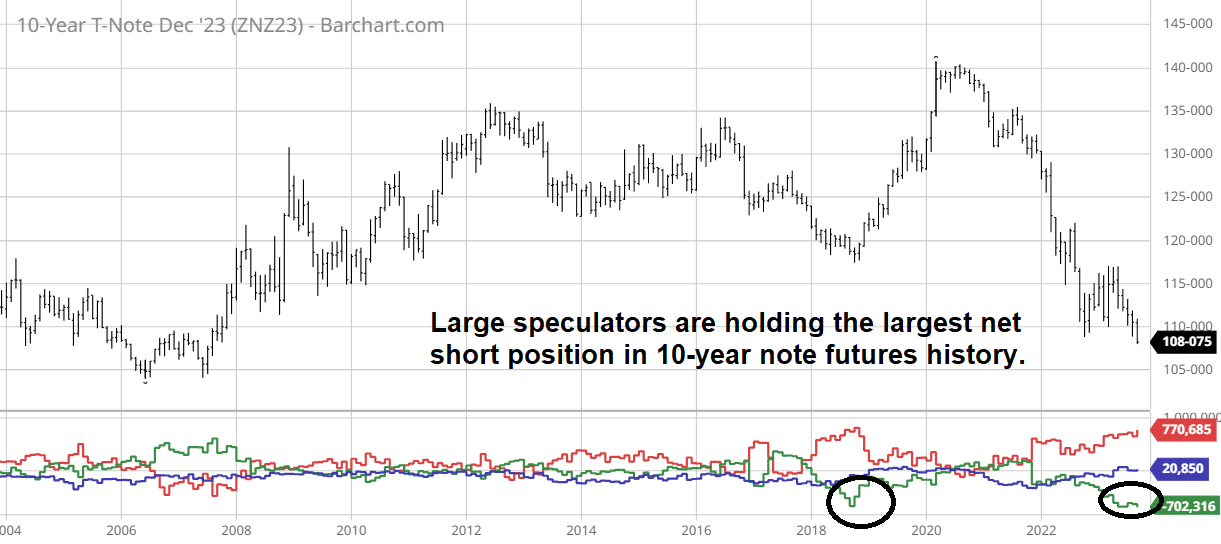

Furthermore, speculators are also at a record net short on Treasury debt.

While many believe this time is different, it is unlikely that such is the case.

“The odds favor an eventual unwind of the overly bearish 10-year note trade. The massive amount of short-covering could easily push yields back into the 2% handle.” – Carley Garner, Real Money

However, it isn’t just the leveraged backdrop of record short equity and bond exposures. That is just the eventual “fuel” for the rally when it begins. There is currently very negative sentiment and technical support, which suggest that a reflexive rally could begin sooner rather than later.

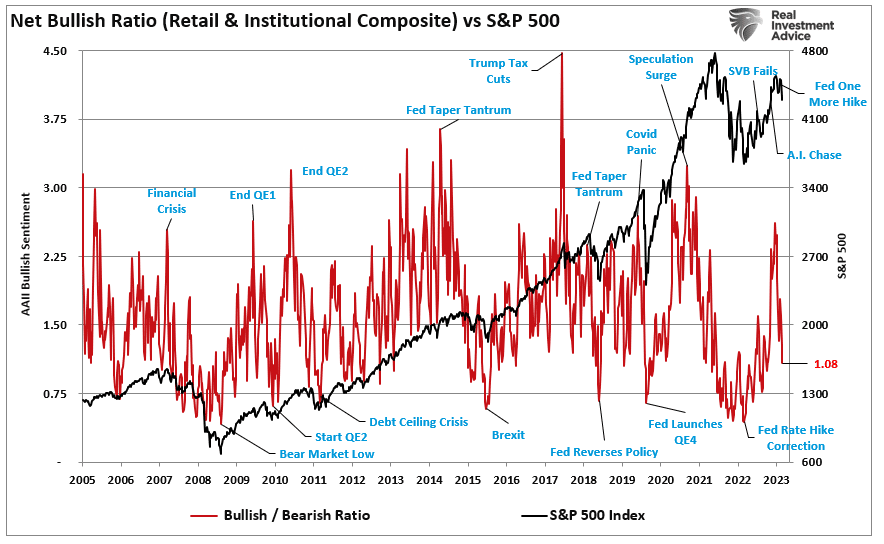

The chart below shows the relatively sharp decline from the more exuberant bullish sentiment we saw in June and July. Historically, when the combined readings of retail and professional sentiment reached current levels, such formed the basis for a reflexive rally.

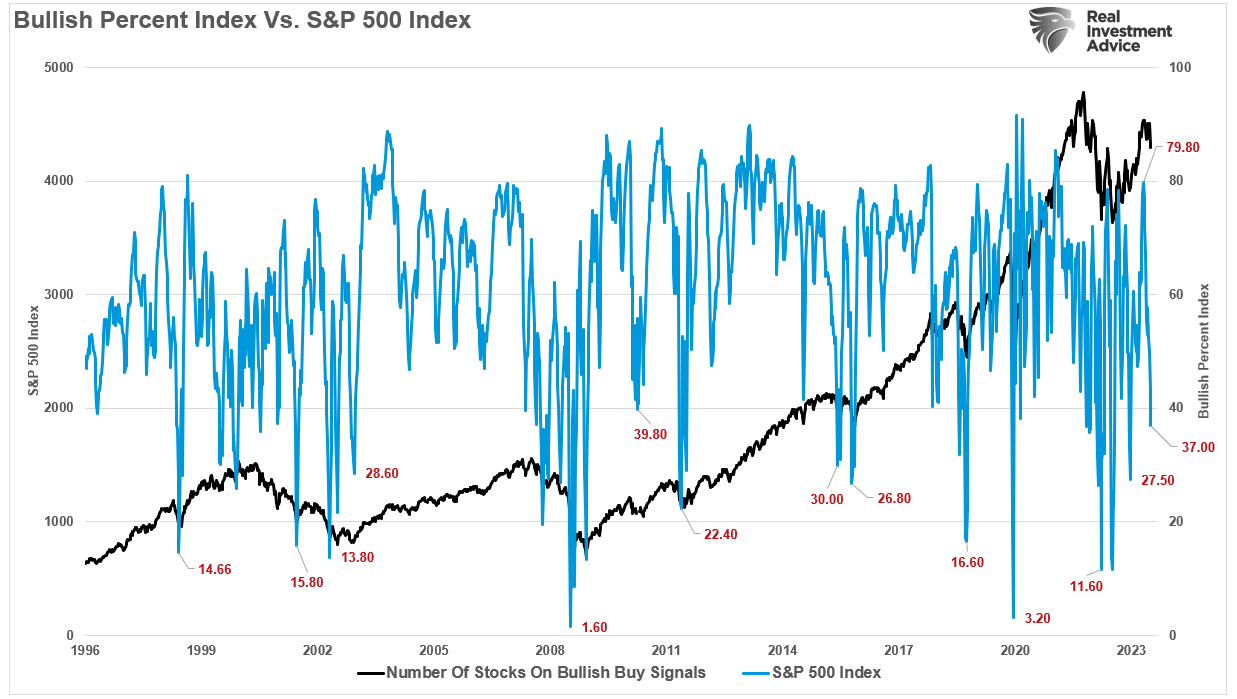

The same holds for the number of stocks on “bullish buy signals.” During more bullish markets, readings below 40 have coincided with near-term market bottoms.

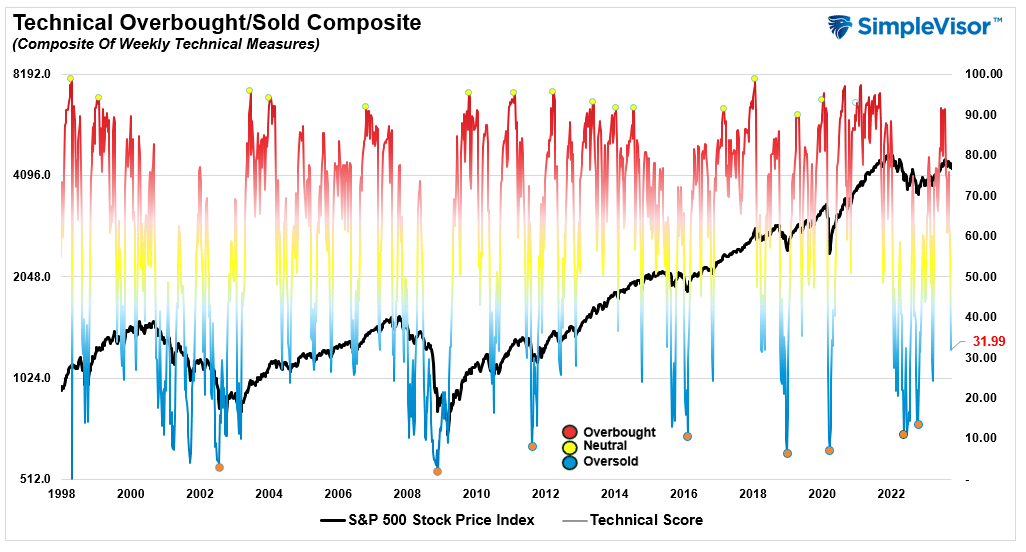

Furthermore, our technical gauge, comprised of weekly readings of the Williams %R, RSI, MACD, and other measures, is reaching more deeply oversold levels. Again, when combined with a high level of leverage and negative sentiment, such is usually the point where markets do the opposite of what everyone expects.

At the moment, it is clear that interest rates are driving the ship. However, that ship is likely on the cusp of making a significant turn. While we could see a short-term rally in equities along with bonds at the end of the year, we suspect that next year maybe when bonds drastically outperform equities.

But such is what you would expect with the onset of a recession.

Being A Contrarian

As we have often discussed, one of the investors’ most significant challenges is going “against” the prevailing market “herd bias.” However, historically speaking, contrarian investing often proves to provide an advantage. One of the most famous contrarian investors is Howard Marks, who once stated:

“Resisting – and thereby achieving success as a contrarian – isn’t easy. Things combine to make it difficult; including natural herd tendencies and the pain imposed by being out of step, particularly when momentum invariably makes pro-cyclical actions look correct for a while.

Given the uncertain nature of the future, and thus the difficulty of being confident your position is the right one – especially as price moves against you – it’s challenging to be a lonely contrarian.”

However, if the most fundamental premise of investing is to “buy when everyone is fearful,” investors may again be missing the contrarian opportunity.

As Bob Farrell’s Rule Number-9 states:

“When all the experts and forecasts agree – something else is going to happen.

So, what do you think most likely happens after the summer weakness?

How We Are Trading It

There are plenty of reasons to be very concerned about the market over the next few months. Given the market leads the economy, we must respect the market’s action today for potentially what it is telling us about tomorrow. Therefore, there are some actions we can take to navigate whatever path the market chooses.

- Move slowly. There is no rush to make dramatic changes. Doing anything in a moment of “panic” tends to be the wrong thing.

- If you are overweight equities, DO NOT try to fully adjust your portfolio to your target allocation in one move. Again, after significant declines, individuals feel like they “must” do something. Think logically about where you want to be and use the rally to adjust to that level.

- Begin by selling laggards and losers. These positions were dragging on performance as the market rose, and they led on the way down.

- Add to sectors or positions performing with or outperforming the broader market if you need risk exposure.

- Move “stop-loss” levels up to recent lows for each position. Managing a portfolio without “stop-loss” levels is like driving with your eyes closed.

- Be prepared to sell into the rally and reduce overall portfolio risk. You will sell many positions at a loss simply because you overpaid for them. Selling at a loss DOES NOT make you a loser. It just means you made a mistake.

- If none of this makes sense, please consider hiring someone to manage your portfolio. It will be worth the additional expense over the long term.

Just remember:

“In good times, skepticism means recognizing the things that are too good to be true; that’s something everyone knows. But in bad times, it requires sensing when things are too bad to be true. People have a hard time doing that.

The things that terrify other people will probably terrify you too, but to be successful, an investor has to be a stalwart. After all, most of the time the world doesn’t end, and if you invest when everyone else thinks it will, you’re apt to get some bargains.“ – Howard Marks

Follow your process.

This past week, I took advantage of the jump in interest rates to add to my long position in TLT. It is now my largest holding by far heading into year-end. My colleague, Michael Lebowitz, CFA, also similarly added to his long-call options on TLT. Our conviction to our view on bonds has a long window of 18-36 months. But the economics don’t support rates at current levels for long.

See you next week.

Research Report

Subscribe To “Before The Bell” For Daily Trading Updates

We have set up a separate channel JUST for our short daily market updates. Please subscribe to THIS CHANNEL to receive daily notifications before the market opens.

Click Here And Then Click The SUBSCRIBE Button

Subscribe To Our YouTube Channel To Get Notified Of All Our Videos

Bull Bear Report Market Statistics & Screens

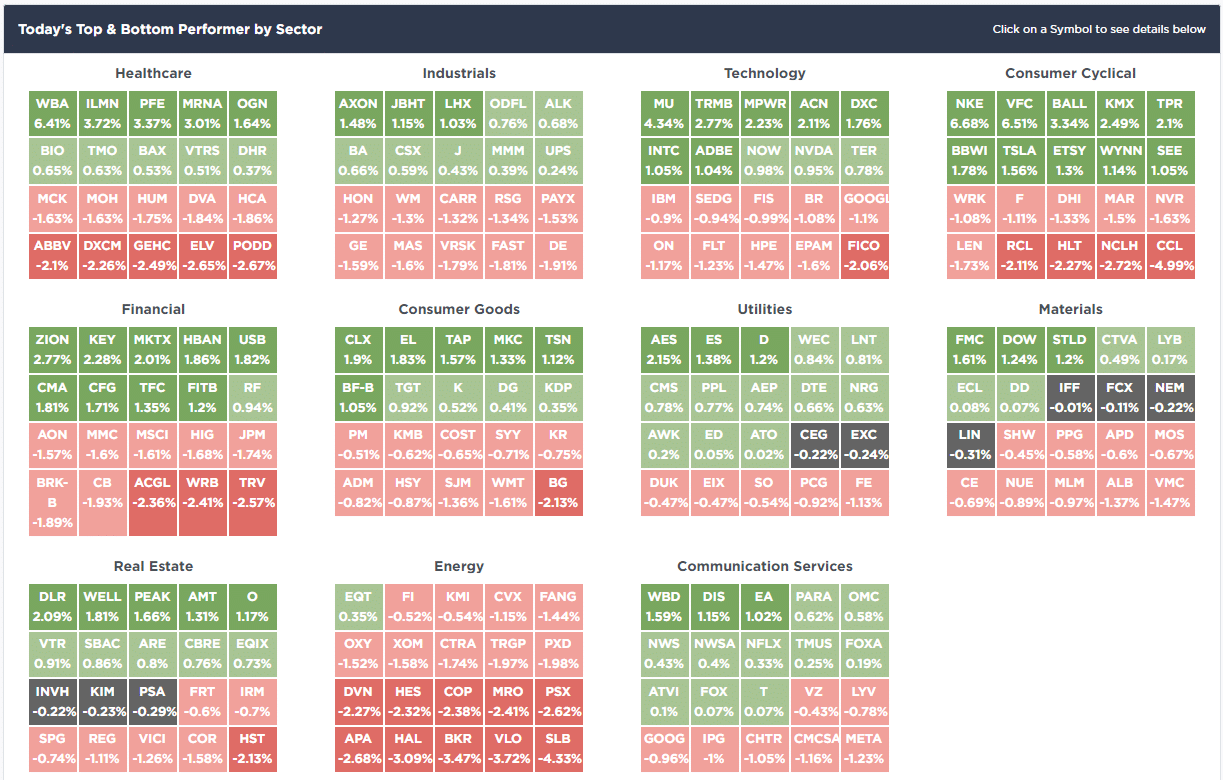

SimpleVisor Top & Bottom Performers By Sector

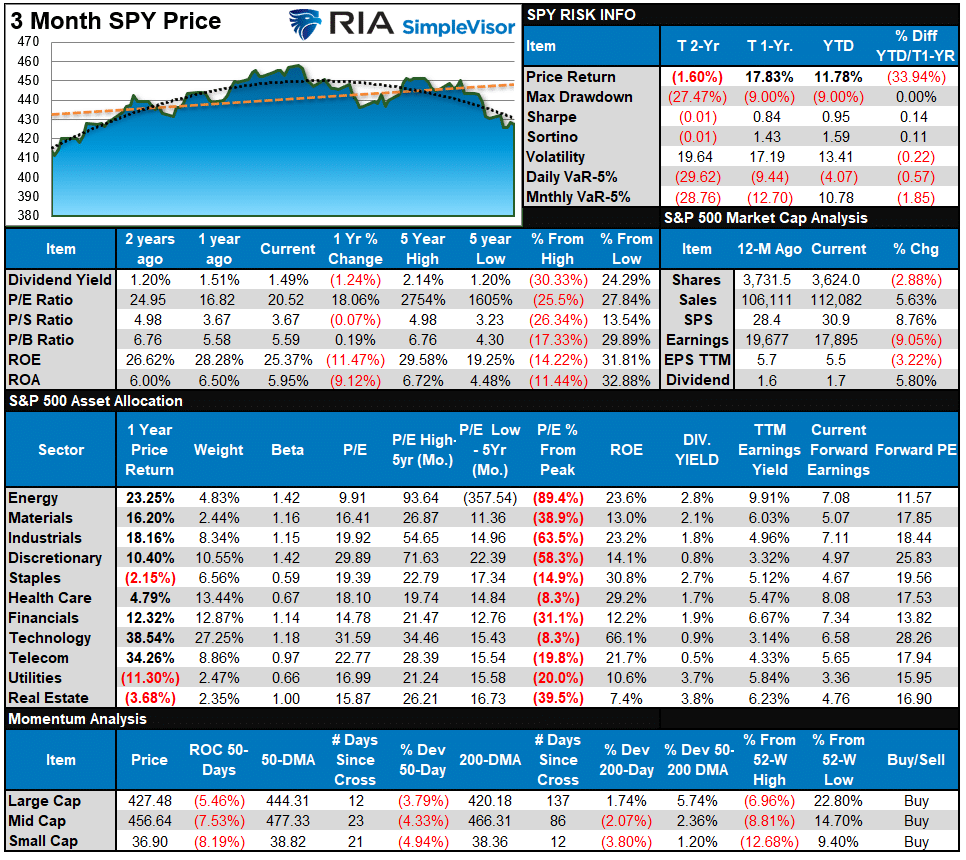

S&P 500 Weekly Tear Sheet

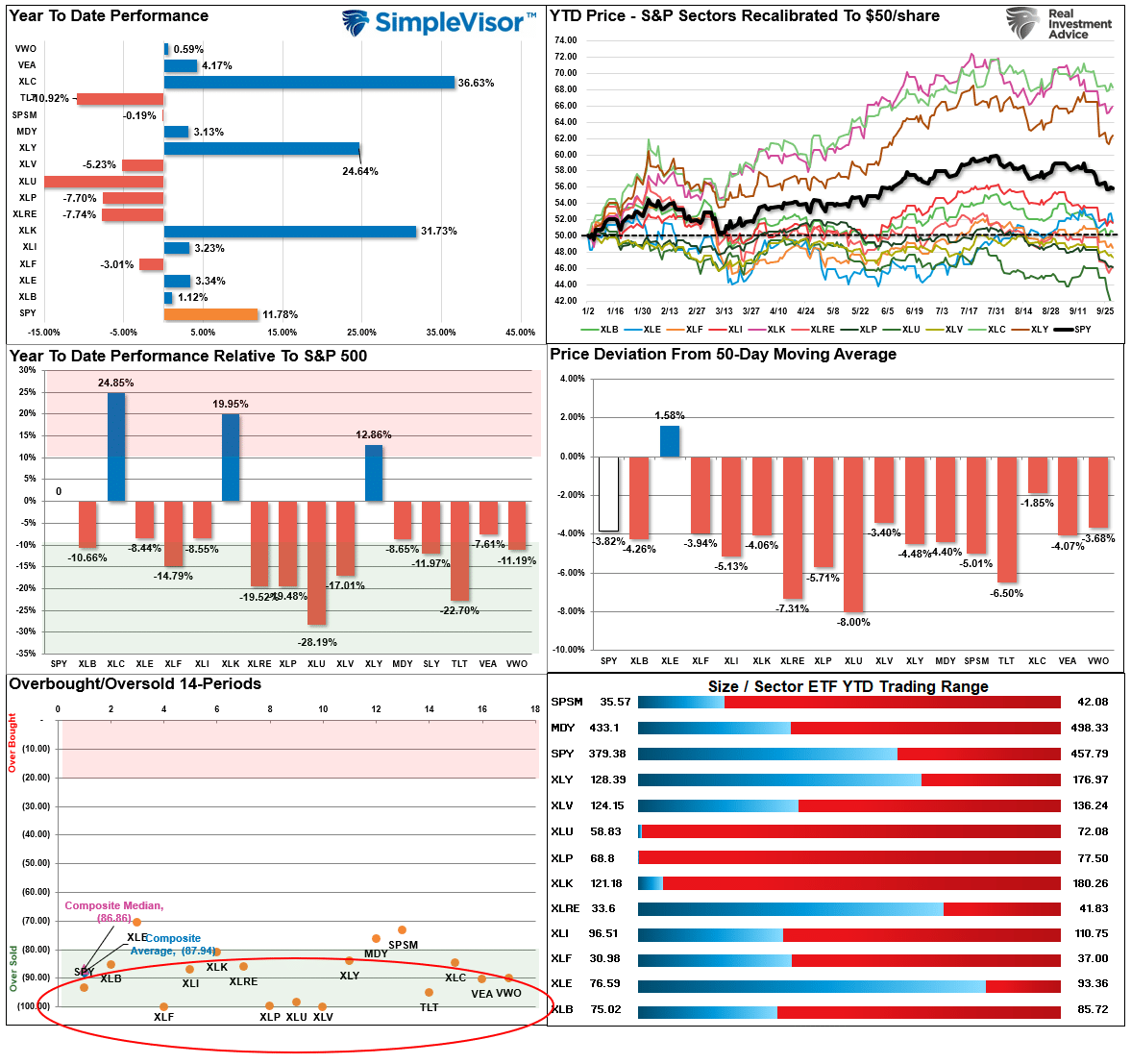

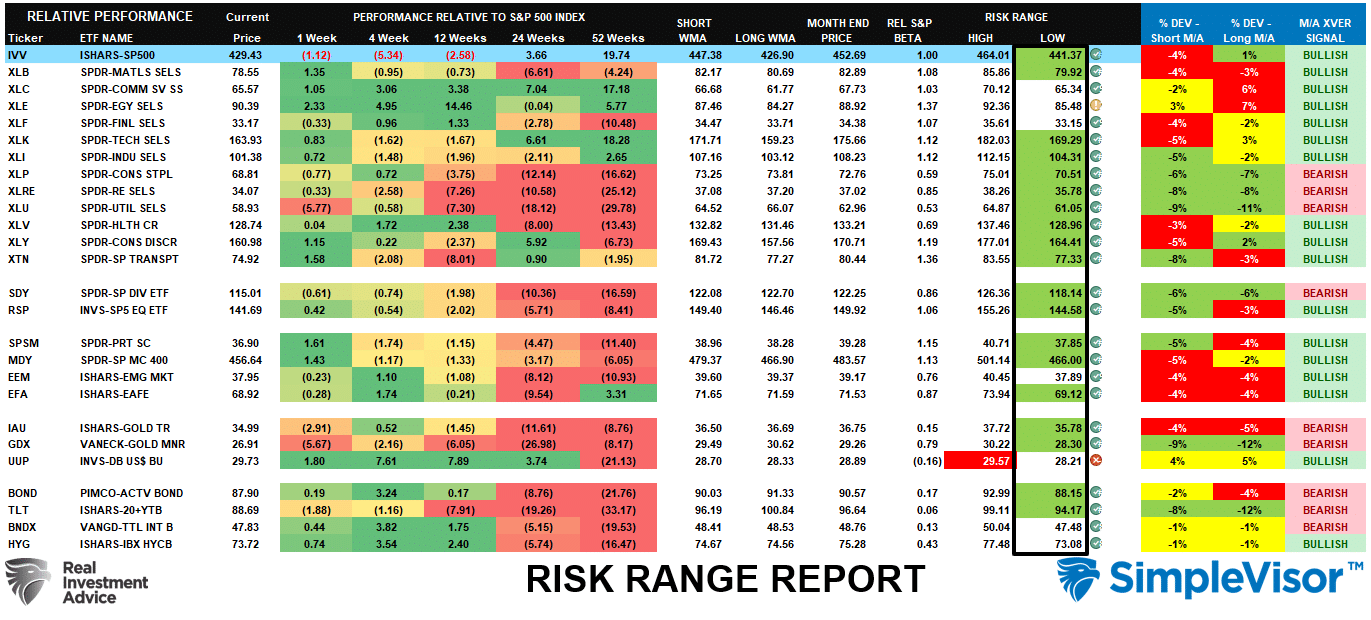

Relative Performance Analysis

Last week, we noted that most markets and sectors were oversold after the sell-off.

“Furthermore, the deviations of many of those markets and sectors below the 50-DMA suggest a decent counter-trend rally is likely starting this week. While we are likely not clear of the seasonally weak period as of yet, the downside from current levels is likely very limited. Look to use current weaknesses to add exposure to portfolios accordingly.”

The rally did not manifest this week, but a counter-trend bounce is highly likely with most markets and sectors in oversold territory and the beginning of the new quarter ahead. This analysis is confirmed by the risk/reward ranges shown below.

Technical Composite

The technical overbought/sold gauge comprises several price indicators (R.S.I., Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. The market peaks when those readings are 80 or above, suggesting prudent profit-taking and risk management. The best buying opportunities exist when those readings are 20 or below.

The current reading is 31.99 out of a possible 100.

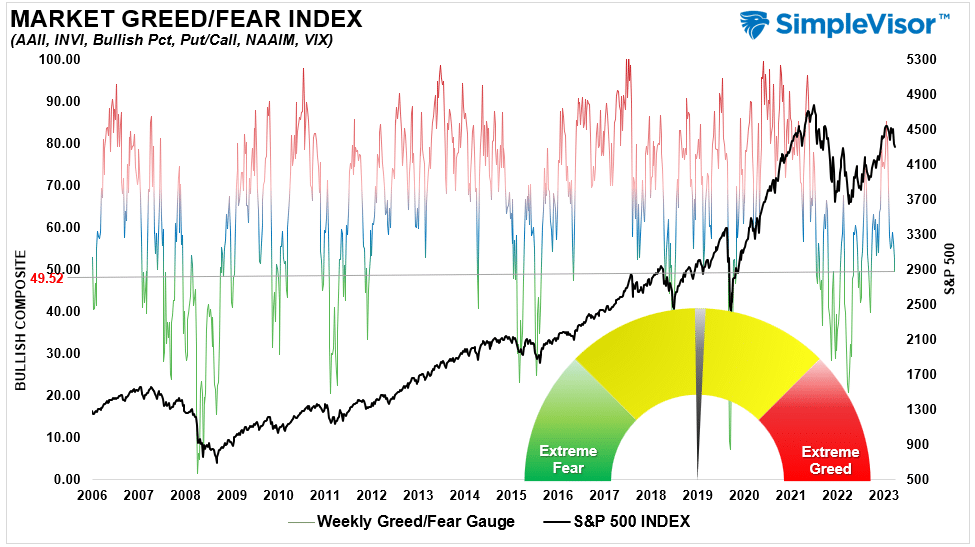

Portfolio Positioning “Fear / Greed” Gauge

The “Fear/Greed” gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, the more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0 to 100. It is a rarity that it reaches levels above 90. The current reading is 49.52 out of a possible 100.

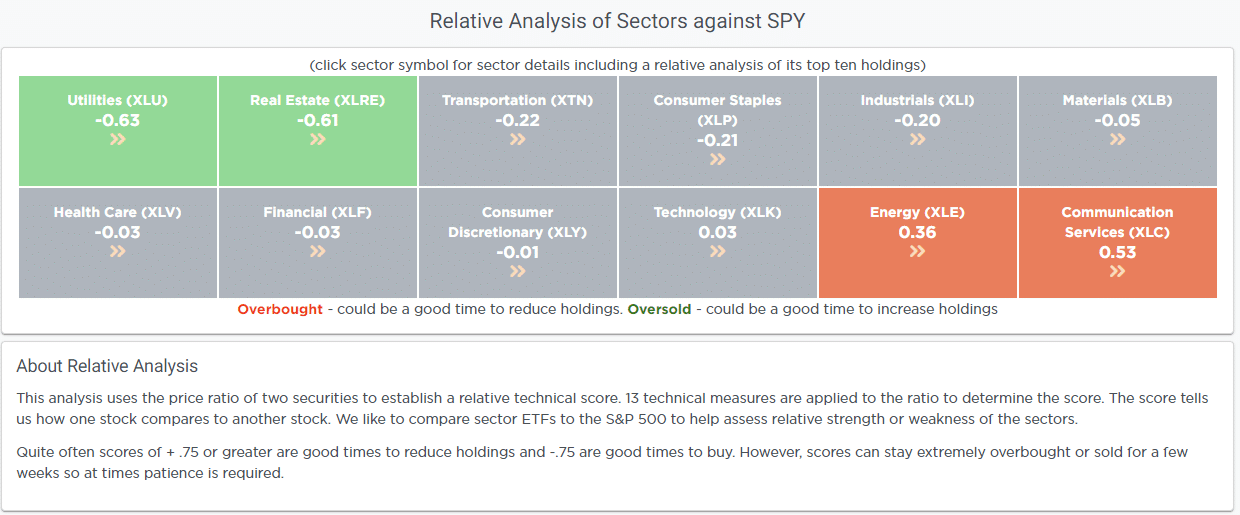

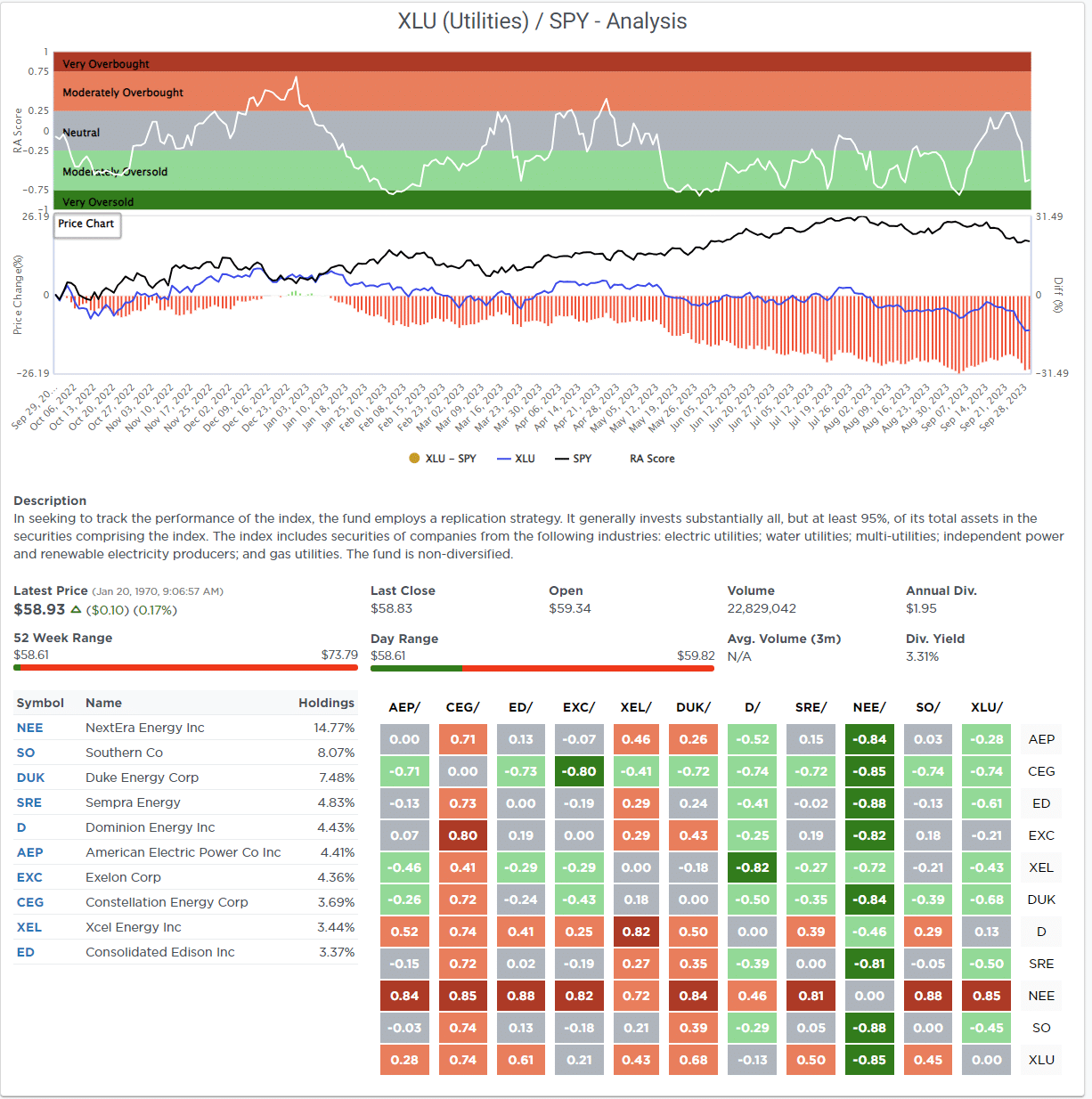

Relative Sector Analysis

Most Oversold Sector Analysis

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares the relative performance of each sector and market to the S&P 500 index.

- “MA XVER” (Moving Average Crossover) is determined by the short-term weekly moving average crossing positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- The table shows the price deviation above and below the weekly moving averages.

The sell-off this past week pushed many sectors and markets well below their normal monthly trading ranges. These more oversold conditions will likely precede a reflexive rally starting this week. In particular, Technology, Real Estate, Staples, Industrials, Materials, Utilities, Healthcare, Discretionary, and Transports are the highlighted sectors for leadership. Small and Mid-capitalization stocks and Bonds are the major markets to watch for a rally.

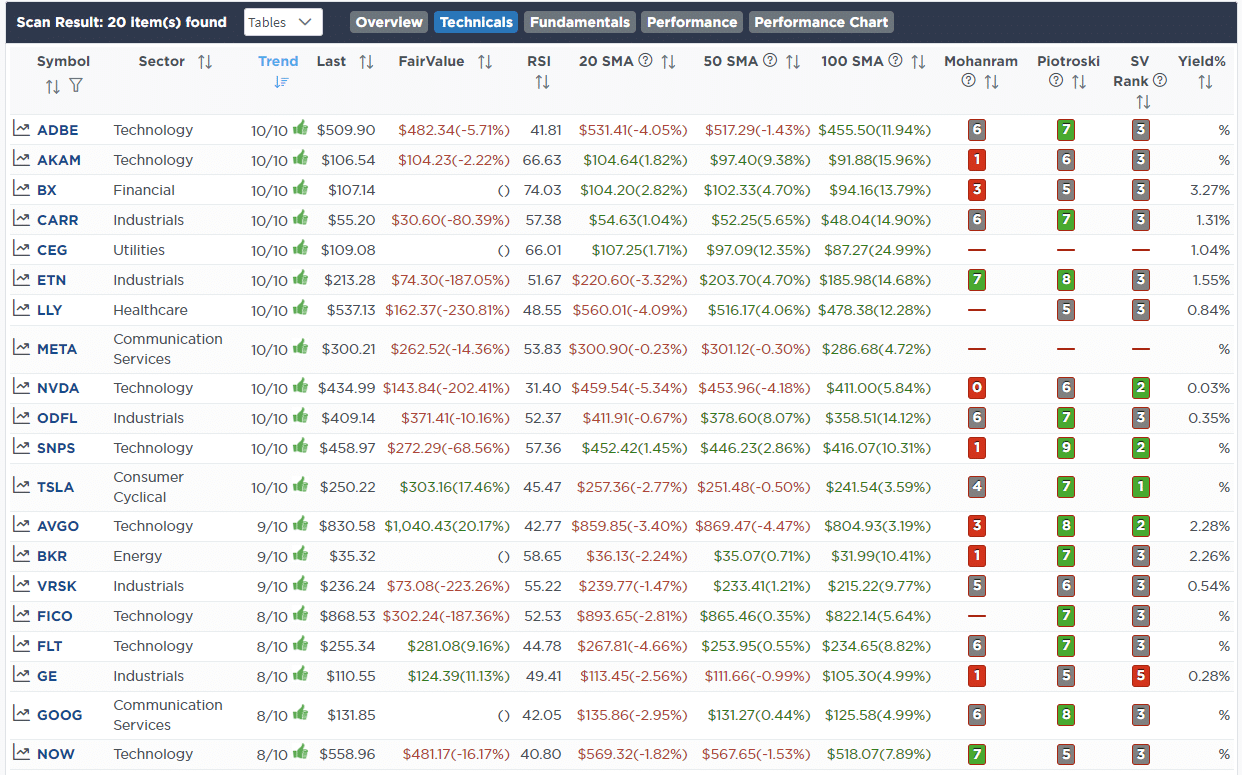

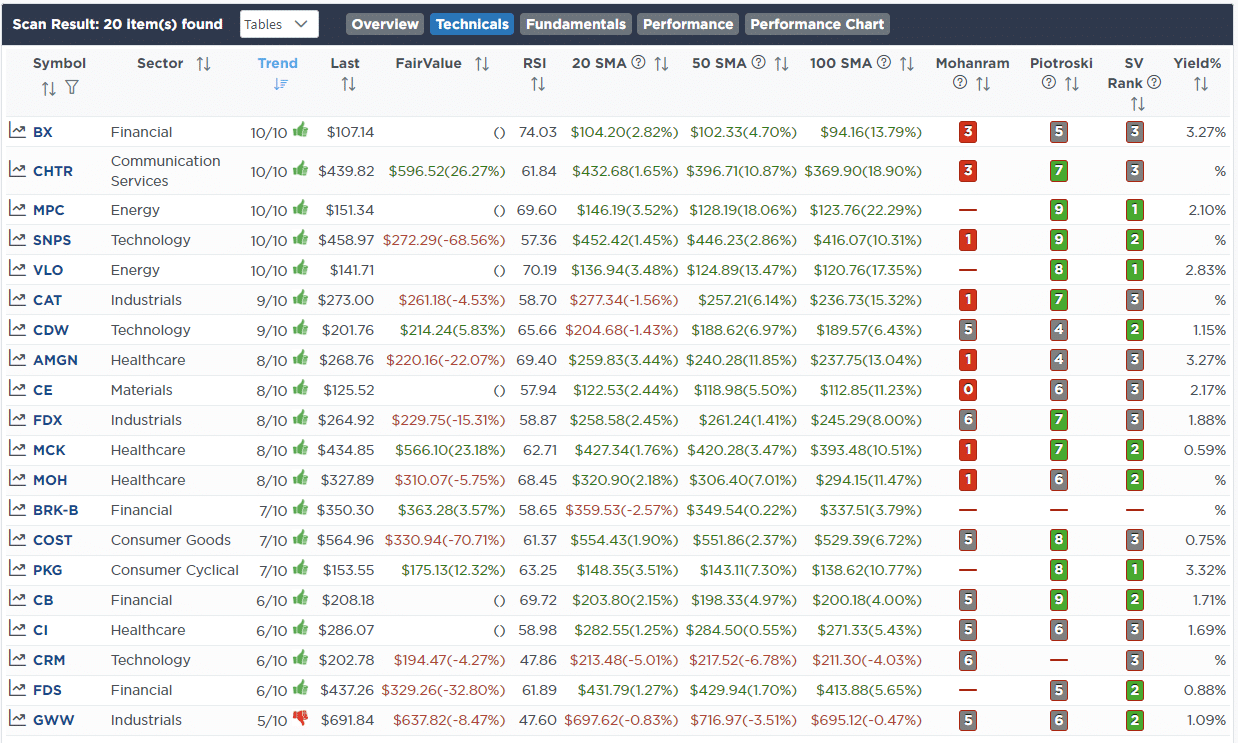

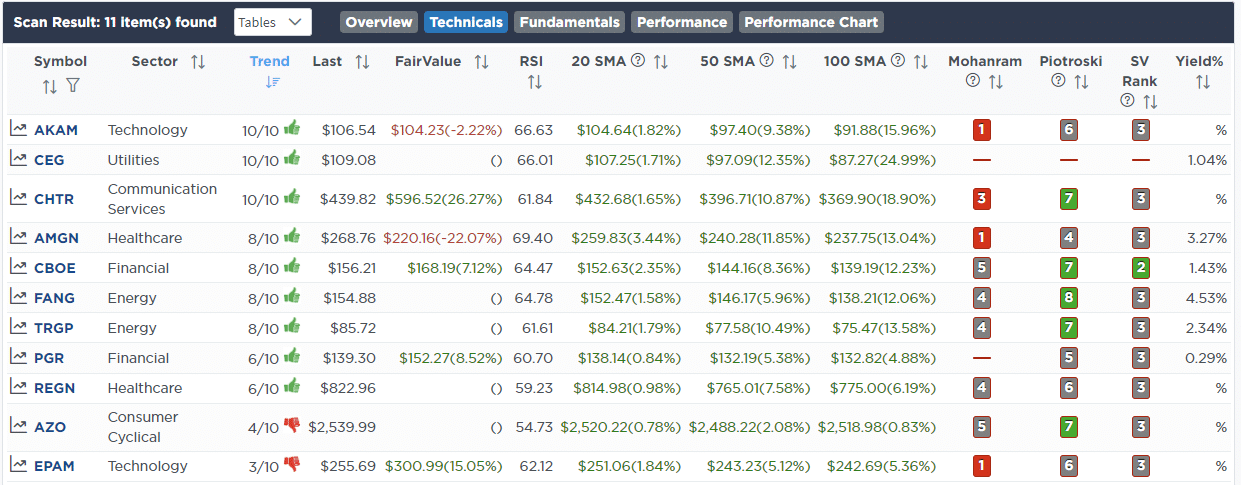

Weekly SimpleVisor Stock Screens

We provide three stock screens each week from SimpleVisor.

This week, we are searching for the Top 20:

- Relative Strength Stocks

- Momentum Stocks

- Fundamental & Technical Strength

(Click Images To Enlarge)

R.S.I. Screen

Momentum Screen

Fundamental & Technical Strength

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

No Trades This Week

Lance Roberts, C.I.O.

Have a great week!

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)