In Part One, we made the following comment about PG:

Its price-to-sales ratio is also elevated versus pre-pandemic levels. The stock is expensive, but continued share buybacks partially justify the valuations.

A reader asked if we would elaborate on how buybacks justify high valuations, especially in the case of PG. We oblige, but before explaining, we recommend reading our recent article on the same topic – Apple’s Magic.

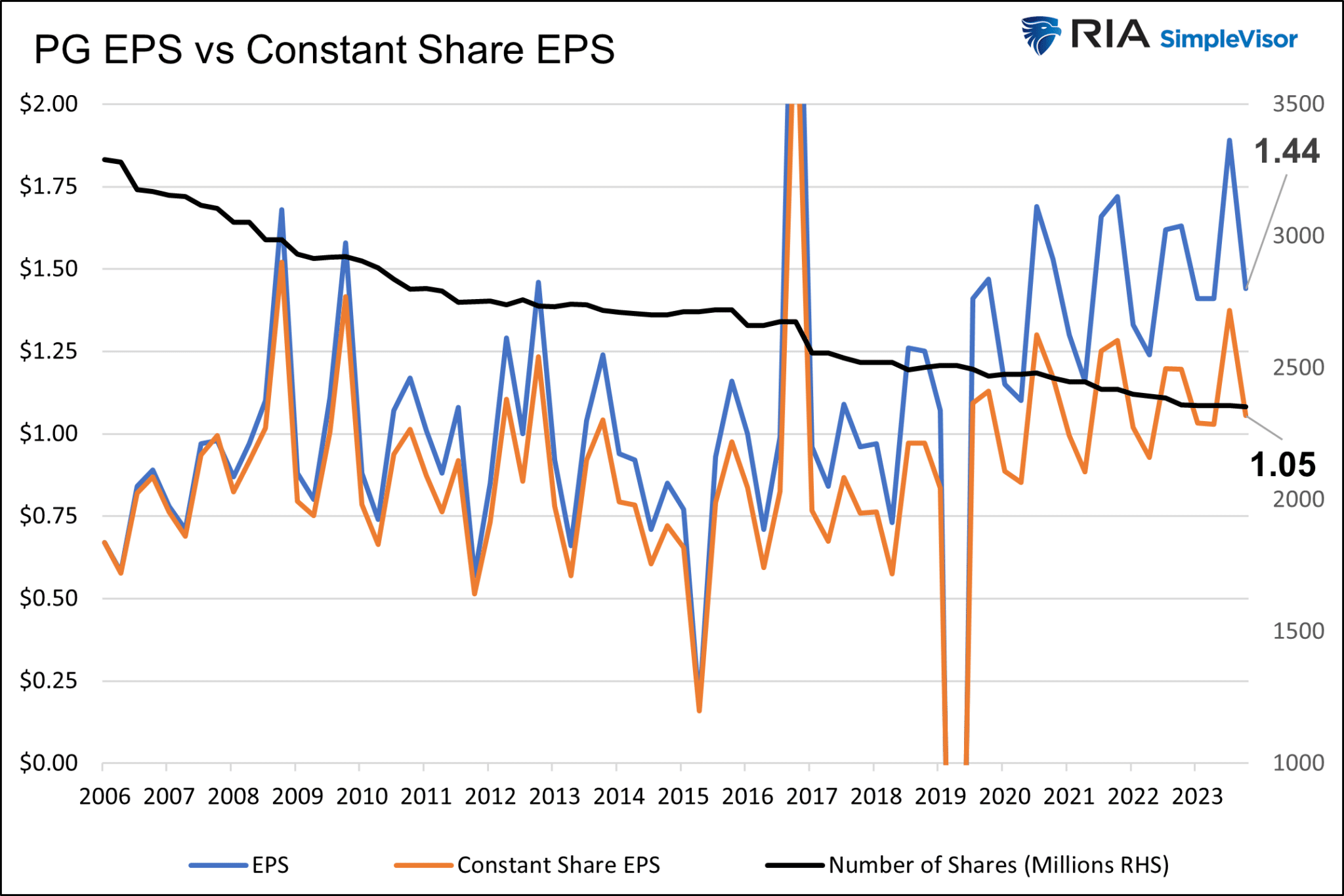

PG Earnings Growth Versus The Market

The following analysis starts in 2006 when the number of PG shares began to shrink.

Since 2006, PG has increased its earnings by 7.90% annually and earnings per share by 13.80% annually. The stark difference is solely a function of buybacks. In the graph below, the black line shows the number of PG shares has declined by 5.50% on an annualized basis.

As a comparison, annualized operating earnings for the S&P 500 have grown by 15.66% and its operating earnings per share by 17.04%. There is also a gap between earnings and EPS, but it’s not nearly as large. This is likely because many companies do not buy back shares and some issue shares.

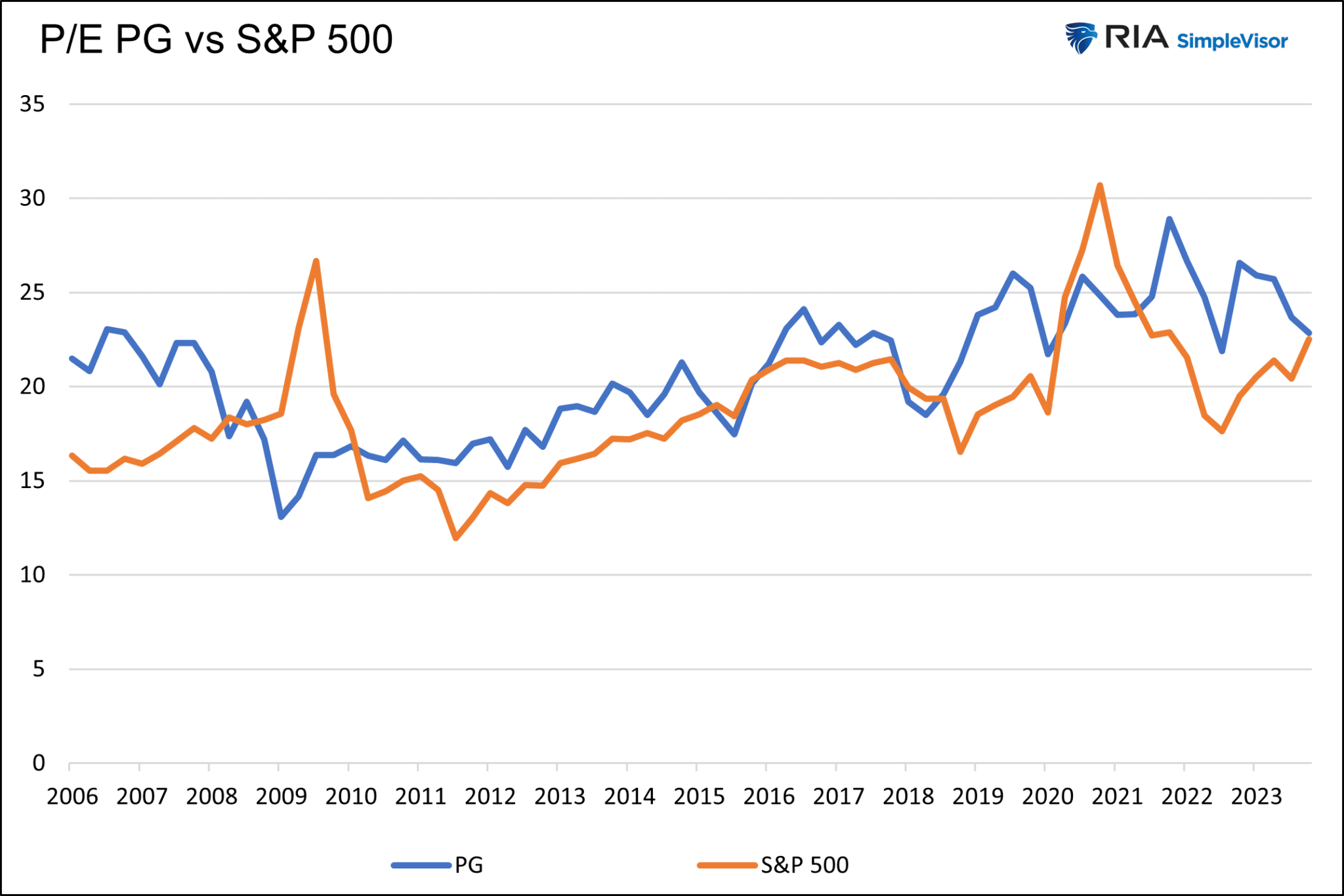

The following graph shows that the P/E valuation for PG and the S&P 500 tend to oscillate around each other.

Based solely on this analysis, PG must continue to buy back its shares to keep its earnings per share in line with the S&P 500 and thus justify a similar valuation. Remember that PG pays a dividend yield of about 1% higher than that of the market.

In the Apple article, we noted that Apple has significant cash and marketable securities and consistent earnings, allowing it to continue buying back its shares at a similar pace as in the past.

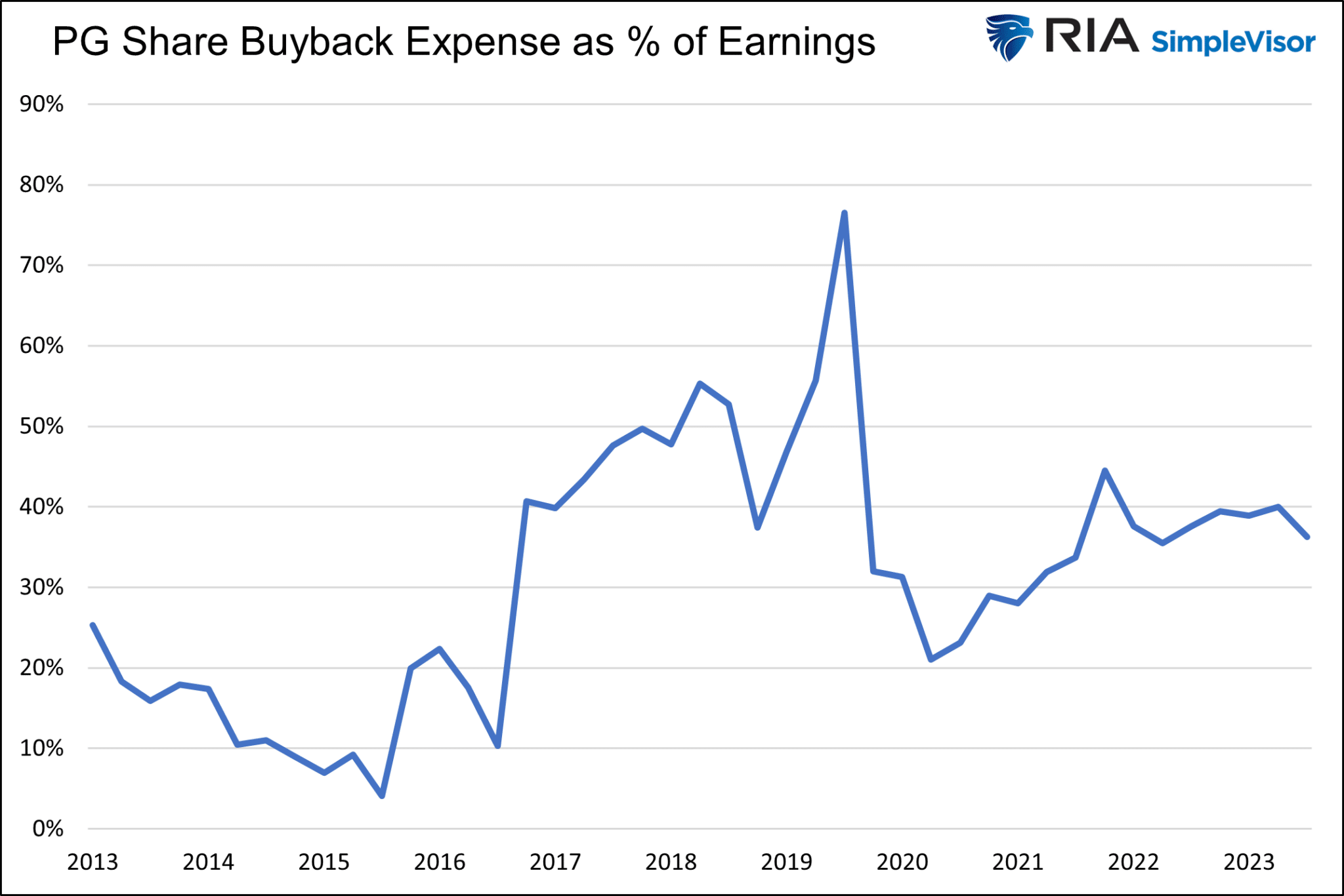

PG holds much less cash than Apple but has sufficient earnings to continue buying back its shares. Over the past few years, PG has used about a third of its income to buy back its shares. The graph below shows the percentage of earnings each quarter devoted to buying back its stock.

We see no reason other than a change in the law regarding buybacks or the company’s mindset that would slow or stop PG’s share repurchases.

PG is a very mature company with little innovation. As such, paying back its shareholders via buybacks and dividends may be the best use of their money. In Apple’s case, in which they must keep up with the latest technology, future investment is much more critical. As we wrote in the Apple article- “However if earnings are employed to buy back shares, it comes at the expense of investments toward innovations and product upgrades.”

Like Apple, a bet on PG is a bet on its ability to continue propping up its EPS with share buybacks.

Disclosure

This report is not a recommendation to buy or sell the named securities. We intend to elicit ideas about stocks meeting specific criteria and investment themes. Please read our disclosures carefully and do your own research before investing.