This week, Jack Manley, Global Market Strategist at J.P. Morgan Asset Management put forth the argument that shelter costs are a main component of inflation and that, by lowering rates, more supply will come to market, causing home prices to decline. “You’re not going to see meaningful downward pressure on shelter costs until the Fed lowers interest rates, mortgages come down to a more reasonable level, and supply comes back online because people are willing to step into that market,” Manley said.

Manley is not alone. Oppenheimer’s John Stoltzfus hinted last week at the idea that lower mortgage rates would prompt more people to sell their homes, leading to more supply and potentially softer prices. If people could afford to buy homes, they wouldn’t need to rent as much, and rents could stabilize.

If I can summarize, the argument must be that lower rates will allow current owners to sell their homes, move, and buy other homes because lower rates make new homes more affordable. More supply will depress home prices, which, in turn will force rents lower. Lower home prices and lower rents will mean lower inflation.

Unfortunately, Manley’s argument is like a Twinkie, delicious but with no redeeming nutritional value.

Manley is correct to focus on shelter costs. In the 3/14/24 World Snapshot entitled Why the FED cannot lower rates yet., TPA explained that shelter (home prices and rents) accounts for about one third of the CPI basket. So, no matter what other parts of CPI do, shelter is the gorilla in the room.

The argument that lower rates will create more housing supply, however, ignores two main features of the housing market:

- Homes are unlike most other things that people buy and sell. You need a home as a place to live. When most people sell a home, they need to buy a home. If everyone who sells a home buys a home, the net addition to supply is zero. The only way a sale could add to the housing supply is if the home sold was not the primary residence. Unfortunately for Mr. Manley’s argument, according to NAHB estimates, the total count of second homes accounted for 5.11% of the total housing stock in 2020.

- The second feature of TODAY’s housing market makes Manley’s argument not only wrong but very risky. There is a huge deficit of homes in the U.S. Simply put; there are far more buyers of homes than inventory of homes. That is the reason for the meteoric rise in home prices in the past 4 years. The only reason more people are not buyers right now is a historic rise in rates. Lowering the costs of buying a home will only bring these buyers into the market; increasing demand and home prices.

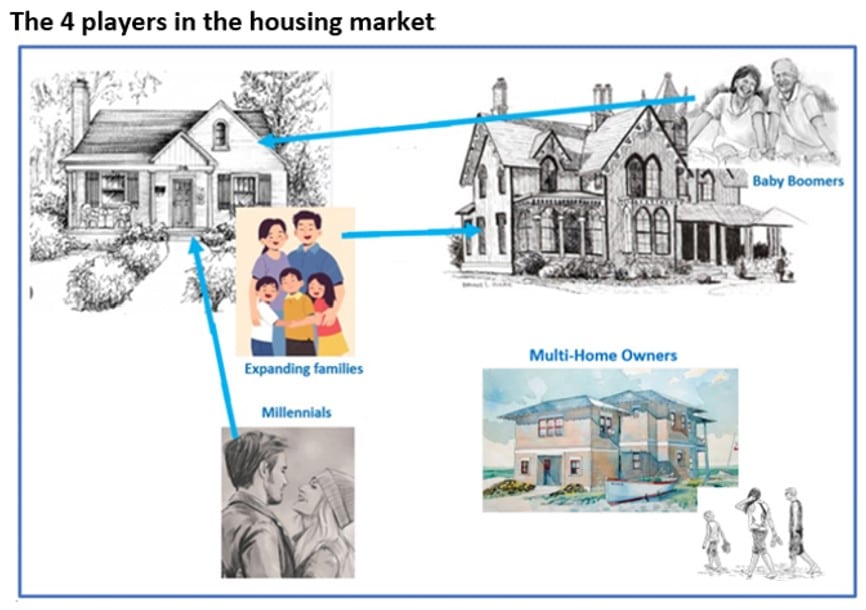

In the 11/15/23 World Snapshot, Lower Rates Will Increase Home Sales and Home Prices, TPA discussed the current market, dynamics that exist in the housing market. I explained that any interest rate decline would occur in an environment of low housing supply, full employment, a stubbornly robust economy, and continued demand for homes. I divided the players in the market into 4 categories to determine their effect on the overall market:

- Downsizers

- Upgraders

- First time home buyers

- Second home owners

Spoiler: if you consider all the parties, the effect of lower rates will be more home transactions AND higher prices.

In order to look at the possible Inventory, Sales, and Price effects on the housing market, it is helpful to consider how different players in the market would be affected by a decrease in rates. In the table below, we have divided the players in the housing market into 4 types:

- Downsizers – people who would like to sell their larger homes and buy a smaller home to lower their monthly housing costs. These people have held off selling at higher prices, because a smaller home would not save them much money due to increased mortgage rates. Now, with financing becoming more attractive, they may consider a sale.

EFFECT – since they are both buying and selling, the effect should be neutral.

- Upgraders – people who want or need a larger home for their family. These people have held off buying because higher rates made it prohibitive or because there was no supply.

EFFECT – since they are both buying and selling, the effect should be neutral.

- First-time buyers –mostly people in their 20s and 30s have been kept out of the market because of high prices, lack of supply, and, most recently, rates that made buying prohibitively expensive.

EFFECT – lower rates will entice some of these people to act. The act will mean buying and more demand.

- Second homeowners – these people have 2 or more homes. They are usually wealthier and less likely to use a mortgage.

EFFECT –although these people may be tempted to sell at high prices and lower rates may make it easier for some people to buy from them, it is hard to determine if there would be any net effect.

Manley’s argument for lower rates leading to lower prices rests on the idea that supply will outweigh demand. The nature of home ownership and the current supply/demand situation flattens Manley’s Twinkie.

Jeff Marcus founded Turning Point Analytics (TPA) in 2009 after 25 years on trading desks and 13 years as a head trader to provide strategic and technical research to institutional clients. Turning Point Analytics (TPA) provides a unique strategy that works as an overlay to clients’ good fundamental analysis. After 10 years of serving only large institutions, TPA now offers its research services to mid and small managers, RIA’s, and wealthy sophisticated individuals looking for a way to increase their returns and outperform their peers.

Subscribe 2 Week Trial

Customer Relationship Summary (Form CRS)